Vous aimerez peut-être aussi

- AppealsDocument25 pagesAppealsArun ShokeenPas encore d'évaluation

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaPas encore d'évaluation

- Business Ethics and Professional Values: Unit - I - IntroductionDocument36 pagesBusiness Ethics and Professional Values: Unit - I - IntroductionnnanditasinghPas encore d'évaluation

- Income From SalaryDocument54 pagesIncome From SalaryJyoti Kalotra70% (10)

- Residential Status Under Income-Tax Act, 1961Document6 pagesResidential Status Under Income-Tax Act, 1961Bharat Tailor100% (1)

- Capital Gains Taxation in IndiaDocument3 pagesCapital Gains Taxation in IndiavikramkukrejaPas encore d'évaluation

- Setting Up of NCLT & NCLATDocument23 pagesSetting Up of NCLT & NCLATRaksha KediaPas encore d'évaluation

- Control of Eviction of Tenant With Role of Slum Area Improvement and Clearance Act 1956Document23 pagesControl of Eviction of Tenant With Role of Slum Area Improvement and Clearance Act 1956Anmol ChitranshiPas encore d'évaluation

- Appeal Procedure for Income Tax CommissionerDocument17 pagesAppeal Procedure for Income Tax CommissionerRajeev RajPas encore d'évaluation

- ASSIGNMENT 1 (Corporate TAX)Document10 pagesASSIGNMENT 1 (Corporate TAX)SandeepPas encore d'évaluation

- Indirect Tax AssignmentDocument6 pagesIndirect Tax AssignmentVishal AgarwalPas encore d'évaluation

- Class - 1 Clubbing of IncomeDocument41 pagesClass - 1 Clubbing of IncomeTomy MathewPas encore d'évaluation

- 15831b - Income Tax AuthoritiesDocument23 pages15831b - Income Tax AuthoritiesanmoldeepsinghPas encore d'évaluation

- Taxation of CompaniesDocument37 pagesTaxation of CompaniesSukirti Shikha50% (2)

- Vodafone Tax CaseDocument15 pagesVodafone Tax CaseBharti BansalPas encore d'évaluation

- Taxation Law ProjectDocument15 pagesTaxation Law Projectraj vardhan agarwalPas encore d'évaluation

- "Enforcement of Arbitration Award": D - R M L N L U, LDocument20 pages"Enforcement of Arbitration Award": D - R M L N L U, Lhardik anandPas encore d'évaluation

- Understand Customs Duty in IndiaDocument17 pagesUnderstand Customs Duty in IndiaMubbashir Khan RanaPas encore d'évaluation

- CCIDocument22 pagesCCIsdj32Pas encore d'évaluation

- Customs Duty Guide: Taxes, Rates, and ProceduresDocument9 pagesCustoms Duty Guide: Taxes, Rates, and ProceduresVarsha ThampiPas encore d'évaluation

- Income Tax ProjectDocument14 pagesIncome Tax ProjectBharat JoshiPas encore d'évaluation

- Insurance Project : RiskDocument21 pagesInsurance Project : RiskPrashant MahawarPas encore d'évaluation

- Taxation Assignment: An Overview of Double Taxation Avoidance Agreements: IndiaDocument12 pagesTaxation Assignment: An Overview of Double Taxation Avoidance Agreements: IndiaNasif MustahidPas encore d'évaluation

- Income From Other SourcesDocument9 pagesIncome From Other Sourcesrajsab20061093Pas encore d'évaluation

- Goods and Services Tax DetailsDocument27 pagesGoods and Services Tax DetailsAyush MishraPas encore d'évaluation

- SEBI Guidelines For IPODocument5 pagesSEBI Guidelines For IPOabhiraj_bangeraPas encore d'évaluation

- SEBI's Role as India's Market RegulatorDocument18 pagesSEBI's Role as India's Market RegulatorUtkarsh KumarPas encore d'évaluation

- MRTP Act and Competition Act: A RevieDocument50 pagesMRTP Act and Competition Act: A RevieAditya SoniPas encore d'évaluation

- Depository Services ExplainedDocument7 pagesDepository Services ExplainedakhilPas encore d'évaluation

- Resdential Status Questionsby Garun Kumar GDCM SrikakulamDocument9 pagesResdential Status Questionsby Garun Kumar GDCM Srikakulamgeddadaarun100% (1)

- Role of Residential Status in Tax LiabilityDocument9 pagesRole of Residential Status in Tax LiabilityPrince RajPas encore d'évaluation

- PGBP Complete TheoryDocument21 pagesPGBP Complete TheoryNirbheek Doyal100% (4)

- Everything you need to know about Statutory CompanyDocument19 pagesEverything you need to know about Statutory CompanyBhanupratap Singh ShekhawatPas encore d'évaluation

- Case Study On Competition LawDocument8 pagesCase Study On Competition LawRitika RitzPas encore d'évaluation

- Income From SalaryDocument66 pagesIncome From SalaryShamika LloydPas encore d'évaluation

- Welfare Measures in A FactoryDocument13 pagesWelfare Measures in A FactoryHavish P D SulliaPas encore d'évaluation

- Income From Other SourcesDocument12 pagesIncome From Other SourcesMuqddas AbbasPas encore d'évaluation

- Employees Provident Fund Act 1952Document43 pagesEmployees Provident Fund Act 1952Manojkumar MohanasundramPas encore d'évaluation

- Tax - Residential Status and Scope of Total IncomeDocument37 pagesTax - Residential Status and Scope of Total IncomeJoshua Griffin100% (1)

- Corporate Law FINALDocument22 pagesCorporate Law FINALAnha RizviPas encore d'évaluation

- Project On Capital GainsDocument19 pagesProject On Capital GainsPrashant MahawarPas encore d'évaluation

- Chapter - 2 Conceptual Framework of DividendDocument36 pagesChapter - 2 Conceptual Framework of DividendMadhavasadasivan PothiyilPas encore d'évaluation

- Powers and Function and Jurisdiction of Competition Commission of IndiaDocument19 pagesPowers and Function and Jurisdiction of Competition Commission of IndiaNAMRATA BHATIAPas encore d'évaluation

- Jayesh AdrDocument24 pagesJayesh AdrSoumya SinhaPas encore d'évaluation

- India's Mega Online Education Hub For Class 9-12 Students, Engineers, Managers, Lawyers and DoctorsDocument32 pagesIndia's Mega Online Education Hub For Class 9-12 Students, Engineers, Managers, Lawyers and Doctorsanupathi mamatha deen dayalPas encore d'évaluation

- 2 Methods of Company Winding-Up ExplainedDocument14 pages2 Methods of Company Winding-Up ExplainedAayushPas encore d'évaluation

- Clinical Report PDFDocument34 pagesClinical Report PDFjanki janiPas encore d'évaluation

- FEMA Act overviewDocument25 pagesFEMA Act overviewSKSAIDINESHPas encore d'évaluation

- Caultimates.com: Income Under Salary HeadDocument142 pagesCaultimates.com: Income Under Salary HeadOnlinePas encore d'évaluation

- Final Draft 1704 Interpleader SuitDocument25 pagesFinal Draft 1704 Interpleader SuitAbhay RajPas encore d'évaluation

- Ankit Tyagi Final Draft Law of Taxation-IDocument13 pagesAnkit Tyagi Final Draft Law of Taxation-IAnkit TyagiPas encore d'évaluation

- Residential Status and Tax Incidence: Dr. Niti SaxenaDocument11 pagesResidential Status and Tax Incidence: Dr. Niti SaxenaYusufPas encore d'évaluation

- Heads of Income Tax Under Income Tax Act, 1961Document15 pagesHeads of Income Tax Under Income Tax Act, 1961Rahul Lahre100% (1)

- Faculty of Law Jamia Millia IslamiaDocument14 pagesFaculty of Law Jamia Millia IslamiaJin KnoxvillePas encore d'évaluation

- The Cyber Regulations Appellate TribunalDocument7 pagesThe Cyber Regulations Appellate TribunalLaxmi SharmaPas encore d'évaluation

- Cartagena Protocol ExplainedDocument15 pagesCartagena Protocol Explainedshivanika singlaPas encore d'évaluation

- Res SubjudiceDocument11 pagesRes SubjudiceSujan Ganesh0% (1)

- IRS Audit Guide For Foreign Insurance TransactionsDocument79 pagesIRS Audit Guide For Foreign Insurance TransactionsSpringer Jones, Enrolled Agent100% (1)

- Understanding Key Income Tax ConceptsDocument94 pagesUnderstanding Key Income Tax ConceptsGopi NathPas encore d'évaluation

- Income Tax Law & Practice Code: BBA-301 Unit - 1: Ms. Manisha Sharma Asst. ProfessorDocument60 pagesIncome Tax Law & Practice Code: BBA-301 Unit - 1: Ms. Manisha Sharma Asst. ProfessorVasu NarangPas encore d'évaluation

- CAREER PLANNING & SUCCESSION STRATEGIESDocument58 pagesCAREER PLANNING & SUCCESSION STRATEGIESJeremy StevensPas encore d'évaluation

- Lesson 5 - Exclusions and Deductions of Income TaxationDocument34 pagesLesson 5 - Exclusions and Deductions of Income TaxationKhu AbenesPas encore d'évaluation

- Manning 2020 June 2020Document3 pagesManning 2020 June 2020SamiPas encore d'évaluation

- Oil Industry Safety: Fatal vs Nonfatal InjuriesDocument4 pagesOil Industry Safety: Fatal vs Nonfatal InjuriesikkiPas encore d'évaluation

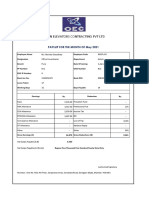

- Orion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Document1 pageOrion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Monika ChoudhariPas encore d'évaluation

- Laddles Discovery Answers (James Island)Document13 pagesLaddles Discovery Answers (James Island)Alex FadoulPas encore d'évaluation

- Employee PerksDocument14 pagesEmployee PerksanniePas encore d'évaluation

- Raymunda Moreno. Roles of SupervisorDocument5 pagesRaymunda Moreno. Roles of Supervisordynamic_edgePas encore d'évaluation

- Literature Review in Internship ReportDocument7 pagesLiterature Review in Internship Reportkmffzlvkg100% (1)

- Social Responsibilities and Good Governance of 24/7 InnDocument13 pagesSocial Responsibilities and Good Governance of 24/7 InnColeen Joy Sebastian PagalingPas encore d'évaluation

- Performance Appraisal and Management - pdf1Document78 pagesPerformance Appraisal and Management - pdf1rohitrpandePas encore d'évaluation

- Recruitment NotesDocument37 pagesRecruitment NotesHARSH VARMAPas encore d'évaluation

- Victorias Social Procurement FrameworkDocument46 pagesVictorias Social Procurement Frameworkhhii85990Pas encore d'évaluation

- Section2-Internal Organisational EnvironmentDocument12 pagesSection2-Internal Organisational EnvironmentAnasha Éttienne-TaylorPas encore d'évaluation

- Chapter 7 Foundations of SelectionDocument17 pagesChapter 7 Foundations of Selectionayda aliPas encore d'évaluation

- Presentation On RecruitmentDocument10 pagesPresentation On RecruitmentRAJ KUMAR MALHOTRAPas encore d'évaluation

- TheSmartManager, SanjayPatro, Feb-Mar 08 - 475Document0 pageTheSmartManager, SanjayPatro, Feb-Mar 08 - 475srin123Pas encore d'évaluation

- Sample - SOP-CompleteDocument46 pagesSample - SOP-CompleteMunish KumarPas encore d'évaluation

- Stages in Career DevelopmentDocument4 pagesStages in Career DevelopmentSajib ChakrabortyPas encore d'évaluation

- Impact of Emotional Intelligence and Organizational Commitment: Testing The Mediatory Role of Job SatisfactionDocument11 pagesImpact of Emotional Intelligence and Organizational Commitment: Testing The Mediatory Role of Job SatisfactionIAEME PublicationPas encore d'évaluation

- EEO Law in PakistanDocument2 pagesEEO Law in PakistanAL-HAMD GROUP100% (1)

- Knowledge ManagementDocument4 pagesKnowledge ManagementSurendaran SathiyanarayananPas encore d'évaluation

- Table of Contents for Sugar Industry ReportDocument28 pagesTable of Contents for Sugar Industry ReportKiran SagarPas encore d'évaluation

- 2011 11 21 Final - DraftDocument172 pages2011 11 21 Final - DraftCREWPas encore d'évaluation

- 1000 Freelancer ProjectsDocument195 pages1000 Freelancer ProjectsMarzouk Eya100% (1)

- Entrepreneurship and Small Business Management Exam 1Document5 pagesEntrepreneurship and Small Business Management Exam 1Rhenz QuipedPas encore d'évaluation

- DPS Assignment Individual MitikuDocument14 pagesDPS Assignment Individual MitikuChaka YohannesPas encore d'évaluation

- HR Strategies of DHL ExpressDocument27 pagesHR Strategies of DHL ExpressAmar Funde100% (1)

- Akanksha ReportDocument61 pagesAkanksha ReportAkanksha Kaushik DubeyPas encore d'évaluation

- EssayDocument3 pagesEssayapi-318197462Pas encore d'évaluation