Vous aimerez peut-être aussi

- REYES Bar Reviewer On Taxation II (v.3)Document164 pagesREYES Bar Reviewer On Taxation II (v.3)Glory Be93% (14)

- Feu Estate TaxDocument17 pagesFeu Estate Taxlouise carino100% (1)

- Taxation ReviewerDocument145 pagesTaxation ReviewerJingJing Romero95% (95)

- CIR V Central LuzonDocument2 pagesCIR V Central LuzonAgnes FranciscoPas encore d'évaluation

- Bank Balance Sheet Components and ALM OverviewDocument41 pagesBank Balance Sheet Components and ALM Overviewgaurav112011Pas encore d'évaluation

- EXIBIT G - SPA Locally ExecutedDocument3 pagesEXIBIT G - SPA Locally ExecutedMaia CastañedaPas encore d'évaluation

- Multiple Choice Tax ReviewDocument1 pageMultiple Choice Tax ReviewQuasi-Delict89% (18)

- Constellation SoftwareDocument11 pagesConstellation SoftwaregalatimePas encore d'évaluation

- Estate Taxation Guide for Northern CPA ReviewDocument18 pagesEstate Taxation Guide for Northern CPA ReviewJane Oblena100% (1)

- Material Cost PDFDocument45 pagesMaterial Cost PDFtnchsg0% (2)

- Exibit N - Offer To SellDocument3 pagesExibit N - Offer To SellMaia CastañedaPas encore d'évaluation

- Spring 2012 EGT OutlineDocument63 pagesSpring 2012 EGT OutlineJessica Rae FarrisPas encore d'évaluation

- Basic Principles of Taxation Lecture NotesDocument5 pagesBasic Principles of Taxation Lecture NotesabbyPas encore d'évaluation

- Tax2 Ch15 Estate Taxes ReviewerDocument7 pagesTax2 Ch15 Estate Taxes Reviewerlyle_rosePas encore d'évaluation

- Taxation of Individuals QuizzerDocument37 pagesTaxation of Individuals QuizzerCharry Ramos62% (13)

- Taxation Law ReviewerDocument62 pagesTaxation Law ReviewerAdelaine Faith Zerna96% (23)

- Taxation 2Document112 pagesTaxation 2cmv mendoza100% (7)

- Taxation Under The Train Law: 1 - PageDocument30 pagesTaxation Under The Train Law: 1 - PageMae50% (2)

- International Compensation ManagementDocument11 pagesInternational Compensation ManagementMahbub Zaman Refat100% (2)

- Tax 101 Basic Principles LectureDocument7 pagesTax 101 Basic Principles LectureMarcley BataoilPas encore d'évaluation

- No Broad Level Report Options Available For Report Execution Tcode in SAPDocument48 pagesNo Broad Level Report Options Available For Report Execution Tcode in SAPpankajsri68100% (1)

- EXHIBIT K - Non-Exclusive Authority To SellDocument3 pagesEXHIBIT K - Non-Exclusive Authority To SellMaia Castañeda100% (7)

- Taxation History and PrinciplesDocument106 pagesTaxation History and PrinciplesFebe TeleronPas encore d'évaluation

- Financial ManagementDocument254 pagesFinancial Managementkimringine50% (2)

- TAXATION 1 MIDTERMS REVIEWDocument28 pagesTAXATION 1 MIDTERMS REVIEWDenise FranchescaPas encore d'évaluation

- EXIBIT U - Contract To SellDocument5 pagesEXIBIT U - Contract To SellMaia CastañedaPas encore d'évaluation

- TAXATION 1 - KEY PRINCIPLESDocument87 pagesTAXATION 1 - KEY PRINCIPLESVincent John Nacua100% (1)

- General Principles of TaxationDocument14 pagesGeneral Principles of TaxationJulie Ann RosalesPas encore d'évaluation

- Exibit Aa - Doas-UnilateralDocument2 pagesExibit Aa - Doas-UnilateralMaia Castañeda33% (3)

- Gross Estate Tax QuizzerDocument6 pagesGross Estate Tax QuizzerLloyd Sonica100% (1)

- Business and Transfer Taxes Notes: Estate TaxDocument8 pagesBusiness and Transfer Taxes Notes: Estate TaxSugar JumuadPas encore d'évaluation

- Tax Review Q and A Quiz 1 and 2 FinalsDocument19 pagesTax Review Q and A Quiz 1 and 2 FinalsAngel Xavier CalejaPas encore d'évaluation

- Chapter 06 Donor's TaxDocument16 pagesChapter 06 Donor's TaxNikki Bucatcat0% (2)

- Basic Principles of Taxation Atty. Macmod, CPADocument7 pagesBasic Principles of Taxation Atty. Macmod, CPAevaPas encore d'évaluation

- The Inherent Powers of Government and TaxationDocument5 pagesThe Inherent Powers of Government and TaxationElaiza LozanoPas encore d'évaluation

- Tax: TRAIN Illustrative Problems: Long Problem With FormsDocument23 pagesTax: TRAIN Illustrative Problems: Long Problem With FormsNooroddenPas encore d'évaluation

- EXIBIT EE - Certificate of ManagementDocument2 pagesEXIBIT EE - Certificate of ManagementMaia Castañeda50% (2)

- Tax 2 1st Exam 2016 TSNDocument18 pagesTax 2 1st Exam 2016 TSNAure ReidPas encore d'évaluation

- Taxation Principles ExplainedDocument135 pagesTaxation Principles ExplainedCMBDB100% (1)

- Taxation Principles ExplainedDocument10 pagesTaxation Principles ExplainedRommel Mirasol100% (1)

- Succession and Estate Tax ConceptsDocument3 pagesSuccession and Estate Tax ConceptsKim Cristian MaañoPas encore d'évaluation

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoPas encore d'évaluation

- Tax2 Ch15 Estate Taxes ReviewerDocument8 pagesTax2 Ch15 Estate Taxes ReviewerAudrey Orpilla AdajarPas encore d'évaluation

- Bus TaxDocument20 pagesBus TaxDanica CoronelPas encore d'évaluation

- Incotax PDFDocument7 pagesIncotax PDFLara LaquiPas encore d'évaluation

- Atlas Reviewer Transfer and Business Tax p1Document25 pagesAtlas Reviewer Transfer and Business Tax p1ABIGAIL DAYOTPas encore d'évaluation

- Estate Tax Notes LimDocument5 pagesEstate Tax Notes LimAustine Clarese VelascoPas encore d'évaluation

- Econ Jahsmen FinalDocument4 pagesEcon Jahsmen FinalJahsmen NavarroPas encore d'évaluation

- Based On Who CollectsDocument3 pagesBased On Who CollectsRujean Salar AltejarPas encore d'évaluation

- TAXATION ReviewerDocument18 pagesTAXATION ReviewerAyessa GayamoPas encore d'évaluation

- Taxation Basic Principles of Taxation: Atty. Macmod, CpaDocument7 pagesTaxation Basic Principles of Taxation: Atty. Macmod, CpaKrisan Rivera100% (1)

- Taxation Fundamentals NotesDocument3 pagesTaxation Fundamentals Noteslayla scotPas encore d'évaluation

- TX01 General Principles of TaxationDocument9 pagesTX01 General Principles of TaxationAce DesabillePas encore d'évaluation

- Basic Principles of Taxation Atty. Macmod, CPADocument7 pagesBasic Principles of Taxation Atty. Macmod, CPAPAGLINGAYEN, MA. ANGELICAPas encore d'évaluation

- Lesson 1Document17 pagesLesson 1Rachel Mae BardePas encore d'évaluation

- General Principles of Taxation ExplainedDocument9 pagesGeneral Principles of Taxation ExplainedARISPas encore d'évaluation

- Income Tax Summary TulibasDocument66 pagesIncome Tax Summary TulibasVan DahuyagPas encore d'évaluation

- CHAPTER 1 3 Bus - TaxDocument26 pagesCHAPTER 1 3 Bus - TaxMixx MinePas encore d'évaluation

- Tax 1 - Unit 1. Chapter IDocument6 pagesTax 1 - Unit 1. Chapter IJamaica ManilaPas encore d'évaluation

- Chapter 1 General Principles and Concepts of TaxationDocument40 pagesChapter 1 General Principles and Concepts of TaxationArjay AlleraPas encore d'évaluation

- TX01 - General Principles of TaxationDocument9 pagesTX01 - General Principles of TaxationDon XiaoPas encore d'évaluation

- Fundamentals of TaxationDocument13 pagesFundamentals of TaxationKatrina MaglaquiPas encore d'évaluation

- Basic Principles of TaxationDocument55 pagesBasic Principles of TaxationKira LimPas encore d'évaluation

- Tax 2 RevisedDocument17 pagesTax 2 RevisedAmanda ButtkissPas encore d'évaluation

- Reviewer - TaxationDocument2 pagesReviewer - TaxationjatalPas encore d'évaluation

- General Principles of Taxation I. Three Inherent Powers of The StateDocument9 pagesGeneral Principles of Taxation I. Three Inherent Powers of The Statejumawaymichaeljeffrey65Pas encore d'évaluation

- INTAXDocument23 pagesINTAXRainyPas encore d'évaluation

- Inherent Powers of the State ExplainedDocument13 pagesInherent Powers of the State ExplainedMarilyn Perez OlañoPas encore d'évaluation

- Tax Midterm Notes.06.14.22Document15 pagesTax Midterm Notes.06.14.22Aleezah Gertrude RaymundoPas encore d'évaluation

- Taxation by WMGDocument16 pagesTaxation by WMGLimmuel LumbaPas encore d'évaluation

- ESTATE TAX LECTURES Part 1 and 2Document8 pagesESTATE TAX LECTURES Part 1 and 2Riyo Mae MagnoPas encore d'évaluation

- Income Taxation General PrinciplesDocument22 pagesIncome Taxation General PrinciplesashPas encore d'évaluation

- Introduction of Taxation REVIEWERDocument6 pagesIntroduction of Taxation REVIEWERguess WhatPas encore d'évaluation

- Understanding the principles, theories, and classifications of taxationDocument1 pageUnderstanding the principles, theories, and classifications of taxationspaghettiPas encore d'évaluation

- EXIBIT W-2 - Escrow GuaranteeDocument1 pageEXIBIT W-2 - Escrow GuaranteeMaia CastañedaPas encore d'évaluation

- EXIBIT O - Prospect Tripping ConfirmationDocument2 pagesEXIBIT O - Prospect Tripping ConfirmationMaia CastañedaPas encore d'évaluation

- Narration / Voice Over Animation Idea: SceneDocument1 pageNarration / Voice Over Animation Idea: SceneMaia CastañedaPas encore d'évaluation

- Exibit y - Doas-Hse& LotDocument4 pagesExibit y - Doas-Hse& LotMaia CastañedaPas encore d'évaluation

- EXIBIT S - Ofr 2 Purchase-CondoDocument3 pagesEXIBIT S - Ofr 2 Purchase-CondoMaia CastañedaPas encore d'évaluation

- EXIBIT V - Acknowledgment Receipt-DPDocument1 pageEXIBIT V - Acknowledgment Receipt-DPMaia CastañedaPas encore d'évaluation

- EXIBIT UU - Final Expense Report-BuyerDocument3 pagesEXIBIT UU - Final Expense Report-BuyerMaia CastañedaPas encore d'évaluation

- EXIBIT RR - Final Expense Report-SellerDocument2 pagesEXIBIT RR - Final Expense Report-SellerMaia CastañedaPas encore d'évaluation

- Exibit T - Ofr 2 Purchase-H& LDocument3 pagesExibit T - Ofr 2 Purchase-H& LMaia CastañedaPas encore d'évaluation

- EXIBIT MM - Affidavit of CitizenshipDocument1 pageEXIBIT MM - Affidavit of CitizenshipMaia CastañedaPas encore d'évaluation

- EXIBIT TT - Final Expense Report Nuyer NewDocument2 pagesEXIBIT TT - Final Expense Report Nuyer NewMaia CastañedaPas encore d'évaluation

- EXIBIT SS - Final Transmittal of Docs-SellerDocument2 pagesEXIBIT SS - Final Transmittal of Docs-SellerMaia CastañedaPas encore d'évaluation

- EXIBIT R - Client RegistrationDocument2 pagesEXIBIT R - Client RegistrationMaia CastañedaPas encore d'évaluation

- Exibit Q - Extension of AtsDocument3 pagesExibit Q - Extension of AtsMaia CastañedaPas encore d'évaluation

- EXIBIT KK - Acknowledgment Receipt-Full PymtDocument2 pagesEXIBIT KK - Acknowledgment Receipt-Full PymtMaia CastañedaPas encore d'évaluation

- EXIBIT P - Broker's AgreementDocument4 pagesEXIBIT P - Broker's AgreementMaia CastañedaPas encore d'évaluation

- EXIBIT I - Secretary's Cert.Document2 pagesEXIBIT I - Secretary's Cert.Maia Castañeda100% (1)

- EXIBIT J - Excludive Right To SellDocument4 pagesEXIBIT J - Excludive Right To SellMaia CastañedaPas encore d'évaluation

- EXIBIT LL - Bank Commitment Ltr.Document2 pagesEXIBIT LL - Bank Commitment Ltr.Maia CastañedaPas encore d'évaluation

- EXIBIT M - Property ProfileDocument2 pagesEXIBIT M - Property ProfileMaia CastañedaPas encore d'évaluation

- EXIBIT L - Secretary's Cert.-AtsDocument2 pagesEXIBIT L - Secretary's Cert.-AtsMaia CastañedaPas encore d'évaluation

- EXIBIT A - Property Inspection ChecklistDocument3 pagesEXIBIT A - Property Inspection ChecklistMaia CastañedaPas encore d'évaluation

- Escrow Agmt. AnnexDocument1 pageEscrow Agmt. AnnexMaia CastañedaPas encore d'évaluation

- Escrow Agmt. AnnexDocument1 pageEscrow Agmt. AnnexMaia CastañedaPas encore d'évaluation

- WGU CMO1 Pre-Assessment Cost Accounting 44 MCQsDocument11 pagesWGU CMO1 Pre-Assessment Cost Accounting 44 MCQsWaqar AhmadPas encore d'évaluation

- Ben Zuccolini - s1101113 - DissertationDocument155 pagesBen Zuccolini - s1101113 - DissertationMohasifPas encore d'évaluation

- Astro TalkDocument24 pagesAstro TalkAteet RaiPas encore d'évaluation

- Exclusive Artist AgreementDocument9 pagesExclusive Artist AgreementSamuel Kagoru GichuruPas encore d'évaluation

- Certain Government Payments: Copy B For RecipientDocument2 pagesCertain Government Payments: Copy B For RecipientDylan Bizier-Conley100% (1)

- Tax On IndividualsDocument9 pagesTax On IndividualsshakiraPas encore d'évaluation

- Patent Infringement Damages - A Brief Summary - Articles - FinneganDocument14 pagesPatent Infringement Damages - A Brief Summary - Articles - FinneganneelgalaPas encore d'évaluation

- Depreciation, ProvisionDocument37 pagesDepreciation, ProvisionSandhyaSharma100% (1)

- TBCH 12Document16 pagesTBCH 12bernandaz123Pas encore d'évaluation

- Magadh University BBM 2ND YEAR QUESTIONSDocument13 pagesMagadh University BBM 2ND YEAR QUESTIONSSuryansh SinghPas encore d'évaluation

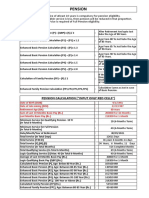

- Pension and Other Retirement BenifitsDocument8 pagesPension and Other Retirement BenifitsVikas GuptaPas encore d'évaluation

- A Brown vs. CIRDocument11 pagesA Brown vs. CIRKwini RojanoPas encore d'évaluation

- Basic Method For Making Economy Study NotesDocument3 pagesBasic Method For Making Economy Study NotesMichael DantogPas encore d'évaluation

- Pre-Feasibility Study on UPS and Stabilizer Assembling UnitDocument23 pagesPre-Feasibility Study on UPS and Stabilizer Assembling UnitRaza Un NabiPas encore d'évaluation

- Acknowledgement Fy 2020-21Document1 pageAcknowledgement Fy 2020-21Prajwal ShettyPas encore d'évaluation

- Pharma Industry Growth and Biovail ScandalDocument7 pagesPharma Industry Growth and Biovail ScandalimeldafebrinatPas encore d'évaluation

- Property Cases BachrachDocument5 pagesProperty Cases BachrachDaniela Erika Beredo InandanPas encore d'évaluation

- Cash Discount: What Is A Cash Discount? Definition of Cash DiscountDocument12 pagesCash Discount: What Is A Cash Discount? Definition of Cash DiscountHumanityPas encore d'évaluation

- Finance Lease ReviewerDocument9 pagesFinance Lease Reviewerian_dazoPas encore d'évaluation

- Accounting Theory: Case StudyDocument5 pagesAccounting Theory: Case StudyKurnia Dwi RachmanPas encore d'évaluation

- CH 23Document81 pagesCH 23rara mirantiPas encore d'évaluation

- DocumentDocument5 pagesDocumentmaxz100% (1)