Vous aimerez peut-être aussi

- A Project Report ON Ratio Analysis at Raddy'S LaboratoryDocument31 pagesA Project Report ON Ratio Analysis at Raddy'S LaboratoryKalpana Gunreddy100% (1)

- Analyzing Dr. Reddy's Market ShareDocument61 pagesAnalyzing Dr. Reddy's Market ShareGaurav Jaiswal100% (1)

- Lupin LTD (3rd Largest Pharma Company of India)Document56 pagesLupin LTD (3rd Largest Pharma Company of India)vidushikanwar67% (3)

- DR Reddy PharmaceuticalsDocument17 pagesDR Reddy PharmaceuticalstnschandraPas encore d'évaluation

- Tata Motors Financial Anlysis Project Report 2021Document19 pagesTata Motors Financial Anlysis Project Report 2021Karan Jadhav100% (1)

- Financial Performance of HCLDocument26 pagesFinancial Performance of HCLshirley100% (1)

- Dabur Working Capital Management Dabur IndiaDocument55 pagesDabur Working Capital Management Dabur IndiaPankaj ThakurPas encore d'évaluation

- Dr. Reddy's Laboratories Business Model and Three Core BusinessesDocument2 pagesDr. Reddy's Laboratories Business Model and Three Core BusinessesSubhanjan BhattacharyaPas encore d'évaluation

- Financial Analysis of ONGCDocument70 pagesFinancial Analysis of ONGCBhavya100% (6)

- Ratio Analysis Project On Lupin Pharmaceutical CompanyDocument93 pagesRatio Analysis Project On Lupin Pharmaceutical CompanyShilpa Reddy50% (2)

- CIPLA & Pharma Detail AnalysisDocument19 pagesCIPLA & Pharma Detail Analysisvijay kumarPas encore d'évaluation

- Project Report of Dr. Reddy'sDocument66 pagesProject Report of Dr. Reddy'srguha198685% (13)

- Organizational Structure of Eicher Motors and Royal EnfieldDocument16 pagesOrganizational Structure of Eicher Motors and Royal EnfieldBalaram ChampannavarPas encore d'évaluation

- Project Report: Cipla LTDDocument28 pagesProject Report: Cipla LTDBhakti Shinde100% (1)

- Dabur FinalDocument89 pagesDabur FinalRahul Anand100% (1)

- Asian Paints SWOT analysis examines strengths, weaknesses, opportunities and threatsDocument2 pagesAsian Paints SWOT analysis examines strengths, weaknesses, opportunities and threatsparth100% (1)

- Cipla Ltd. Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisDocument14 pagesCipla Ltd. Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisAnushka SinhaPas encore d'évaluation

- Ratio Analysis Reveals Dabur's Strong Financial PositionDocument100 pagesRatio Analysis Reveals Dabur's Strong Financial PositionManish Gupta75% (4)

- GSKDocument22 pagesGSKChaudhary Hassan ArainPas encore d'évaluation

- A Study On The Fundamental Analysis On Bajaj Auto LimitedDocument65 pagesA Study On The Fundamental Analysis On Bajaj Auto Limitedprayas sarkar50% (2)

- This Report On CiplaDocument34 pagesThis Report On CiplaDeepak Rana75% (4)

- Sales and Distribution of Zydus Wellness: A Project Report OnDocument19 pagesSales and Distribution of Zydus Wellness: A Project Report OnJe RomePas encore d'évaluation

- A Study On Financial Statement Analysis of Tata SteelDocument16 pagesA Study On Financial Statement Analysis of Tata SteelGokul krishnanPas encore d'évaluation

- Implementation of 7s Srategy in DR Reddy'sDocument10 pagesImplementation of 7s Srategy in DR Reddy'schaithanyaPas encore d'évaluation

- Tata MotorsDocument49 pagesTata MotorsUnknown 123Pas encore d'évaluation

- Acquisition of Air IndiaDocument4 pagesAcquisition of Air IndiaHJ ManviPas encore d'évaluation

- Finance Project 2Document25 pagesFinance Project 2Mehak UmerPas encore d'évaluation

- Marketing Research and Consumer Behaviour Case StudyDocument7 pagesMarketing Research and Consumer Behaviour Case StudyFaizan Aalam75% (4)

- Project Report Manisha Sharma Anand CiplaDocument68 pagesProject Report Manisha Sharma Anand CiplaAyush Tiwari100% (1)

- Capital Budgeting Analysis at Indian Oil CorporationDocument16 pagesCapital Budgeting Analysis at Indian Oil CorporationBhargavi Dodda100% (1)

- Review of LiteratureDocument9 pagesReview of Literatureasir immanuvelPas encore d'évaluation

- Job Satisfaction at Baidyanath pvt Limited NagpurDocument12 pagesJob Satisfaction at Baidyanath pvt Limited Nagpurrahul khobragadePas encore d'évaluation

- Cadila's Journey to Becoming a Leading Pharma CompanyDocument70 pagesCadila's Journey to Becoming a Leading Pharma CompanyVikalp Tomar100% (1)

- Final Project of Ratio Analysis - PrakashDocument166 pagesFinal Project of Ratio Analysis - PrakashSamir UpadhyayPas encore d'évaluation

- Ratio Analysis - Ashokleyland SUDHEERDocument83 pagesRatio Analysis - Ashokleyland SUDHEERArun Kumar100% (3)

- Executive Summary: Description of Project in BriefDocument60 pagesExecutive Summary: Description of Project in BriefkrishnaPas encore d'évaluation

- EIC Analysis of FMCG SectorDocument37 pagesEIC Analysis of FMCG SectorBig BullsPas encore d'évaluation

- Financial Analysis of Tata Steel and Jindal Steel and Power Ltd.Document34 pagesFinancial Analysis of Tata Steel and Jindal Steel and Power Ltd.O.p. SharmaPas encore d'évaluation

- HDFC-HDFC Bank MergerDocument18 pagesHDFC-HDFC Bank Mergershriramdeshpande431100% (1)

- VLINK SIP Project ReportDocument51 pagesVLINK SIP Project ReportABHINAV SHANKHDHARPas encore d'évaluation

- TATA MOTORS Atif PDFDocument9 pagesTATA MOTORS Atif PDFAtif Raza AkbarPas encore d'évaluation

- Apollo Tyres Brand ImageDocument61 pagesApollo Tyres Brand ImageShahzad SaifPas encore d'évaluation

- Finance ProjectDocument79 pagesFinance Projectram krishnaPas encore d'évaluation

- Final 1 - Mankind Pharma ReportDocument133 pagesFinal 1 - Mankind Pharma ReportMahabalaPas encore d'évaluation

- A Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance Analysis With Reference To Kesoram CementDocument81 pagesA Study A Study On Financial Performance Analysis With Reference To Kesoram Cementon Financial Performance Analysis With Reference To Kesoram CementjeganrajrajPas encore d'évaluation

- Financial Analysis of ITC Limited (ITCDocument97 pagesFinancial Analysis of ITC Limited (ITCRavi BarotPas encore d'évaluation

- Company Analysis Report On AirtelDocument39 pagesCompany Analysis Report On AirtelSUDEEP KUMAR69% (13)

- Tata Motors Cost of CapitalDocument10 pagesTata Motors Cost of CapitalMia KhalifaPas encore d'évaluation

- Cipla LTD Company ProfileDocument13 pagesCipla LTD Company ProfileAdnan Ejaz33% (3)

- 1a. PWC Article Exercise - The Four Worlds of Work in 2030Document6 pages1a. PWC Article Exercise - The Four Worlds of Work in 2030dffdf fdfg0% (1)

- Tata Steel: A Century of Excellence in the Global Steel IndustryDocument33 pagesTata Steel: A Century of Excellence in the Global Steel Industryabhay00750% (2)

- CVP Analysis ProjectDocument63 pagesCVP Analysis ProjectMBA Sec APas encore d'évaluation

- Cadila PharmaceuticalsDocument27 pagesCadila Pharmaceuticals12ekPas encore d'évaluation

- Case Study On Strategic MGTDocument13 pagesCase Study On Strategic MGTAtulAtulKumarAgarwalPas encore d'évaluation

- Financial Analysis of Cipla, Dr. Reddy and LupinDocument14 pagesFinancial Analysis of Cipla, Dr. Reddy and LupinParth GuptaPas encore d'évaluation

- Lavya Minor Project SampleDocument21 pagesLavya Minor Project SampleUday GuptaPas encore d'évaluation

- DR Reddy'sDocument6 pagesDR Reddy'sViraat Lakhanpal0% (1)

- Dr. Reddy'S Laboratories LimitedDocument36 pagesDr. Reddy'S Laboratories LimitedJagadesh PPas encore d'évaluation

- DR Reddy's AmericaDocument2 pagesDR Reddy's AmericaxadityasharmaxPas encore d'évaluation

- Business Strategy AssignmentDocument17 pagesBusiness Strategy AssignmentAnkit SinghPas encore d'évaluation

- Fitch - Accounting ManipulationDocument13 pagesFitch - Accounting ManipulationMarius MuresanPas encore d'évaluation

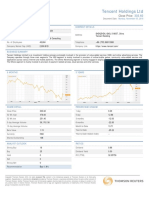

- Tencent Holdings LTD: Close PriceDocument2 pagesTencent Holdings LTD: Close PricetrungPas encore d'évaluation

- Eportfolio AssignmentDocument12 pagesEportfolio Assignmentapi-300872702Pas encore d'évaluation

- A.2. Liabilities and EquityDocument27 pagesA.2. Liabilities and EquityKondreddi SakuPas encore d'évaluation

- Goodwill Games PDFDocument2 pagesGoodwill Games PDFSid SavaraPas encore d'évaluation

- Investment AppraisalDocument18 pagesInvestment AppraisalKwasi MmehPas encore d'évaluation

- Advanced Financial Accounting TopicsDocument16 pagesAdvanced Financial Accounting TopicsNhel AlvaroPas encore d'évaluation

- Financial Statements ExercicesDocument7 pagesFinancial Statements Exercicesluliga.loulouPas encore d'évaluation

- Case Study SolutionDocument4 pagesCase Study Solutionganesh teja0% (1)

- 1 AssignmentDocument4 pages1 AssignmentHammad Hassan AsnariPas encore d'évaluation

- Accounting Info for Decision MakingDocument77 pagesAccounting Info for Decision Makingsat satw100% (1)

- Valuation of Apollo Tyres Using 4 Methods Shows UndervaluationDocument3 pagesValuation of Apollo Tyres Using 4 Methods Shows UndervaluationnityaPas encore d'évaluation

- Accounting EquationDocument36 pagesAccounting EquationZainon Idris100% (1)

- Calculate WACC for bond and equity valuationDocument3 pagesCalculate WACC for bond and equity valuationStephanie Dian AureliaPas encore d'évaluation

- 224 Integrated PeriodEnd Closing ActivitiesDocument42 pages224 Integrated PeriodEnd Closing ActivitiesshujasirajPas encore d'évaluation

- Dividend PolicyDocument51 pagesDividend PolicyMmonower HosenPas encore d'évaluation

- IFRS3: Business CombinationDocument56 pagesIFRS3: Business Combinationmesfin yemerPas encore d'évaluation

- Module 7 - PAS 16 PPEDocument6 pagesModule 7 - PAS 16 PPEbladdor DG.Pas encore d'évaluation

- Financial Statement of A CompanyDocument49 pagesFinancial Statement of A CompanyApollo Institute of Hospital Administration100% (3)

- NIKE Inc Ten Year Financial History FY19Document1 pageNIKE Inc Ten Year Financial History FY19Moisés Ríos RamosPas encore d'évaluation

- Activity 10Document2 pagesActivity 10Randelle James FiestaPas encore d'évaluation

- Accounting 211 Chapter 5Document46 pagesAccounting 211 Chapter 5Darwin QuintosPas encore d'évaluation

- Tugas Kelompok Ke-1 (Minggu 3) : Case 1Document10 pagesTugas Kelompok Ke-1 (Minggu 3) : Case 1Kenny BagusPas encore d'évaluation

- Chart of AccountsDocument3 pagesChart of AccountsJacePas encore d'évaluation

- BF SG 12 0203Document31 pagesBF SG 12 0203JOSHUA GABATEROPas encore d'évaluation

- Recognition and Measurement of The Elements of Financial StatementsDocument17 pagesRecognition and Measurement of The Elements of Financial StatementsRudraksh WaliaPas encore d'évaluation

- CF Assignment 2 Group 9Document35 pagesCF Assignment 2 Group 9rishabh tyagiPas encore d'évaluation

- Actgfr Group 3 Chapter 8 Problem 8-6Document24 pagesActgfr Group 3 Chapter 8 Problem 8-6KrizahMarieCaballeroPas encore d'évaluation

- Accounting VacationDocument28 pagesAccounting VacationPro NdebelePas encore d'évaluation