Vous aimerez peut-être aussi

- Chemistry AOS1 Unit 3 NotesDocument34 pagesChemistry AOS1 Unit 3 NotesAnonymous oqlnO8e0% (1)

- Cambridge International AS and A Level Physics: Paper 5 - Planning, Analysis and EvaluationDocument34 pagesCambridge International AS and A Level Physics: Paper 5 - Planning, Analysis and EvaluationZelegans Lynn100% (1)

- CA Final SFM Theory NotesDocument73 pagesCA Final SFM Theory NotesCA Rishabh DaiyaPas encore d'évaluation

- Chemistry Unit 3 Student GuideDocument28 pagesChemistry Unit 3 Student GuideApollo WongPas encore d'évaluation

- Ch2 Atoms&Molecules MolesDocument23 pagesCh2 Atoms&Molecules MolesFlorinel BaietelPas encore d'évaluation

- 2013 Sample QuestionsDocument262 pages2013 Sample QuestionsNorhafiza RoslanPas encore d'évaluation

- Cie Igcse Physics Chapter 4 2023 OnwDocument23 pagesCie Igcse Physics Chapter 4 2023 OnwZeinab ElkholyPas encore d'évaluation

- Personal Finance Canadian 7th Edition Kapoor Solutions ManualDocument27 pagesPersonal Finance Canadian 7th Edition Kapoor Solutions Manualischiummargrave80ep100% (26)

- BFIN Week 11-20Document14 pagesBFIN Week 11-20KingDyther Velasco92% (13)

- CFP Retirement Planning Study Notes SampleDocument35 pagesCFP Retirement Planning Study Notes SampleMeenakshi100% (1)

- Essay Synoptic e Book PDFDocument64 pagesEssay Synoptic e Book PDFChandrasekaran SubramaniamPas encore d'évaluation

- Vol 4 - Credit Management (General)Document353 pagesVol 4 - Credit Management (General)Neelesh KumarPas encore d'évaluation

- Determining Enthalpy of Chemical ReactionDocument5 pagesDetermining Enthalpy of Chemical ReactionCristian AlamosPas encore d'évaluation

- PDF PDFDocument80 pagesPDF PDFAnirudh Makhana100% (1)

- Practical SkillsDocument64 pagesPractical Skillsraghava12345650% (2)

- Enzymes (AS Level Bio)Document23 pagesEnzymes (AS Level Bio)DrMufaddal RampurwalaPas encore d'évaluation

- Student Edexce Moles Workbook Unit 1 PDFDocument112 pagesStudent Edexce Moles Workbook Unit 1 PDFdhawana20% (1)

- Getting Started Guide PDFDocument23 pagesGetting Started Guide PDFZafir RahmanPas encore d'évaluation

- BiologyDocument21 pagesBiologyTallyPas encore d'évaluation

- CasesDocument18 pagesCasesrosebmendozaPas encore d'évaluation

- OCC Interest Rate RiskDocument74 pagesOCC Interest Rate RiskSara HumayunPas encore d'évaluation

- J00001 Oxford Int AS and A-Level Biology Specification WEB PDFDocument46 pagesJ00001 Oxford Int AS and A-Level Biology Specification WEB PDFPakistan English AcademyPas encore d'évaluation

- CP 5 - Investigating The Rates of Hydrolysis of HalogenoalkanesDocument2 pagesCP 5 - Investigating The Rates of Hydrolysis of HalogenoalkanesPOPPas encore d'évaluation

- Mathematics of InvestmentsDocument8 pagesMathematics of InvestmentsMathew EsparragoPas encore d'évaluation

- Edexcel A Level 2 Biology Answers Combined FINAL PDFDocument71 pagesEdexcel A Level 2 Biology Answers Combined FINAL PDFbgtes123Pas encore d'évaluation

- As Chemistry Edexcel Past PapersDocument2 pagesAs Chemistry Edexcel Past PaperszohrabianPas encore d'évaluation

- IAL Chemistry 2018 Data Booklet Issue 1 March 2019Document12 pagesIAL Chemistry 2018 Data Booklet Issue 1 March 2019Romeo ChapolaPas encore d'évaluation

- SNAB Biology - Mark Scheme June 09Document72 pagesSNAB Biology - Mark Scheme June 09Izzat Azmeer Ahmad0% (1)

- Forces and Collisions Particle Motion ProblemsDocument4 pagesForces and Collisions Particle Motion ProblemsAbdullah Al Sakib50% (2)

- Biology: Pearson Edexcel GCEDocument8 pagesBiology: Pearson Edexcel GCEyat yat szePas encore d'évaluation

- GCE Physics Topic Test 1Document40 pagesGCE Physics Topic Test 1刘奇Pas encore d'évaluation

- Chemistry Unit 4 Notes: 4.1 Rates of ReactionsDocument36 pagesChemistry Unit 4 Notes: 4.1 Rates of ReactionssarawongPas encore d'évaluation

- A and As Level Physics Syllabus 2010Document72 pagesA and As Level Physics Syllabus 2010amachqPas encore d'évaluation

- A2 ChemDocument81 pagesA2 ChemJana Mohamed100% (1)

- IAL Science GuideDocument16 pagesIAL Science GuideBekhiet AhmedPas encore d'évaluation

- GCE Biology Unit 6 TSM Final (Unit 6 Guide and Examples From Edexcel)Document76 pagesGCE Biology Unit 6 TSM Final (Unit 6 Guide and Examples From Edexcel)razoraz90% (10)

- Edexcel IAL As Physics Revision Guide Unit 1ADocument54 pagesEdexcel IAL As Physics Revision Guide Unit 1ATHE PSYCOPas encore d'évaluation

- GCE Physics Internal AssessmentDocument198 pagesGCE Physics Internal AssessmentLegacyGrade1280% (5)

- As Practical Skills HandbookDocument62 pagesAs Practical Skills HandbookChiwe Thando MatutaPas encore d'évaluation

- Lower Secondary SpecDocument46 pagesLower Secondary SpectharangaPas encore d'évaluation

- Topic 12 Entropy-Energetics Chemistry Ial EdexcelDocument26 pagesTopic 12 Entropy-Energetics Chemistry Ial EdexcelZubanaPas encore d'évaluation

- QQQ - Pureyr1 - Chapter 7 - Binomial Expansion (V2) : Total Marks: 17Document2 pagesQQQ - Pureyr1 - Chapter 7 - Binomial Expansion (V2) : Total Marks: 17Mapo MarkPas encore d'évaluation

- Unit 1 May19 Till Jan21Document299 pagesUnit 1 May19 Till Jan21Wael TareqPas encore d'évaluation

- 2 2 2 Bonding and StructureDocument7 pages2 2 2 Bonding and StructureifratsubhaPas encore d'évaluation

- BiologyDocument76 pagesBiologycabdifataxPas encore d'évaluation

- AQA-synoptic Essay Marking GuidelinesDocument13 pagesAQA-synoptic Essay Marking GuidelinesSarah HarleyPas encore d'évaluation

- Cambridge International AS & A Level: Mathematics 9709/42Document16 pagesCambridge International AS & A Level: Mathematics 9709/42JahangeerPas encore d'évaluation

- Biology Unit 4 PDFDocument41 pagesBiology Unit 4 PDFsammam mahdi samiPas encore d'évaluation

- Chemistry: Preparing For Key Stage 4 SuccessDocument9 pagesChemistry: Preparing For Key Stage 4 SuccessPaul0% (1)

- IAL Chemistry Data Booklet Issue 3Document35 pagesIAL Chemistry Data Booklet Issue 3jeeshan sayed0% (1)

- Naming Covalent CompoundsDocument6 pagesNaming Covalent Compoundsapi-296446442Pas encore d'évaluation

- DefinitionsDocument6 pagesDefinitionsali ahsan khanPas encore d'évaluation

- 3.2 Carbohydrates Lipids Proteins WORDDocument6 pages3.2 Carbohydrates Lipids Proteins WORDCaitlin Barrett100% (1)

- Longman11-14Chemistry StudentBook9781408231081 Chapter3 PDFDocument24 pagesLongman11-14Chemistry StudentBook9781408231081 Chapter3 PDFNermeinKhattabPas encore d'évaluation

- Stem CellsDocument35 pagesStem Cellshari ilman toni100% (1)

- Edexcel A-Level Chemistry Redox I NotesDocument6 pagesEdexcel A-Level Chemistry Redox I NotesttjjjPas encore d'évaluation

- Topic-5A (Homework) PDFDocument5 pagesTopic-5A (Homework) PDFShayna NaserPas encore d'évaluation

- Summary Notes - Topic 5 Edexcel (A) Biology A-LevelDocument6 pagesSummary Notes - Topic 5 Edexcel (A) Biology A-LevelAhmad MohdPas encore d'évaluation

- June 2019 (IAL) QP - Unit 4 Edexcel Economics A-LevelDocument44 pagesJune 2019 (IAL) QP - Unit 4 Edexcel Economics A-LevelFahad FarhanPas encore d'évaluation

- Mithun's Physics Revision Notes (Unit 1)Document6 pagesMithun's Physics Revision Notes (Unit 1)Mithun Dev SabaratnamPas encore d'évaluation

- 9701 w13 QP 2Document36 pages9701 w13 QP 2hui1430% (1)

- As and A Level Biology B Core Practical 15 Sampling Methods (Student, Teacher, Technician Worksheets)Document7 pagesAs and A Level Biology B Core Practical 15 Sampling Methods (Student, Teacher, Technician Worksheets)Zoe NyawiraPas encore d'évaluation

- Some Problems of Chemical Kinetics and Reactivity: Volume 1D'EverandSome Problems of Chemical Kinetics and Reactivity: Volume 1Pas encore d'évaluation

- 6PH01 May June 2009Document24 pages6PH01 May June 2009Ghaleb W. MihyarPas encore d'évaluation

- Physics Unit 1 6PH01 January 2010 ERDocument22 pagesPhysics Unit 1 6PH01 January 2010 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Jan 2011 Unit 1 EdexcelDocument24 pagesPhysics Jan 2011 Unit 1 EdexcelRatna ChowdhryPas encore d'évaluation

- Physics Unit 7 6PH07 January 2010 ERDocument12 pagesPhysics Unit 7 6PH07 January 2010 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 7 6PH07 January 2011 ERDocument18 pagesPhysics Unit 7 6PH07 January 2011 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 1 6PH01 January 2011 ERDocument38 pagesPhysics Unit 1 6PH01 January 2011 ERDaniyal SiddiquiPas encore d'évaluation

- Physics 2011 January Unit 3Document16 pagesPhysics 2011 January Unit 3Prasitha RushenPas encore d'évaluation

- 6PH04 01 Que 20110127Document24 pages6PH04 01 Que 20110127Shabbir H. KhanPas encore d'évaluation

- Further Pure 1 June 2010 MSDocument14 pagesFurther Pure 1 June 2010 MSDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 4 6PH04 January 2010 ERDocument14 pagesPhysics Unit 4 6PH04 January 2010 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 4 6PH04 June 2010 ERDocument18 pagesPhysics Unit 4 6PH04 June 2010 ERDaniyal SiddiquiPas encore d'évaluation

- FP2 2010Document24 pagesFP2 2010Ian SipinPas encore d'évaluation

- Physics Unit 5 6PH05 January 2011 ERDocument28 pagesPhysics Unit 5 6PH05 January 2011 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 4 6PH04 January 2011 ERDocument40 pagesPhysics Unit 4 6PH04 January 2011 ERDaniyal SiddiquiPas encore d'évaluation

- 6668 - 01 - Further Pure Mathematics FP2Document12 pages6668 - 01 - Further Pure Mathematics FP2Qingyi WangPas encore d'évaluation

- C4 June 2008Document28 pagesC4 June 2008redkyungjinPas encore d'évaluation

- FP2 - June 2009 PaperDocument28 pagesFP2 - June 2009 PaperchequillasPas encore d'évaluation

- 2011 Jan M1 Edexcel Exam PaperDocument24 pages2011 Jan M1 Edexcel Exam PaperkarammyPas encore d'évaluation

- Physics Unit 1 6PH01 & Unit 2 6PH02 June 2009 MSDocument27 pagesPhysics Unit 1 6PH01 & Unit 2 6PH02 June 2009 MSDaniyal SiddiquiPas encore d'évaluation

- Edexcel GCE January 2010 FP1 (New Syllabus) Question PaperDocument24 pagesEdexcel GCE January 2010 FP1 (New Syllabus) Question PapergerikaalhuPas encore d'évaluation

- Edexcel GCE January 2010 FP1 (New Syllabus) Marking SchemeDocument12 pagesEdexcel GCE January 2010 FP1 (New Syllabus) Marking SchemegerikaalhuPas encore d'évaluation

- Physics Unit 2 6PH02 January 2011 ERDocument30 pagesPhysics Unit 2 6PH02 January 2011 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 1 6PH01 & Unit 2 6PH02 January 2009 ERDocument16 pagesPhysics Unit 1 6PH01 & Unit 2 6PH02 January 2009 ERDaniyal Siddiqui0% (1)

- 2011 Jan M1 Edexcel Exam PaperDocument24 pages2011 Jan M1 Edexcel Exam PaperkarammyPas encore d'évaluation

- Accounts Unit 2 6002/01 Question Paper & Source Booklet June 2010Document52 pagesAccounts Unit 2 6002/01 Question Paper & Source Booklet June 2010Daniyal SiddiquiPas encore d'évaluation

- Accounts Unit 2 6002/01 Examiner Report June 2010Document8 pagesAccounts Unit 2 6002/01 Examiner Report June 2010Daniyal SiddiquiPas encore d'évaluation

- Physics Unit 1 6PH01 & Unit 2 6PH02 June 2009 ERDocument56 pagesPhysics Unit 1 6PH01 & Unit 2 6PH02 June 2009 ERDaniyal SiddiquiPas encore d'évaluation

- Physics Unit 2 6PH02 January 2010 ERDocument20 pagesPhysics Unit 2 6PH02 January 2010 ERDaniyal SiddiquiPas encore d'évaluation

- Unit 2 Physics - May 2009Document24 pagesUnit 2 Physics - May 2009Tariq DaasPas encore d'évaluation

- Land Acquisition Act 1984Document25 pagesLand Acquisition Act 1984vipvikramPas encore d'évaluation

- Effective Interest RateDocument3 pagesEffective Interest Ratetimothy454Pas encore d'évaluation

- TVM Present Value Calculations & Investment DecisionsDocument2 pagesTVM Present Value Calculations & Investment Decisionsangelavani_16Pas encore d'évaluation

- Toa 41 42 PDFDocument22 pagesToa 41 42 PDFspur iousPas encore d'évaluation

- JainDocument9 pagesJainkamal joshiPas encore d'évaluation

- Mind-Map - Marathon NotesDocument10 pagesMind-Map - Marathon NotesMd. Sohail Raza100% (1)

- Construction Loan Repayment ScheduleDocument3 pagesConstruction Loan Repayment ScheduleMahesh JhaPas encore d'évaluation

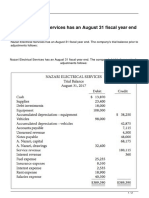

- Nazari Electrical Services Has An August 31 Fiscal Year EndDocument2 pagesNazari Electrical Services Has An August 31 Fiscal Year EndCharlottePas encore d'évaluation

- EC1002 ZA Part1 PDFDocument9 pagesEC1002 ZA Part1 PDFAmanda CheamPas encore d'évaluation

- Liabilities and EquityDocument23 pagesLiabilities and Equityadmiral spongebobPas encore d'évaluation

- B V M Engineering College Vallabh VidyanagarDocument9 pagesB V M Engineering College Vallabh VidyanagarShish DattaPas encore d'évaluation

- Engaging Activity Unit 4 Financial InstitutionDocument2 pagesEngaging Activity Unit 4 Financial InstitutionMary Justine ManaloPas encore d'évaluation

- Post Office Savings SchemesDocument5 pagesPost Office Savings SchemeslucknowhubPas encore d'évaluation

- Types of Borrowers and Lending ServicesDocument52 pagesTypes of Borrowers and Lending Servicesgodfrey grizzlyPas encore d'évaluation

- PRC 5 Chap 4 SlidesDocument51 pagesPRC 5 Chap 4 SlidesSyedMaazAliPas encore d'évaluation

- REPAYMENT SCHEDULEDocument2 pagesREPAYMENT SCHEDULEZeubayr KabliPas encore d'évaluation

- Corporation Code Up To 45Document56 pagesCorporation Code Up To 45Jasmine Montero-GaribayPas encore d'évaluation

- Multinational Business Finance 15th Edition Eiteman Test BankDocument14 pagesMultinational Business Finance 15th Edition Eiteman Test Bankmisavizebrigadeuieix100% (26)

- Allied Bank (M) SDN BHD V Yau Jiok Hua - (20Document14 pagesAllied Bank (M) SDN BHD V Yau Jiok Hua - (20Huishien QuayPas encore d'évaluation

- DuPont AnalysisDocument4 pagesDuPont AnalysisYogi BearPas encore d'évaluation

- FR - Study Hub - Flash CardsDocument14 pagesFR - Study Hub - Flash CardsFalguni PurohitPas encore d'évaluation

- Ajanta Pharma LTD.: Credit Analysis & Research LimitedDocument7 pagesAjanta Pharma LTD.: Credit Analysis & Research Limitedaadsare11287Pas encore d'évaluation