Vous aimerez peut-être aussi

- European Governance and the Role of the State in Economic DevelopmentDocument14 pagesEuropean Governance and the Role of the State in Economic Developmentluci_luci43% (7)

- Jewelers Bench PlansDocument1 pageJewelers Bench Planscristi6923Pas encore d'évaluation

- Plant Manager's Office - LatestDocument1 pagePlant Manager's Office - LatestAzel Mica GarciaPas encore d'évaluation

- Groundsill 32Document1 pageGroundsill 32Aditya PrayogaPas encore d'évaluation

- Assembly JIG & FIXTUREDocument1 pageAssembly JIG & FIXTUREYulian Dwi NurwantiPas encore d'évaluation

- Complex engineering assembly diagram breakdownDocument1 pageComplex engineering assembly diagram breakdownYulian Dwi NurwantiPas encore d'évaluation

- Plano de Un Vivienda de Concreto Armado de Dos Pisos Con Cobertura de Teja Andina Sobre TijeralesDocument1 pagePlano de Un Vivienda de Concreto Armado de Dos Pisos Con Cobertura de Teja Andina Sobre TijeralesFrancisco IPPas encore d'évaluation

- Deslizador PDFDocument1 pageDeslizador PDFDaniel BtitoPas encore d'évaluation

- Deslizador PDFDocument1 pageDeslizador PDFDaniel BtitoPas encore d'évaluation

- Deslizador PDFDocument1 pageDeslizador PDFDaniel BtitoPas encore d'évaluation

- 26/04/2016 Rodrigo Rodrigo Rodrigo: Date Date Approved by Checked by Designed byDocument1 page26/04/2016 Rodrigo Rodrigo Rodrigo: Date Date Approved by Checked by Designed byDaniel BtitoPas encore d'évaluation

- Plotar Autocad - Projeto FinalDocument1 pagePlotar Autocad - Projeto Finallimabbruna22Pas encore d'évaluation

- Plan View LayoutDocument1 pagePlan View LayoutChristian IrakozePas encore d'évaluation

- SELAMAT DATANG KE EMPANGAN SG LEBAMDocument17 pagesSELAMAT DATANG KE EMPANGAN SG LEBAMNurul SakinahPas encore d'évaluation

- Print 1Document1 pagePrint 1Alya halilintarPas encore d'évaluation

- Print 1 PDFDocument1 pagePrint 1 PDFAlya halilintarPas encore d'évaluation

- Analysis of Semester Exam ResultsDocument9 pagesAnalysis of Semester Exam ResultswikytPas encore d'évaluation

- Popr 424 180Document1 pagePopr 424 180DhoviIrvanPas encore d'évaluation

- Diciembre 2021 Tarea N1Document1 pageDiciembre 2021 Tarea N1Jose Luis Ruiz RuizPas encore d'évaluation

- ROOF-DECK-PLAN-FINAL-ESQUISSE-SITEDocument1 pageROOF-DECK-PLAN-FINAL-ESQUISSE-SITEzseo7512Pas encore d'évaluation

- Invoice #1032 for 2 Black Leather JacketsDocument1 pageInvoice #1032 for 2 Black Leather Jacketspopoy fetsPas encore d'évaluation

- Desenho CanhãoDocument1 pageDesenho CanhãoLuiz Kozikoski0% (1)

- Project payment trackerDocument1 pageProject payment trackerpratik ghavatePas encore d'évaluation

- FPS Rig Loadings Spreadsheet Disclaimer ExplainedDocument9 pagesFPS Rig Loadings Spreadsheet Disclaimer Explainedpakbilal1Pas encore d'évaluation

- Employee ReimbursementDocument2 pagesEmployee ReimbursementPratima ChavanPas encore d'évaluation

- Upper half cutter machine diagramDocument1 pageUpper half cutter machine diagramDaniel Edward OmondiPas encore d'évaluation

- Building foundation plans and detailsDocument1 pageBuilding foundation plans and detailsThOfa MoPas encore d'évaluation

- Muka Tanah Asli: Pejabat Pembuat Komitmen Perencanaan Dan ProgramDocument1 pageMuka Tanah Asli: Pejabat Pembuat Komitmen Perencanaan Dan ProgramTim EmasPas encore d'évaluation

- DISEÑO CANCHA BARRIO SANTA ELENA BasqueDocument1 pageDISEÑO CANCHA BARRIO SANTA ELENA BasqueCarlosIvanLeonOliverosPas encore d'évaluation

- 10w Design LayoutDocument1 page10w Design Layoutabdul rehman syed parvezPas encore d'évaluation

- Potongan JembatanDocument1 pagePotongan JembatanAhmad YusufPas encore d'évaluation

- Denah Pola Lantai LT 2 Denah Pola Lantai LT 2: Shoji LandDocument1 pageDenah Pola Lantai LT 2 Denah Pola Lantai LT 2: Shoji Landprasetya ferdiPas encore d'évaluation

- Purchase Order Template 03 - TemplateLabDocument1 pagePurchase Order Template 03 - TemplateLabAfiq NoraniPas encore d'évaluation

- 2D Ragum Jepit AssyDocument1 page2D Ragum Jepit AssyHabib DodiPas encore d'évaluation

- Planta Baja Planta Alta Fachada PrincipalDocument1 pagePlanta Baja Planta Alta Fachada PrincipalYeiser Mendoza CotrinaPas encore d'évaluation

- Foundation plan and column detailsDocument1 pageFoundation plan and column detailsÇÄrlös EMPas encore d'évaluation

- Engineering drawing of mechanical parts assemblyDocument1 pageEngineering drawing of mechanical parts assemblyGnabryPas encore d'évaluation

- Name: Stage: 1: Jeddah Foundation Co. Design Sheet PilesDocument1 pageName: Stage: 1: Jeddah Foundation Co. Design Sheet PilesElhussain HassanPas encore d'évaluation

- Jaffar (Sans Chambre)Document4 pagesJaffar (Sans Chambre)Daniel FutiPas encore d'évaluation

- Daily Levels EnglishDocument1 pageDaily Levels EnglishFlorence ZhangPas encore d'évaluation

- Floor plan layout with room dimensionsDocument1 pageFloor plan layout with room dimensionsDanang DwinPas encore d'évaluation

- Invoice: 3etmd Engineering Solutions Private LTDDocument9 pagesInvoice: 3etmd Engineering Solutions Private LTDsmanpmkPas encore d'évaluation

- Dimensions and tolerances of a precision machined partDocument1 pageDimensions and tolerances of a precision machined partdoni eka saputraPas encore d'évaluation

- Ground Floor Plan Second Floor Plan Roof Plan: A B' B C D C' A' A B' B C D C' A' A B' B C D C'Document1 pageGround Floor Plan Second Floor Plan Roof Plan: A B' B C D C' A' A B' B C D C' A' A B' B C D C'JEH222Pas encore d'évaluation

- PERU Vs RUSIA PDFDocument1 pagePERU Vs RUSIA PDFyoelPas encore d'évaluation

- Go OfferDocument1 pageGo OfferOUSMAN SEIDPas encore d'évaluation

- Ound & First Floor PlanDocument1 pageOund & First Floor PlanChetan B ArkasaliPas encore d'évaluation

- ModelDocument3 pagesModelKHO KAI FEIPas encore d'évaluation

- Tec FormDocument1 pageTec FormalexPas encore d'évaluation

- DPA SKPD Document Budget ImplementationDocument28 pagesDPA SKPD Document Budget ImplementationTomi Adi PutraPas encore d'évaluation

- Dessin1 ObjetDocument1 pageDessin1 ObjetBruno CambléPas encore d'évaluation

- 1 - (Er) - 02 - Ida Risky Angelina - 3334200072Document1 page1 - (Er) - 02 - Ida Risky Angelina - 3334200072ROHMANSYAH ROHMANSYAHPas encore d'évaluation

- Supply Request 21Document1 pageSupply Request 21dubaitoyscdPas encore d'évaluation

- COLEZAG4Document1 pageCOLEZAG4milan3zxPas encore d'évaluation

- Edificio 8 PisosDocument3 pagesEdificio 8 PisosJôhânn SantamariaPas encore d'évaluation

- Detail SirenDocument1 pageDetail SirenMuhammad ImranPas encore d'évaluation

- R-Tech invoice 301 under 40 charactersDocument1 pageR-Tech invoice 301 under 40 charactersMukesh ManjhiPas encore d'évaluation

- 111 Layout1Document1 page111 Layout1abc dePas encore d'évaluation

- Signalizacija PDFDocument1 pageSignalizacija PDFMaja AbdihodžićPas encore d'évaluation

- Levantamiento 23Document1 pageLevantamiento 23jehieli.perez22Pas encore d'évaluation

- 8086 Cpu ArchitectureDocument9 pages8086 Cpu Architectureapi-371236783% (6)

- L & TDocument9 pagesL & Tapi-3712367Pas encore d'évaluation

- Report OnDocument9 pagesReport Onapi-3712367Pas encore d'évaluation

- Macroeconomics AssignmentsDocument15 pagesMacroeconomics Assignmentsapi-3712367Pas encore d'évaluation

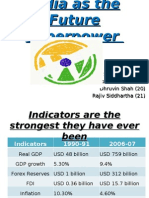

- India As SuperpowerDocument21 pagesIndia As Superpowerapi-3712367Pas encore d'évaluation

- Macro Economics OutlineDocument2 pagesMacro Economics Outlineapi-3712367100% (1)

- Manging Foreign ExchnageDocument6 pagesManging Foreign Exchnageapi-3712367Pas encore d'évaluation

- WEight Training ScheduleDocument2 pagesWEight Training Scheduleapi-3712367100% (1)

- Fiscal Deficit 2003 FormatDocument19 pagesFiscal Deficit 2003 Formatapi-3712367Pas encore d'évaluation

- Policybrief Nov05Document6 pagesPolicybrief Nov05api-3712367Pas encore d'évaluation

- Manging Foreign ExchnageDocument6 pagesManging Foreign Exchnageapi-3712367Pas encore d'évaluation

- 72903Document11 pages72903api-3712367Pas encore d'évaluation

- FOREX Management Versus SingaporeDocument3 pagesFOREX Management Versus Singaporeapi-3712367Pas encore d'évaluation

- Just in TimeDocument3 pagesJust in Timeapi-3712367Pas encore d'évaluation

- Fema CDocument5 pagesFema Capi-3712367Pas encore d'évaluation

- FFRChange HistoryDocument1 pageFFRChange Historyapi-3712367Pas encore d'évaluation

- D&B Economy Observer November 07Document3 pagesD&B Economy Observer November 07api-3712367Pas encore d'évaluation

- Foreign Exchange Management Policy in IndiaDocument6 pagesForeign Exchange Management Policy in Indiaapi-371236767% (3)

- US Subprime 070817Document6 pagesUS Subprime 070817api-3712367Pas encore d'évaluation

- Subprime FinalDocument34 pagesSubprime Finalapi-3712367Pas encore d'évaluation

- Sebi TocDocument33 pagesSebi Tocapi-3712367Pas encore d'évaluation

- Subprime Toxic Debt - Bloomberg July07Document10 pagesSubprime Toxic Debt - Bloomberg July07api-3712367Pas encore d'évaluation

- BSC & Knowledge ManagementDocument3 pagesBSC & Knowledge Managementapi-3712367100% (1)

- SubPrime Mortgage MarketDocument6 pagesSubPrime Mortgage Marketapi-3712367Pas encore d'évaluation

- Global Economics - IndiaDocument2 pagesGlobal Economics - Indiaapi-3712367Pas encore d'évaluation

- Balanced ScorecardDocument13 pagesBalanced Scorecardapi-3712367Pas encore d'évaluation

- SubprimeDocument31 pagesSubprimeapi-3712367Pas encore d'évaluation

- Balanced Scorecard Elearning - PresentationDocument39 pagesBalanced Scorecard Elearning - Presentationapi-3712367Pas encore d'évaluation

- Balanced Scorecard 02Document7 pagesBalanced Scorecard 02api-3712367100% (2)

- Indian Planning Overview: 5-Year Plans and Economic GrowthDocument44 pagesIndian Planning Overview: 5-Year Plans and Economic GrowthPanvel PatilPas encore d'évaluation

- Tarun Das ADB Nepal Macro Economic ModelDocument61 pagesTarun Das ADB Nepal Macro Economic ModelProfessor Tarun DasPas encore d'évaluation

- Domestic Resource Mobilisation IndiaDocument63 pagesDomestic Resource Mobilisation Indiaashish1981Pas encore d'évaluation

- Annual Report Highlights Nepal SBI Bank's Growth and ProgressDocument122 pagesAnnual Report Highlights Nepal SBI Bank's Growth and ProgressNirmal Shrestha100% (1)

- Gabor European Derisking State-1Document30 pagesGabor European Derisking State-1Maximus L MadusPas encore d'évaluation

- Creel ND Poilon - 2008Document47 pagesCreel ND Poilon - 2008StegabPas encore d'évaluation

- Akpi Laporan Tahunan 2021Document205 pagesAkpi Laporan Tahunan 2021Sella YunitaPas encore d'évaluation

- FRBM ActDocument2 pagesFRBM Actrajesh_scribd1984Pas encore d'évaluation

- Hsslive XII Economics Macro CH 5Document7 pagesHsslive XII Economics Macro CH 5RameshKumarMuraliPas encore d'évaluation

- Exam 3 Practice Exam, Econ 204, Fall 2019Document10 pagesExam 3 Practice Exam, Econ 204, Fall 2019abdulelahaljaafariPas encore d'évaluation

- EssayDocument5 pagesEssayJim_Tsao_4234Pas encore d'évaluation

- 122 1004Document32 pages122 1004api-275486640% (1)

- Paper 4 PYQDocument16 pagesPaper 4 PYQSaurabh PatelPas encore d'évaluation

- Perotti (2002)Document60 pagesPerotti (2002)Hoang Lan HuongPas encore d'évaluation

- Post Pandemic Recovery GrowthDocument47 pagesPost Pandemic Recovery GrowthShivang MohtaPas encore d'évaluation

- Public BudgetDocument10 pagesPublic BudgetMuhammad IbadPas encore d'évaluation

- Spain EconomyDocument15 pagesSpain EconomyHarikrishnan SPas encore d'évaluation

- Todays Accountant Issue 23 December 2022Document68 pagesTodays Accountant Issue 23 December 2022joelljeffPas encore d'évaluation

- Chapter 1Document30 pagesChapter 1Yitera SisayPas encore d'évaluation

- Greece Macro PDFDocument85 pagesGreece Macro PDFchetan choudhariPas encore d'évaluation

- Changing Dimensions of Business in IndiaDocument136 pagesChanging Dimensions of Business in Indiarajat_singla100% (1)

- Ahluwalia, M. S. (2019)Document17 pagesAhluwalia, M. S. (2019)rnjn mhta.Pas encore d'évaluation

- 2528 - 2ND Sem - Ba LLB (H) - CBCS - Economics IiDocument6 pages2528 - 2ND Sem - Ba LLB (H) - CBCS - Economics IiLòvè BírdsPas encore d'évaluation

- Macroeconomic Issues and Policy: Fernando & Yvonn QuijanoDocument30 pagesMacroeconomic Issues and Policy: Fernando & Yvonn Quijanoprasetyo caroko akbarPas encore d'évaluation

- Role of Government in Economic PolicyDocument22 pagesRole of Government in Economic PolicyMiss PauPas encore d'évaluation

- Government Budget Revision Notes for Class 12 MacroeconomicsDocument4 pagesGovernment Budget Revision Notes for Class 12 MacroeconomicsROHIT SHAPas encore d'évaluation

- Post-Crisis Economic Governance in Latvia: The European Semester, The Balance-of-Payments Programme, and Euro Accession ConvergenceDocument40 pagesPost-Crisis Economic Governance in Latvia: The European Semester, The Balance-of-Payments Programme, and Euro Accession ConvergenceSara CarterPas encore d'évaluation

- NISM Certified Course in Securities MarketsDocument12 pagesNISM Certified Course in Securities MarketsSunita RamanathanPas encore d'évaluation

- CFA Level1 2017 Mock Exam PDFDocument75 pagesCFA Level1 2017 Mock Exam PDFHéctor GarcíaPas encore d'évaluation