Vous aimerez peut-être aussi

- Phil Town Rule1Document18 pagesPhil Town Rule1Rajiv Mahajan88% (8)

- Organisational Failure and PathologyDocument4 pagesOrganisational Failure and PathologyVishal Koundal100% (2)

- PB - MIS in Insurance SectorDocument3 pagesPB - MIS in Insurance SectorPriyam BiswasPas encore d'évaluation

- Micro, Macro, and Managerial Economics RelationshipDocument6 pagesMicro, Macro, and Managerial Economics RelationshipJenz Alemana100% (6)

- External MobilityDocument12 pagesExternal MobilityRishabh MishraPas encore d'évaluation

- CASE STUDY - Entrepreneurship DevelopmentDocument3 pagesCASE STUDY - Entrepreneurship DevelopmentBhagwati Chaudhary44% (9)

- UNIT-1 - Managerial Economics (MBA-1st Year)Document22 pagesUNIT-1 - Managerial Economics (MBA-1st Year)Tanya Malviya100% (1)

- Vuoap01 0406 - Mba 201Document17 pagesVuoap01 0406 - Mba 201prayas sarkarPas encore d'évaluation

- Term Sheet For Intercreditor Agreement 1.21Document4 pagesTerm Sheet For Intercreditor Agreement 1.21Helpin HandPas encore d'évaluation

- Mining Services: An Overview of SRK's Services To The Global Mining IndustryDocument40 pagesMining Services: An Overview of SRK's Services To The Global Mining IndustryUmesh Shanmugam100% (1)

- PRTC AUD-1stPB 05.22Document14 pagesPRTC AUD-1stPB 05.22Ciatto SpotifyPas encore d'évaluation

- General Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaDocument137 pagesGeneral Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaMarvin Marciano DiñoPas encore d'évaluation

- Chap 14 - Bret Company (Case Study)Document5 pagesChap 14 - Bret Company (Case Study)Al HiponiaPas encore d'évaluation

- Henkel 2016 Annual ReportDocument202 pagesHenkel 2016 Annual ReportjonnyPas encore d'évaluation

- Financial Management - NotesDocument39 pagesFinancial Management - NotesdollyguptaPas encore d'évaluation

- Grand StrategiesDocument7 pagesGrand StrategiesSeher NazPas encore d'évaluation

- Objectives or Purposes o F Business CommunicationDocument7 pagesObjectives or Purposes o F Business CommunicationAjay Prakash100% (1)

- Scope and Nature of MarketingDocument4 pagesScope and Nature of MarketingAbhijit Dhar100% (1)

- Irll NotesDocument26 pagesIrll NotesKopuri Mastan ReddyPas encore d'évaluation

- Drivers of International BusinessDocument4 pagesDrivers of International Businesskrkr_sharad67% (3)

- Legal & Tax Aspects of BusinessDocument238 pagesLegal & Tax Aspects of BusinessBhavin Mahesh GandhiPas encore d'évaluation

- Hoffers ModelDocument10 pagesHoffers ModelPradnya SurwadePas encore d'évaluation

- 05 Market and Demand AnalysisDocument30 pages05 Market and Demand Analysismussaiyib100% (1)

- Government Influence On Trade and InvestmentDocument11 pagesGovernment Influence On Trade and InvestmentKrunal Maniyar100% (2)

- What Is Industrial ConflictDocument4 pagesWhat Is Industrial Conflictcoolguys235100% (2)

- Research Design Business Research Methods 6th Semester BBA Notes TUDocument13 pagesResearch Design Business Research Methods 6th Semester BBA Notes TUDjay Sly100% (1)

- Marketing Management Notes For MG University MBA First SemesterDocument63 pagesMarketing Management Notes For MG University MBA First SemesterSebin Jose100% (2)

- Study Material Unit 1 CBCRMDocument35 pagesStudy Material Unit 1 CBCRMaruna krishnaPas encore d'évaluation

- OBDocument4 pagesOBDavid Raju Gollapudi33% (3)

- Types Right To StrikeDocument17 pagesTypes Right To StrikeMishika Pandita100% (1)

- 4 Pillars of Corporate Gov.Document3 pages4 Pillars of Corporate Gov.Anita Khan76% (17)

- Investment Management NotesDocument40 pagesInvestment Management NotesSiddharth Ingle100% (1)

- Wages and Salary Administration QuestionsDocument4 pagesWages and Salary Administration Questionssounderajjan25% (4)

- Financial Management Class Notes For BBADocument20 pagesFinancial Management Class Notes For BBASameel Rehman67% (3)

- MIS Basics and MIS Other Academic DisciplinesDocument26 pagesMIS Basics and MIS Other Academic DisciplinesSarikaSaxena100% (1)

- Approaches To Grievance MachineryDocument2 pagesApproaches To Grievance MachinerySumathy S Ramkumar0% (1)

- Buyer Seller DyadDocument6 pagesBuyer Seller DyadSOUMYAJIT KARPas encore d'évaluation

- Strategic Advantage AnalysisDocument21 pagesStrategic Advantage Analysisvaishalic100% (1)

- New Issue MarketDocument15 pagesNew Issue MarketRavi Kumar100% (1)

- Managerial ECONOMICS PPT 1 PDFDocument27 pagesManagerial ECONOMICS PPT 1 PDFJerwin FajardoPas encore d'évaluation

- Chapter Six Marketing and New Venture DevelopmentDocument49 pagesChapter Six Marketing and New Venture DevelopmentAgatPas encore d'évaluation

- Strategic Management PPT by Akshaya KumarDocument23 pagesStrategic Management PPT by Akshaya KumarAkshaya KumarPas encore d'évaluation

- Entrepreneurship Development NotesDocument11 pagesEntrepreneurship Development Notessourav kumar ray100% (1)

- Notes.-Legal Systems. - IIPM. - MBA. & LCP FormDocument17 pagesNotes.-Legal Systems. - IIPM. - MBA. & LCP FormamitkaraliaPas encore d'évaluation

- New Issue MarketDocument13 pagesNew Issue MarketKanivarasi Hercule100% (2)

- Different Levels of StrategyDocument12 pagesDifferent Levels of StrategyELMUNTHIR BEN AMMARPas encore d'évaluation

- Functions of SEBIDocument6 pagesFunctions of SEBIKumar Raghav MauryaPas encore d'évaluation

- Business Ethics and CSR - Own NotesDocument41 pagesBusiness Ethics and CSR - Own NotesPiyush Phapale67% (6)

- Note On Public IssueDocument9 pagesNote On Public IssueKrish KalraPas encore d'évaluation

- Insurance - Methods of Handling RiskDocument2 pagesInsurance - Methods of Handling RiskMohit SharmaPas encore d'évaluation

- Role of State in IRDocument7 pagesRole of State in IRvaniPas encore d'évaluation

- Factors Affect Factors Affecting Working Capitaling Working CapitalDocument24 pagesFactors Affect Factors Affecting Working Capitaling Working Capitalranjita kelageriPas encore d'évaluation

- Corporate Social ResponsibilityDocument18 pagesCorporate Social ResponsibilityPrashant RampuriaPas encore d'évaluation

- The Hot Stove RuleDocument2 pagesThe Hot Stove RuleRahul SarkerPas encore d'évaluation

- Objectives and Functions of IDBI: ObjectiveDocument2 pagesObjectives and Functions of IDBI: ObjectiveParveen SinghPas encore d'évaluation

- Legal Framework of Industrial RelationsDocument18 pagesLegal Framework of Industrial Relationsdeepu0787Pas encore d'évaluation

- Information Technology in RetailDocument17 pagesInformation Technology in RetailMaya RemcyPas encore d'évaluation

- 03 - Prerequisites of Collective BargainingDocument8 pages03 - Prerequisites of Collective BargainingGayatri Dhawan100% (1)

- 03.MS WordDocument30 pages03.MS WordMuruganPas encore d'évaluation

- 7 Main Objectives of A Business FirmDocument17 pages7 Main Objectives of A Business FirmVickyPas encore d'évaluation

- Module VII Profit Mgmt.Document15 pagesModule VII Profit Mgmt.Apoorv BPas encore d'évaluation

- Theory of A Firm ImpDocument8 pagesTheory of A Firm ImpPrajwal JamdapurePas encore d'évaluation

- Conventional Theory of Firm Assumes Profit Maximization Is The Sole Objective of Business FirmsDocument2 pagesConventional Theory of Firm Assumes Profit Maximization Is The Sole Objective of Business FirmsIyer Deepika100% (1)

- Financial ManagementDocument7 pagesFinancial ManagementSarah SarahPas encore d'évaluation

- Williamson's Managerial Discretionary Theory:: I. Expansion of StaffDocument44 pagesWilliamson's Managerial Discretionary Theory:: I. Expansion of StaffAhim Raj JoshiPas encore d'évaluation

- Unit 5Document16 pagesUnit 5mussaiyibPas encore d'évaluation

- GRP 3Document4 pagesGRP 3kkv_phani_varma5396Pas encore d'évaluation

- AS 27pptDocument24 pagesAS 27pptrajvinder kaurPas encore d'évaluation

- Infosys Balance SheetDocument10 pagesInfosys Balance Sheetrajvinder kaurPas encore d'évaluation

- Attitude: Prof Arati KaleDocument30 pagesAttitude: Prof Arati Kalesaru_soodPas encore d'évaluation

- Serives MKTG - Banking Full and FinalDocument31 pagesSerives MKTG - Banking Full and Finalrajvinder kaurPas encore d'évaluation

- Production FunctionsDocument45 pagesProduction Functionsrajvinder kaurPas encore d'évaluation

- PricingDocument25 pagesPricingrajvinder kaurPas encore d'évaluation

- Objectives of A Business FirmDocument10 pagesObjectives of A Business Firmrajvinder kaurPas encore d'évaluation

- Law of DemandDocument28 pagesLaw of Demandrajvinder kaurPas encore d'évaluation

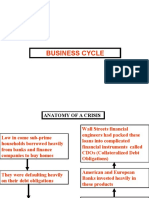

- Business CycleDocument36 pagesBusiness Cyclerajvinder kaurPas encore d'évaluation

- From Economics To Managerial EconomicsDocument46 pagesFrom Economics To Managerial Economicsrajvinder kaurPas encore d'évaluation

- Managerial Economics 1Document7 pagesManagerial Economics 1rajvinder kaurPas encore d'évaluation

- Demand AnalysisDocument42 pagesDemand Analysisrajvinder kaurPas encore d'évaluation

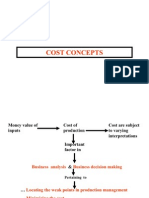

- Cost ConceptsDocument17 pagesCost Conceptsrajvinder kaurPas encore d'évaluation

- Distinction Between Public Sector Undertaking and Private CompanyDocument3 pagesDistinction Between Public Sector Undertaking and Private CompanyArun Kumar SharmaPas encore d'évaluation

- 2023 - FRM - PI - PE2 - 020223 - CleanDocument171 pages2023 - FRM - PI - PE2 - 020223 - CleanRaymond Kwong100% (1)

- Chapter 2 Bank FundDocument31 pagesChapter 2 Bank FundNiloy AhmedPas encore d'évaluation

- Practical Investment Management: Robert A. StrongDocument14 pagesPractical Investment Management: Robert A. Strongkashifali249_8739463Pas encore d'évaluation

- Mehrub ResumeDocument1 pageMehrub ResumeZeehenul IshfaqPas encore d'évaluation

- True / False Questions: Accounting in BusinessDocument101 pagesTrue / False Questions: Accounting in BusinesskiomePas encore d'évaluation

- Trading Chart PatternsDocument32 pagesTrading Chart Patternsadewaleadeshina8957100% (1)

- Declaration 3520228712048Document5 pagesDeclaration 3520228712048hinamuzammil.acaPas encore d'évaluation

- 09 - Chapter 3Document34 pages09 - Chapter 3Aakash SonarPas encore d'évaluation

- Ic-Mineval: Software For The Financial Evaluation of Mineral DepositsDocument67 pagesIc-Mineval: Software For The Financial Evaluation of Mineral DepositstamanimoPas encore d'évaluation

- Tutorial 1 AnswerDocument1 pageTutorial 1 AnswerShinChanPas encore d'évaluation

- Kotak Multicap Fund-SIDDocument122 pagesKotak Multicap Fund-SIDsenthilkumarPas encore d'évaluation

- Cash and Marketable Securities Seatworks PDFDocument3 pagesCash and Marketable Securities Seatworks PDFGirl Lang AkoPas encore d'évaluation

- CBZ Holdings 2019 Annual Report PDFDocument160 pagesCBZ Holdings 2019 Annual Report PDFWebSter NyandoroPas encore d'évaluation

- Ncert Solution Class 11 Accountancy Chapter 10Document68 pagesNcert Solution Class 11 Accountancy Chapter 10Prakal 444Pas encore d'évaluation

- Tata Steel Key Financial Ratios, Tata Steel Financial Statement & AccountsDocument3 pagesTata Steel Key Financial Ratios, Tata Steel Financial Statement & Accountsmohan chouriwarPas encore d'évaluation

- Financial Engineering and Evaluation of New Instruments: Dr. Munawar IqbalDocument29 pagesFinancial Engineering and Evaluation of New Instruments: Dr. Munawar Iqbaloanzar513Pas encore d'évaluation

- India in Stagflation, Not Crisis - Kenneth Rogoff, Harvard Economist - The Economic TimesDocument4 pagesIndia in Stagflation, Not Crisis - Kenneth Rogoff, Harvard Economist - The Economic Timessanits591Pas encore d'évaluation

- WSJ - September 11 2023Document38 pagesWSJ - September 11 2023Rizy BumhPas encore d'évaluation

- Kunjaw UasDocument11 pagesKunjaw UasIvan Katibul FaiziPas encore d'évaluation

- Tutorial 7Document2 pagesTutorial 7It's Bella RobertsonPas encore d'évaluation

- Berle 1947 - Theory of Enterprise Entity PDFDocument17 pagesBerle 1947 - Theory of Enterprise Entity PDFJosiah BalgosPas encore d'évaluation

- ايميلات شركات كتير فى الكويتDocument40 pagesايميلات شركات كتير فى الكويتahmed HOSNYPas encore d'évaluation