Vous aimerez peut-être aussi

- Buckwold12e Solutions Ch07Document41 pagesBuckwold12e Solutions Ch07awerweasd100% (1)

- Buckwold11e Solutions Ch08Document63 pagesBuckwold11e Solutions Ch08Ravindra Joshi0% (1)

- Chapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013Document32 pagesChapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013melsun007Pas encore d'évaluation

- BUS345 Midterm 1 NotesDocument31 pagesBUS345 Midterm 1 NotesՄարիա ՄինասեանPas encore d'évaluation

- Chap 01Document13 pagesChap 01Tim JamesPas encore d'évaluation

- BU 357 Wilfrid Laurier HomeworkDocument35 pagesBU 357 Wilfrid Laurier HomeworkNia ニア MulyaningsihPas encore d'évaluation

- Tax Answers 2Document280 pagesTax Answers 2Don83% (6)

- Corporate Distributions, Windings-Up, and Sales: Solutions To Chapter 15 Assignment ProblemsDocument21 pagesCorporate Distributions, Windings-Up, and Sales: Solutions To Chapter 15 Assignment ProblemsKiều Thảo AnhPas encore d'évaluation

- Hilton6e SM08Document70 pagesHilton6e SM08Eych MendozaPas encore d'évaluation

- Chap03 Sol OddDocument19 pagesChap03 Sol OddRussell WilsonPas encore d'évaluation

- Computation of Taxable Income and Tax After General Reductions For CorporationsDocument20 pagesComputation of Taxable Income and Tax After General Reductions For CorporationsKiều Thảo Anh100% (1)

- Chap 06Document30 pagesChap 06Tim JamesPas encore d'évaluation

- Test Bank For Modern Advanced Accounting in Canada Canadian 7th Edition by HiltonDocument6 pagesTest Bank For Modern Advanced Accounting in Canada Canadian 7th Edition by Hiltonhezodyvar80% (5)

- Chapter 01 - Introduction To Federal Taxation in CanadaDocument40 pagesChapter 01 - Introduction To Federal Taxation in CanadaDonna So100% (2)

- Exam SampleDocument15 pagesExam SampleKim LePas encore d'évaluation

- Download: Acc 307 Final Exam Part 1Document2 pagesDownload: Acc 307 Final Exam Part 1AlexPas encore d'évaluation

- Business Combinations: 2005 Mcgraw-Hill Ryerson Limited. All Rights Reserved. 52Document37 pagesBusiness Combinations: 2005 Mcgraw-Hill Ryerson Limited. All Rights Reserved. 52cpscbd9Pas encore d'évaluation

- CH 7 Answer KeyDocument88 pagesCH 7 Answer KeyT m100% (1)

- Chapter Two SolutionsDocument9 pagesChapter Two Solutionsapi-3705855Pas encore d'évaluation

- Chap 02Document25 pagesChap 02Tim JamesPas encore d'évaluation

- Corporation TaxationDocument16 pagesCorporation TaxationMeg Lee0% (1)

- Chapter 11 Question Answer KeyDocument91 pagesChapter 11 Question Answer KeyBrian Schweinsteiger Fok100% (1)

- Consolidation Subsequent To Acquisition Date: Solutions Manual, Chapter 5Document86 pagesConsolidation Subsequent To Acquisition Date: Solutions Manual, Chapter 5olivia caoPas encore d'évaluation

- Byrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1st Edition Byrd Solutions ManualDocument9 pagesByrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1st Edition Byrd Solutions Manuallemon787100% (5)

- Chapter 16 Sol 2020 WKDocument53 pagesChapter 16 Sol 2020 WKVu Khanh LePas encore d'évaluation

- Tax QuestionsDocument261 pagesTax QuestionsPocaGuri100% (1)

- Chapter 16 & 17 ProblemsDocument31 pagesChapter 16 & 17 ProblemsKevin Tee100% (3)

- CH 10 TBDocument18 pagesCH 10 TBjhaydn100% (1)

- Exam 2 Income Tax Study Guide (The Better Version)Document48 pagesExam 2 Income Tax Study Guide (The Better Version)Mary Tol100% (1)

- SolutionsDocument24 pagesSolutionsapi-38170720% (1)

- Tax of Business Entities Chapter 4Document38 pagesTax of Business Entities Chapter 4craig52292Pas encore d'évaluation

- Canadian Tax Principles 2017-2018. Study Guide QuestionsDocument266 pagesCanadian Tax Principles 2017-2018. Study Guide QuestionsTimilehin Akintayo100% (9)

- Tax Outline: What Is Income?Document19 pagesTax Outline: What Is Income?Sio MoPas encore d'évaluation

- Beechy 7ce v2 Ch18Document89 pagesBeechy 7ce v2 Ch18منیر سادات0% (2)

- Taxation of Partnerships PowerpointDocument7 pagesTaxation of Partnerships PowerpointALAJID, KIM EMMANUELPas encore d'évaluation

- Tax Notes 5Document29 pagesTax Notes 5spiotrowskiPas encore d'évaluation

- Buckwold12e Solutions Ch11Document40 pagesBuckwold12e Solutions Ch11Fang YanPas encore d'évaluation

- Chapter 5Document26 pagesChapter 5Reese Parker33% (3)

- Test Bank For McGraw Hills Taxation of Business Entities 2019 Edition 10th Edition by Brian C. SpilkerDocument19 pagesTest Bank For McGraw Hills Taxation of Business Entities 2019 Edition 10th Edition by Brian C. SpilkerTestbanks Here100% (1)

- Chapter 5 Question Answer KeyDocument83 pagesChapter 5 Question Answer KeyBrian Schweinsteiger FokPas encore d'évaluation

- Chapter 11 TaxDocument21 pagesChapter 11 TaxMatt HratkoPas encore d'évaluation

- Depreciable Property and Eligible Capital Property: Solutions To Chapter 5 Assignment ProblemsDocument27 pagesDepreciable Property and Eligible Capital Property: Solutions To Chapter 5 Assignment ProblemsOktariadie RamadhianPas encore d'évaluation

- Chapter 1 - Sol - 2023 Introduction To Federal Income Taxation in Canada, 44th EditionDocument5 pagesChapter 1 - Sol - 2023 Introduction To Federal Income Taxation in Canada, 44th Editionfullgradestore2023Pas encore d'évaluation

- Case Notes EcoPakDocument8 pagesCase Notes EcoPakGajan SelvaPas encore d'évaluation

- Controls at The Bellagio Casino ResortDocument2 pagesControls at The Bellagio Casino ResortFareeha Anwar0% (1)

- SolutionsDocument17 pagesSolutionsapi-3817072Pas encore d'évaluation

- US Taxation - Outline: I. Types of Tax Rate StructuresDocument12 pagesUS Taxation - Outline: I. Types of Tax Rate Structuresvarghese2007Pas encore d'évaluation

- SMCHAP025Document29 pagesSMCHAP025testbank100% (3)

- CHAPTER 5 Depreciable Capital Property and Eligible Capital PropertyDocument20 pagesCHAPTER 5 Depreciable Capital Property and Eligible Capital PropertyNia ニア Mulyaningsih100% (6)

- Chap 010 - Taxation of Individuals and Business EntitiesDocument63 pagesChap 010 - Taxation of Individuals and Business Entitiesaffy714Pas encore d'évaluation

- Transfer Taxes and Wealth Planning Solutions Manual: Discussion QuestionsDocument29 pagesTransfer Taxes and Wealth Planning Solutions Manual: Discussion QuestionsAstha GoplaniPas encore d'évaluation

- Tax Cheat Sheet Exam 2 - CH 7,8,10,11Document2 pagesTax Cheat Sheet Exam 2 - CH 7,8,10,11tyg1992Pas encore d'évaluation

- Partnership AllocationDocument63 pagesPartnership AllocationMitchelGramaticaPas encore d'évaluation

- McGraw-Hill's Taxation of Business Entities, 2016 EditionDocument28 pagesMcGraw-Hill's Taxation of Business Entities, 2016 Editiontravelling100% (1)

- Computation of Taxable Income and Tax After General Reductions For CorporationsDocument35 pagesComputation of Taxable Income and Tax After General Reductions For Corporationsjahcaveman75% (4)

- SolutionsDocument12 pagesSolutionsapi-381707233% (3)

- Controls at Belagio Resort CaseDocument21 pagesControls at Belagio Resort CasemaastrichtpiePas encore d'évaluation

- 15gift and Estate Tax - Katzenstein - Fall 2002Document95 pages15gift and Estate Tax - Katzenstein - Fall 2002proveitwasmePas encore d'évaluation

- Essentials of Federal Taxation 3rd Edition Spilker Solutions Manual Full Chapter PDFDocument67 pagesEssentials of Federal Taxation 3rd Edition Spilker Solutions Manual Full Chapter PDFdilysiristtes5100% (13)

- Aa TaxDocument22 pagesAa Taxnirshan rajPas encore d'évaluation

- Client Letter - Federal Income TaxesDocument8 pagesClient Letter - Federal Income TaxesReese ParkerPas encore d'évaluation

- Chapter 6Document29 pagesChapter 6Reese Parker20% (5)

- Chapter 5Document26 pagesChapter 5Reese Parker33% (3)

- Chapter 1 Fundamentals of Taxation by Cruz, Deschamps, Miswander, Prendergast, Schisler, and TroneDocument25 pagesChapter 1 Fundamentals of Taxation by Cruz, Deschamps, Miswander, Prendergast, Schisler, and TroneReese Parker100% (4)

- Promotion LetterDocument1 pagePromotion Letterpooja245chauPas encore d'évaluation

- Sepco Online BilllDocument1 pageSepco Online Billlshaikh_piscesPas encore d'évaluation

- Abc Bill No.1372 Santhosh SDocument1 pageAbc Bill No.1372 Santhosh Ssanthosh srinivasPas encore d'évaluation

- MGM Budget 2008Document1 pageMGM Budget 2008Stonegate Subdivision HOAPas encore d'évaluation

- Chapter 11 TaxDocument11 pagesChapter 11 Taxkp_popinjPas encore d'évaluation

- Tax Invoice: State Name Delhi, Code 07Document1 pageTax Invoice: State Name Delhi, Code 07Ritesh pandeyPas encore d'évaluation

- St. Joseph County ProposalsDocument1 pageSt. Joseph County ProposalsWXMIPas encore d'évaluation

- Click Here To View Your Aliyah Benefits at A GlanceDocument1 pageClick Here To View Your Aliyah Benefits at A GlanceAyelen FlintPas encore d'évaluation

- Sample Payroll System Codes Via Visual Fox ProDocument6 pagesSample Payroll System Codes Via Visual Fox ProDiana Hermida100% (1)

- U.S. Individual Income Tax Return: (See Instructions.)Document2 pagesU.S. Individual Income Tax Return: (See Instructions.)Daniel RamirezPas encore d'évaluation

- Guide To The Completion of The EMPLOYEE Income Tax FormDocument5 pagesGuide To The Completion of The EMPLOYEE Income Tax FormMarz CuculPas encore d'évaluation

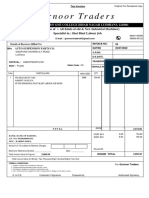

- Gurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobDocument1 pageGurnoor Traders: Sale & Purchase Of:-All Kinds of Old & New Industrial Machinery Specialist In: Shot Blast Labour JobANMOLPas encore d'évaluation

- Model SlipDocument1 pageModel SlipNithiyanantham BcomcaPas encore d'évaluation

- Summary of Final Income: Tax TableDocument3 pagesSummary of Final Income: Tax TableRealEXcellence71% (7)

- Inv 004093Document1 pageInv 004093Hyderabad CastingsPas encore d'évaluation

- L Lull: Offs:308 H-1, Garg Tower, Netaji Subhash Place Pitampura, Delhi-110034Document4 pagesL Lull: Offs:308 H-1, Garg Tower, Netaji Subhash Place Pitampura, Delhi-110034Nidhi Aggarwal SinghalPas encore d'évaluation

- BONUS ACT 1965 FORM-A Computation of Allocable SurplusDocument1 pageBONUS ACT 1965 FORM-A Computation of Allocable SurplusUmesh KumarPas encore d'évaluation

- BIR Form 1702-RTDocument8 pagesBIR Form 1702-RTDianne SantiagoPas encore d'évaluation

- 2021 Tax Rates SwitzerlandDocument4 pages2021 Tax Rates SwitzerlandKamil JanasPas encore d'évaluation

- Sales Tax3650193129439Document12 pagesSales Tax3650193129439tayyabPas encore d'évaluation

- 2015 Itr1 PR9Document9 pages2015 Itr1 PR9Soumyaranjan SwainPas encore d'évaluation

- Breakfast For Paul HodesDocument4 pagesBreakfast For Paul HodesSunlight FoundationPas encore d'évaluation

- GHFHDocument8 pagesGHFHnicahPas encore d'évaluation

- Salary Slip (30385759 May, 2018)Document1 pageSalary Slip (30385759 May, 2018)munafPas encore d'évaluation

- Foreign Tax Credit - Worked Example From IRASDocument1 pageForeign Tax Credit - Worked Example From IRASItorin DigitalPas encore d'évaluation

- Comey AuditDocument5 pagesComey AuditDanny ChaitinPas encore d'évaluation

- Ack 456121331281023Document1 pageAck 456121331281023Subrat SahooPas encore d'évaluation

- Prelim Exam-Business Tax - Set BDocument3 pagesPrelim Exam-Business Tax - Set BRenalyn Paras0% (1)

- Vat & Tax CalculatorDocument6 pagesVat & Tax CalculatorRoyPas encore d'évaluation

- Format For TaxationDocument4 pagesFormat For TaxationSITI NURFARHANA AB RAZAKPas encore d'évaluation

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Creating Shareholder Value: A Guide For Managers And InvestorsD'EverandCreating Shareholder Value: A Guide For Managers And InvestorsÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingD'EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (17)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 3.5 sur 5 étoiles3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthD'EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthÉvaluation : 4 sur 5 étoiles4/5 (20)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelD'Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelPas encore d'évaluation

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursD'EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (18)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamD'EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamPas encore d'évaluation

- Mind over Money: The Psychology of Money and How to Use It BetterD'EverandMind over Money: The Psychology of Money and How to Use It BetterÉvaluation : 4 sur 5 étoiles4/5 (24)

- Financial Risk Management: A Simple IntroductionD'EverandFinancial Risk Management: A Simple IntroductionÉvaluation : 4.5 sur 5 étoiles4.5/5 (7)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsD'EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsD'EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsPas encore d'évaluation

- Product-Led Growth: How to Build a Product That Sells ItselfD'EverandProduct-Led Growth: How to Build a Product That Sells ItselfÉvaluation : 5 sur 5 étoiles5/5 (1)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)D'EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Évaluation : 4 sur 5 étoiles4/5 (5)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistD'EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistÉvaluation : 4 sur 5 étoiles4/5 (32)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursD'EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursÉvaluation : 4.5 sur 5 étoiles4.5/5 (34)

- How to Measure Anything: Finding the Value of Intangibles in BusinessD'EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessÉvaluation : 3.5 sur 5 étoiles3.5/5 (4)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondD'EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondPas encore d'évaluation