Vous aimerez peut-être aussi

- Corporate Finance Formulas: A Simple IntroductionD'EverandCorporate Finance Formulas: A Simple IntroductionÉvaluation : 4 sur 5 étoiles4/5 (8)

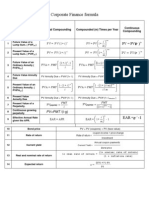

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Modern School For SaxophoneDocument23 pagesModern School For SaxophoneAllen Demiter65% (23)

- National Football League FRC 2000 Sol SRGBDocument33 pagesNational Football League FRC 2000 Sol SRGBMick StukesPas encore d'évaluation

- Knee JointDocument28 pagesKnee JointRaj Shekhar Singh100% (1)

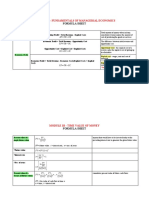

- Time Value of Money Cheat Sheet: by ViaDocument3 pagesTime Value of Money Cheat Sheet: by ViaTechbotix AppsPas encore d'évaluation

- Cheat Sheet FinanceDocument1 pageCheat Sheet FinanceGhitaPas encore d'évaluation

- Formula Sheet Corporate Finance (COF) : Stockholm Business SchoolDocument6 pagesFormula Sheet Corporate Finance (COF) : Stockholm Business SchoolLinus AhlgrenPas encore d'évaluation

- Mathematical Formulas for Economics and Business: A Simple IntroductionD'EverandMathematical Formulas for Economics and Business: A Simple IntroductionÉvaluation : 4 sur 5 étoiles4/5 (4)

- 2016 IT - Sheilding Guide PDFDocument40 pages2016 IT - Sheilding Guide PDFlazarosPas encore d'évaluation

- Cyclic MeditationDocument8 pagesCyclic MeditationSatadal GuptaPas encore d'évaluation

- Dec JanDocument6 pagesDec Janmadhujayan100% (1)

- 2022 Level I Key Facts and Formulas SheetDocument13 pages2022 Level I Key Facts and Formulas Sheetayesha ansari100% (2)

- Exotic DVM 11 3 CompleteDocument12 pagesExotic DVM 11 3 CompleteLuc CardPas encore d'évaluation

- Union Test Prep Nclex Study GuideDocument115 pagesUnion Test Prep Nclex Study GuideBradburn Nursing100% (2)

- Cong ThucDocument12 pagesCong ThucGiang Thái HươngPas encore d'évaluation

- 365+careers Formula+Sheet PART+1Document27 pages365+careers Formula+Sheet PART+1Narmin MirzayevaPas encore d'évaluation

- Quantitative MethodsDocument9 pagesQuantitative Methodsumushtaq005Pas encore d'évaluation

- Nataliemoore Time Value of MoneyDocument4 pagesNataliemoore Time Value of MoneyMaurice AgbayaniPas encore d'évaluation

- FIN222 Equations NotesDocument49 pagesFIN222 Equations NotesSotiris HarisPas encore d'évaluation

- CH 2Document6 pagesCH 2Hemant GoyalPas encore d'évaluation

- FINA 1310 - Lecture 3 NotesDocument6 pagesFINA 1310 - Lecture 3 NotesAayushi ReddyPas encore d'évaluation

- Corporate Finance Equations NotesDocument4 pagesCorporate Finance Equations NotesSotiris HarisPas encore d'évaluation

- Lecture NotesDocument2 pagesLecture Notesbinhvn16.sicPas encore d'évaluation

- Finanical Management Ch4Document60 pagesFinanical Management Ch4Chucky ChungPas encore d'évaluation

- RP - CF1 - Time Value of MoneyDocument28 pagesRP - CF1 - Time Value of MoneySamyu KPas encore d'évaluation

- Ch. 5 The Time Value of Money: 5.1. Future Values and Compound InterestDocument2 pagesCh. 5 The Time Value of Money: 5.1. Future Values and Compound InterestShahid NaseemPas encore d'évaluation

- Formula Sheet (Time Value of Money)Document3 pagesFormula Sheet (Time Value of Money)Allan CabreraPas encore d'évaluation

- Valuing Projects and FirmsDocument1 pageValuing Projects and FirmsKevin KevPas encore d'évaluation

- Icfai FM Time Value of Money Ch. IiiDocument13 pagesIcfai FM Time Value of Money Ch. Iiiapi-3757629100% (3)

- Finance - Time Value of MoneyDocument2 pagesFinance - Time Value of MoneyMaria Inês AzevedoPas encore d'évaluation

- Appendix A: Formula Sheet: The Following Are Useful Formulae 1. Simple Interest FormulaDocument53 pagesAppendix A: Formula Sheet: The Following Are Useful Formulae 1. Simple Interest FormulasilentPas encore d'évaluation

- TVM GSNDocument35 pagesTVM GSNM.MONIKAPas encore d'évaluation

- Module 2 Time Value of MoneyDocument7 pagesModule 2 Time Value of MoneyZaid Ismail ShahPas encore d'évaluation

- L1 QM01 - Summary 3 (2023)Document3 pagesL1 QM01 - Summary 3 (2023)sarthak sanwalPas encore d'évaluation

- Financial Management (MBA 511E) Assignment # 2: Nowsheen Noor ID # 1921251Document2 pagesFinancial Management (MBA 511E) Assignment # 2: Nowsheen Noor ID # 1921251Nowsheen NoorPas encore d'évaluation

- PFM15e IM CH05Document33 pagesPFM15e IM CH05Daniel HakimPas encore d'évaluation

- Time Value of Money (Part 2)Document17 pagesTime Value of Money (Part 2)Claudine DuhapaPas encore d'évaluation

- Time Value of Money: Suggested Readings: Chapter 3, Van Horne / DhamijaDocument18 pagesTime Value of Money: Suggested Readings: Chapter 3, Van Horne / DhamijaSaurabh ChawlaPas encore d'évaluation

- Chapter 6Document3 pagesChapter 6NHƯ NGUYỄN LÂM TÂMPas encore d'évaluation

- Corporate Finance Professional Certificate MOOC: Quick Reference GuideDocument1 pageCorporate Finance Professional Certificate MOOC: Quick Reference GuideShivani AgarwalPas encore d'évaluation

- MAF101 Formula Sheet-2010TR1Document2 pagesMAF101 Formula Sheet-2010TR1Ann VuPas encore d'évaluation

- Formula Time Value of MoneyDocument2 pagesFormula Time Value of MoneySaifur R. SabbirPas encore d'évaluation

- Time Value of MoneyDocument3 pagesTime Value of MoneyVishnupriya PremkumarPas encore d'évaluation

- FM FormulasDocument24 pagesFM FormulasMd. Nafiz ShahrierPas encore d'évaluation

- Summary of Formulas For Time Value of MoneyDocument3 pagesSummary of Formulas For Time Value of MoneyMarilyn Varquez100% (1)

- 2.lecture TVMDocument60 pages2.lecture TVMfurqankhalid1218Pas encore d'évaluation

- Ema Ge Berk CF 2GE SG 04Document13 pagesEma Ge Berk CF 2GE SG 04Duygu ÇınarPas encore d'évaluation

- Module 1 - Basic Finance ConceptsDocument1 pageModule 1 - Basic Finance ConceptsJeniffer FrançaPas encore d'évaluation

- Present Value and Future Value: Finance: Time Value of MoneyDocument11 pagesPresent Value and Future Value: Finance: Time Value of MoneyTes DudtePas encore d'évaluation

- FV PV: LN LN (1)Document2 pagesFV PV: LN LN (1)Danneek BillingsPas encore d'évaluation

- Tvom PDFDocument16 pagesTvom PDFgoyal_khushbu88Pas encore d'évaluation

- BCH-503-SM04time ValueDocument67 pagesBCH-503-SM04time Valuesugandh bajaj100% (1)

- Corporate Finance and Formulas and Cheat Sheet Finance 300Document4 pagesCorporate Finance and Formulas and Cheat Sheet Finance 300quỳnh anh lươngPas encore d'évaluation

- Time Value OF MoneyDocument16 pagesTime Value OF MoneyKomal AgarwalPas encore d'évaluation

- T3 FormulasDocument9 pagesT3 FormulasmartinPas encore d'évaluation

- List of Corporate Finance FormulasDocument9 pagesList of Corporate Finance FormulasYoungRedPas encore d'évaluation

- CA5102 Q1 FORMULA SHEETDocument12 pagesCA5102 Q1 FORMULA SHEETDyra Mae OmegaPas encore d'évaluation

- Test EdiDocument2 pagesTest EdiHeba AbdullahPas encore d'évaluation

- Present Value of A PerpetuityDocument1 pagePresent Value of A PerpetuityKevin KevPas encore d'évaluation

- Time Value of Money ReviewerDocument1 pageTime Value of Money ReviewerCJ IbalePas encore d'évaluation

- Chapter 5Document3 pagesChapter 5Jayesh DesaiPas encore d'évaluation

- Topic 2-Time Value of MoneyDocument38 pagesTopic 2-Time Value of MoneyK61CAF Tạ Thảo VânPas encore d'évaluation

- Test 1Document28 pagesTest 1Joseph J. AssafPas encore d'évaluation

- Handbook of Capital Recovery (CR) Factors: European EditionD'EverandHandbook of Capital Recovery (CR) Factors: European EditionPas encore d'évaluation

- RMC 102-2017 HighlightsDocument3 pagesRMC 102-2017 HighlightsmmeeeowwPas encore d'évaluation

- I I I I: Peroxid.Q!Document2 pagesI I I I: Peroxid.Q!Diego PradelPas encore d'évaluation

- Siemens Rapidlab 248, 348, 840, 845, 850, 855, 860, 865: Reagents & ControlsDocument2 pagesSiemens Rapidlab 248, 348, 840, 845, 850, 855, 860, 865: Reagents & ControlsJuan Carlos CrespoPas encore d'évaluation

- Assignment 4Document5 pagesAssignment 4Hafiz AhmadPas encore d'évaluation

- Module6 Quiz1Document4 pagesModule6 Quiz1karthik1555Pas encore d'évaluation

- Recruitment SelectionDocument11 pagesRecruitment SelectionMOHAMMED KHAYYUMPas encore d'évaluation

- E-Versuri Ro - Rihana - UmbrelaDocument2 pagesE-Versuri Ro - Rihana - Umbrelaanon-821253100% (1)

- Grade 9 Science Biology 1 DLPDocument13 pagesGrade 9 Science Biology 1 DLPManongdo AllanPas encore d'évaluation

- Numerical Modelling and Design of Electrical DevicesDocument69 pagesNumerical Modelling and Design of Electrical Devicesfabrice mellantPas encore d'évaluation

- Research 093502Document8 pagesResearch 093502Chrlszjhon Sales SuguitanPas encore d'évaluation

- A Review of Service Quality ModelsDocument8 pagesA Review of Service Quality ModelsJimmiJini100% (1)

- Building and Structural Construction N6 T1 2024 T2Document9 pagesBuilding and Structural Construction N6 T1 2024 T2FrancePas encore d'évaluation

- Ajmera - Treon - FF - R4 - 13-11-17 FinalDocument45 pagesAjmera - Treon - FF - R4 - 13-11-17 FinalNikita KadamPas encore d'évaluation

- Google Tools: Reggie Luther Tracsoft, Inc. 706-568-4133Document23 pagesGoogle Tools: Reggie Luther Tracsoft, Inc. 706-568-4133nbaghrechaPas encore d'évaluation

- Chemistry Investigatory Project (R)Document23 pagesChemistry Investigatory Project (R)BhagyashreePas encore d'évaluation

- Csu Cep Professional Dispositions 1Document6 pagesCsu Cep Professional Dispositions 1api-502440235Pas encore d'évaluation

- Focus Edition From GC: Phosphate Bonded Investments For C&B TechniquesDocument35 pagesFocus Edition From GC: Phosphate Bonded Investments For C&B TechniquesAlexis De Jesus FernandezPas encore d'évaluation

- ZygalDocument22 pagesZygalShubham KandiPas encore d'évaluation

- Curriculum Guide Ay 2021-2022: Dr. Gloria Lacson Foundation Colleges, IncDocument9 pagesCurriculum Guide Ay 2021-2022: Dr. Gloria Lacson Foundation Colleges, IncJean Marie Itang GarciaPas encore d'évaluation

- Water Pump 250 Hrs Service No Unit: Date: HM: ShiftDocument8 pagesWater Pump 250 Hrs Service No Unit: Date: HM: ShiftTLK ChannelPas encore d'évaluation

- Acc116 Dec 2022 - Q - Test 1Document6 pagesAcc116 Dec 2022 - Q - Test 12022825274100% (1)

- DS Agile - Enm - C6pDocument358 pagesDS Agile - Enm - C6pABDERRAHMANE JAFPas encore d'évaluation