Vous aimerez peut-être aussi

- God of The Oppressed - James ConeDocument271 pagesGod of The Oppressed - James ConeArun Samuel Varghese97% (29)

- Assignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Document6 pagesAssignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Rajat Gupta100% (4)

- Druthers Forming Answer KeyDocument3 pagesDruthers Forming Answer KeyDesventes AdrienPas encore d'évaluation

- Business CaseDocument4 pagesBusiness CaseJoseph GonzalesPas encore d'évaluation

- Corporate Finance - PresentationDocument14 pagesCorporate Finance - Presentationguruprasadkudva83% (6)

- Lockeed 5 StarDocument6 pagesLockeed 5 StarAjay SinghPas encore d'évaluation

- Lockheed Case SolutionDocument3 pagesLockheed Case SolutionKashish SrivastavaPas encore d'évaluation

- NPV and IRR Calculations for Investment Projects AnalysisDocument8 pagesNPV and IRR Calculations for Investment Projects AnalysisCheytan Thakar100% (3)

- Lockheed Tristar Case SolutionDocument3 pagesLockheed Tristar Case SolutionPrakash Nishtala100% (1)

- Lockheed Tristar Case Similar SolutionDocument12 pagesLockheed Tristar Case Similar SolutionguruprasadkudvaPas encore d'évaluation

- Case Study: "Green Zebra": NotesDocument1 pageCase Study: "Green Zebra": NotesFlora PapastfPas encore d'évaluation

- Sealed AirDocument10 pagesSealed AirHimanshu KumarPas encore d'évaluation

- Finance Simulation Valuation ExerciseDocument7 pagesFinance Simulation Valuation ExerciseAdemola Adeola0% (2)

- Case Questions - Home DepotDocument4 pagesCase Questions - Home Depotanon_6801677100% (1)

- SunAir Boat BuildersDocument3 pagesSunAir Boat Buildersram_prabhu00325% (4)

- Week 5 Balancing Process Capacity Simulation Slides Challenge1 and Challenge 2 HHv2Document23 pagesWeek 5 Balancing Process Capacity Simulation Slides Challenge1 and Challenge 2 HHv2Mariam AlraeesiPas encore d'évaluation

- HBS CaseDocument3 pagesHBS CaseIvani Bora0% (1)

- Atmakaraka PDFDocument46 pagesAtmakaraka PDFrohitsingh_8150% (4)

- Lockheed Tristar ProjectDocument1 pageLockheed Tristar ProjectDurgaprasad VelamalaPas encore d'évaluation

- HPC Western India Refinery Project NPV AnalysisDocument1 pageHPC Western India Refinery Project NPV AnalysisAmmrita SharmaPas encore d'évaluation

- Operations Management Toffee IncDocument12 pagesOperations Management Toffee IncRonak PataliaPas encore d'évaluation

- Sneaker 2013 Business CaseDocument4 pagesSneaker 2013 Business CaseGiselli Castillo Gárate0% (1)

- Excel Spreadsheet Sampa VideoDocument5 pagesExcel Spreadsheet Sampa VideoFaith AllenPas encore d'évaluation

- Polaroid Corporation: Group MembersDocument7 pagesPolaroid Corporation: Group MemberscristinahumaPas encore d'évaluation

- Wills Lifestyle Group1 Section2Document5 pagesWills Lifestyle Group1 Section2vignesh asaithambiPas encore d'évaluation

- Capital Budgeting Decision for Hola-Kola's Zero-Calorie Soft DrinkDocument7 pagesCapital Budgeting Decision for Hola-Kola's Zero-Calorie Soft DrinkRivki MeitriyantoPas encore d'évaluation

- Valuing ProjectsDocument5 pagesValuing ProjectsAjay SinghPas encore d'évaluation

- Case 1 StudyDocument9 pagesCase 1 StudyJamesTho0% (1)

- Had On The $158,000 Profit of First Six Months of 2004? AnswerDocument3 pagesHad On The $158,000 Profit of First Six Months of 2004? AnswerRamalu Dinesh ReddyPas encore d'évaluation

- 2 - Global Supply Chain Management Simulation v2Document2 pages2 - Global Supply Chain Management Simulation v2prashant309100% (1)

- Investment Analysis and Lockheed TristarDocument9 pagesInvestment Analysis and Lockheed TristarRajesh KumarPas encore d'évaluation

- EDMU 520 Phonics Lesson ObservationDocument6 pagesEDMU 520 Phonics Lesson ObservationElisa FloresPas encore d'évaluation

- Investment Analysis - Lockheed Tri-StarDocument2 pagesInvestment Analysis - Lockheed Tri-Staraclink88100% (1)

- Assignment 2 Lockheed CaseDocument6 pagesAssignment 2 Lockheed CaseBob MarlowPas encore d'évaluation

- Lockheed Tri Star Capital Budgeting Case AnalysisDocument9 pagesLockheed Tri Star Capital Budgeting Case AnalysisMichael DevereauxPas encore d'évaluation

- Forecasting Case - XlxsDocument8 pagesForecasting Case - Xlxsmayank.dce123Pas encore d'évaluation

- Investment Analysis & Lockheed Case StudyDocument34 pagesInvestment Analysis & Lockheed Case StudyKshitij GuptaPas encore d'évaluation

- Valuing Capital Investment Projects For PracticeDocument18 pagesValuing Capital Investment Projects For PracticeShivam Goyal100% (1)

- Msdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleDocument24 pagesMsdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleShashank Shekhar100% (1)

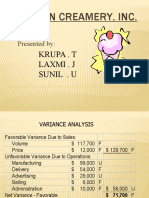

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Proforma Cash Flow Analysis and Recommendations for Chemalite IncDocument8 pagesProforma Cash Flow Analysis and Recommendations for Chemalite IncHàMềmPas encore d'évaluation

- Tristar Case Sol.Document4 pagesTristar Case Sol.Niketa JaiswalPas encore d'évaluation

- FM Assignment 2 IDocument2 pagesFM Assignment 2 Irahul gargPas encore d'évaluation

- Daud Engine Parts CompanyDocument3 pagesDaud Engine Parts CompanyJawadPas encore d'évaluation

- Wilkins Case SolutionDocument10 pagesWilkins Case SolutionSri Hari KrishnaPas encore d'évaluation

- Investment Banking: Individual Assignment 2Document5 pagesInvestment Banking: Individual Assignment 2Aakash Ladha100% (3)

- Worldwide Paper Company: Case Solution Company BackgroundDocument4 pagesWorldwide Paper Company: Case Solution Company BackgroundJauhari WicaksonoPas encore d'évaluation

- Planning The Product Mix at Panchtantra CorporationDocument14 pagesPlanning The Product Mix at Panchtantra CorporationNRLDCPas encore d'évaluation

- American Chemical CorporationDocument8 pagesAmerican Chemical CorporationAnastasiaPas encore d'évaluation

- Analysis Butler Lumber CompanyDocument3 pagesAnalysis Butler Lumber CompanyRoberto LlerenaPas encore d'évaluation

- Case StudyDocument10 pagesCase StudyEvelyn VillafrancaPas encore d'évaluation

- Samanya Building financialsDocument5 pagesSamanya Building financialsShiladitya Swarnakar0% (1)

- Applichemcase Group 5 - PresentationDocument20 pagesApplichemcase Group 5 - Presentationnick najitoPas encore d'évaluation

- ITC Echoupal Report - GR 1 - OSCMDocument28 pagesITC Echoupal Report - GR 1 - OSCMAishwarya Dash100% (1)

- Sec-2 - Subgroup-9 (FM-Hola Kola)Document9 pagesSec-2 - Subgroup-9 (FM-Hola Kola)Ankit VisputePas encore d'évaluation

- Answer - D, E, F, GDocument4 pagesAnswer - D, E, F, GAkash SharmaPas encore d'évaluation

- Lockheed Tristar Case AnalysisDocument9 pagesLockheed Tristar Case AnalysispranavPas encore d'évaluation

- Fin 630 Exam 1Document19 pagesFin 630 Exam 1jimmy_chou1314Pas encore d'évaluation

- Making Investment Decisions With The Net Present Value Rule: Principles of Corporate Finance, 8/eDocument26 pagesMaking Investment Decisions With The Net Present Value Rule: Principles of Corporate Finance, 8/eMuneendra BhardwajPas encore d'évaluation

- Long Run and Short Run (Final)Document39 pagesLong Run and Short Run (Final)subanerjee18Pas encore d'évaluation

- Case 1Document4 pagesCase 1Kamran IjazPas encore d'évaluation

- Shelby ShelvingDocument10 pagesShelby ShelvingrellimnojPas encore d'évaluation

- Capital Budgeting WorksheetDocument2 pagesCapital Budgeting WorksheetImperoCo LLCPas encore d'évaluation

- The Indian Bond MarketDocument2 pagesThe Indian Bond MarketR Harika ReddyPas encore d'évaluation

- Package Carrier ModifiedDocument13 pagesPackage Carrier ModifiedR Harika Reddy100% (1)

- UntitledDocument1 pageUntitledTamas GyörigPas encore d'évaluation

- NMAT2005Document29 pagesNMAT2005Mbatutes100% (3)

- Sample Paper 2011Document12 pagesSample Paper 2011R Harika ReddyPas encore d'évaluation

- GATE Instrumentation Engineering Solved 2013Document22 pagesGATE Instrumentation Engineering Solved 2013Meghraj ChiniyaPas encore d'évaluation

- José Rizal: The Life of The National HeroDocument9 pagesJosé Rizal: The Life of The National HeroMark Harry Olivier P. VanguardiaPas encore d'évaluation

- MRI BRAIN FINAL DR Shamol PDFDocument306 pagesMRI BRAIN FINAL DR Shamol PDFDrSunil Kumar DasPas encore d'évaluation

- Diaphragmatic Breathing - The Foundation of Core Stability PDFDocument7 pagesDiaphragmatic Breathing - The Foundation of Core Stability PDFElaine CspPas encore d'évaluation

- Eight Principles of Ethical Leadership in EducationDocument2 pagesEight Principles of Ethical Leadership in EducationKimberly Rose Nativo100% (1)

- Wild (E) Men and SavagesDocument237 pagesWild (E) Men and SavagesAhmed DiaaPas encore d'évaluation

- Phronesis Volume 7 Issue 1 1962 (Doi 10.2307/4181698) John Malcolm - The Line and The CaveDocument9 pagesPhronesis Volume 7 Issue 1 1962 (Doi 10.2307/4181698) John Malcolm - The Line and The CaveNițceValiPas encore d'évaluation

- DefenseDocument20 pagesDefenseManny De MesaPas encore d'évaluation

- Alpha To Omega PPT (David & Krishna)Document11 pagesAlpha To Omega PPT (David & Krishna)gsdrfwpfd2Pas encore d'évaluation

- ID Kajian Hukum Perjanjian Perkawinan Di Kalangan Wni Islam Studi Di Kota Medan PDFDocument17 pagesID Kajian Hukum Perjanjian Perkawinan Di Kalangan Wni Islam Studi Di Kota Medan PDFsabila azilaPas encore d'évaluation

- Rock and Roll and The American Dream: Essential QuestionDocument7 pagesRock and Roll and The American Dream: Essential QuestionChad HorsleyPas encore d'évaluation

- PrisonerDocument10 pagesPrisonerAbdi ShakourPas encore d'évaluation

- Ch5 Multivariate MethodsDocument26 pagesCh5 Multivariate MethodsRikiPas encore d'évaluation

- En458 PDFDocument1 168 pagesEn458 PDFpantocrat0r100% (1)

- My Experience With DreamsDocument7 pagesMy Experience With DreamsPamela Rivera SantosPas encore d'évaluation

- B1 Mod 01 MathsDocument152 pagesB1 Mod 01 MathsTharrmaselan VmanimaranPas encore d'évaluation

- 1201 CCP Literature ReviewDocument5 pages1201 CCP Literature Reviewapi-548148057Pas encore d'évaluation

- English 7 1st Lesson Plan For 2nd QuarterDocument4 pagesEnglish 7 1st Lesson Plan For 2nd QuarterDiane LeonesPas encore d'évaluation

- TGT EnglishDocument3 pagesTGT EnglishKatta SrinivasPas encore d'évaluation

- Native Immersion #2 - Shopping in A Nutshell PDFDocument43 pagesNative Immersion #2 - Shopping in A Nutshell PDFmeenaPas encore d'évaluation

- Chapter 8 SQL Complex QueriesDocument51 pagesChapter 8 SQL Complex QueriesJiawei TanPas encore d'évaluation

- ECO 201 Sample Midterm Exam (Paulo GuimaraesDocument14 pagesECO 201 Sample Midterm Exam (Paulo GuimaraesAhmed NegmPas encore d'évaluation

- Minutes: Motion Was Submitted For ResolutionDocument29 pagesMinutes: Motion Was Submitted For Resolutionayen cusiPas encore d'évaluation

- (PC) Brian Barlow v. California Dept. of Corrections Et Al - Document No. 4Document2 pages(PC) Brian Barlow v. California Dept. of Corrections Et Al - Document No. 4Justia.comPas encore d'évaluation

- Christoffel Symbols: PHYS 471: Introduction To Relativity and CosmologyDocument9 pagesChristoffel Symbols: PHYS 471: Introduction To Relativity and Cosmologyarileo3100% (1)

- Lynn Hunt - Writing History in The Global Era-W.W. Norton & Company (2014)Document83 pagesLynn Hunt - Writing History in The Global Era-W.W. Norton & Company (2014)Ricardo Valenzuela100% (2)

- A Practice Teaching Narrative of Experience in Off Campus InternshipDocument84 pagesA Practice Teaching Narrative of Experience in Off Campus InternshipClarenz Jade Magdoboy MonseratePas encore d'évaluation