Vous aimerez peut-être aussi

- Trends and Determinants of Investment - UNCTAD 1998Document445 pagesTrends and Determinants of Investment - UNCTAD 1998Bui Thu HaPas encore d'évaluation

- Additional Questions On ProbabilityDocument5 pagesAdditional Questions On ProbabilityPeh Wee LoonPas encore d'évaluation

- Sell or Process Further Case AnalysisDocument23 pagesSell or Process Further Case AnalysisRosslyn Dayrit50% (2)

- Fondapol Study Paul Adrien Hyppolite Reshoring Production 2020 11Document72 pagesFondapol Study Paul Adrien Hyppolite Reshoring Production 2020 11FondapolPas encore d'évaluation

- Sy Po v. CTADocument11 pagesSy Po v. CTANester MendozaPas encore d'évaluation

- FM CH 15 PDFDocument50 pagesFM CH 15 PDFLayatmika SahooPas encore d'évaluation

- Cir V BoacDocument15 pagesCir V BoaccandicePas encore d'évaluation

- 13-Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Document13 pages13-Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Jopan SJPas encore d'évaluation

- Force MajeureDocument13 pagesForce MajeureGovind Shriram ChhawsariaPas encore d'évaluation

- International Parity Conditions 2Document30 pagesInternational Parity Conditions 2Monika BahlPas encore d'évaluation

- Global Strategic Management FrameworkDocument10 pagesGlobal Strategic Management FrameworkNavneet KumarPas encore d'évaluation

- Electrical ProjectDocument365 pagesElectrical Projectapi-3826509100% (3)

- Producer and Consumer SurplusDocument28 pagesProducer and Consumer SurplusSyedPas encore d'évaluation

- Futuristic Roadmap of FarmersDocument6 pagesFuturistic Roadmap of FarmersSatyajit RoyPas encore d'évaluation

- The McDonald's Coffee Spill Case: More Than Meets the EyeDocument2 pagesThe McDonald's Coffee Spill Case: More Than Meets the EyeBluehelenPas encore d'évaluation

- If NumericalsDocument13 pagesIf NumericalsArindam Chatterjee0% (1)

- Supreme Court upholds conviction of man for attempted homicideDocument6 pagesSupreme Court upholds conviction of man for attempted homicideK Dawn Bernal CaballeroPas encore d'évaluation

- Cost Output Relationship in The Short RunDocument5 pagesCost Output Relationship in The Short RunpratibhaPas encore d'évaluation

- Accounting ExamDocument7 pagesAccounting Examjerrytanny100% (1)

- Movie (Erin Brockovich)Document6 pagesMovie (Erin Brockovich)LA Yogore JermeoPas encore d'évaluation

- Relative ValuationDocument100 pagesRelative ValuationHonza MynarPas encore d'évaluation

- CH 08Document36 pagesCH 08Xiaojie CaiPas encore d'évaluation

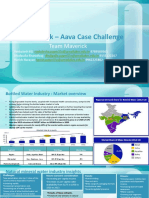

- On The Mark - Aava Case Challenge: Team MaverickDocument11 pagesOn The Mark - Aava Case Challenge: Team MaverickriteshPas encore d'évaluation

- The Recalcitrant Director at ByteDocument3 pagesThe Recalcitrant Director at ByteMarissa Sgambelluri100% (1)

- EE Optimization for Power Plants TrainingDocument313 pagesEE Optimization for Power Plants TrainingItilekha DashPas encore d'évaluation

- Capital StructureDocument58 pagesCapital StructureVinit WigPas encore d'évaluation

- Answer of Service and Retail MarketingDocument12 pagesAnswer of Service and Retail MarketingMAMAPas encore d'évaluation

- Jyske Bank Case Facilitation AnswersDocument8 pagesJyske Bank Case Facilitation AnswersJoey LiaoPas encore d'évaluation

- Perfect CompetitionDocument12 pagesPerfect CompetitionNomanPas encore d'évaluation

- Market Power and Externalities: Understanding Monopolies, Monopsonies, and Market FailuresDocument19 pagesMarket Power and Externalities: Understanding Monopolies, Monopsonies, and Market FailuresLove Rabbyt100% (1)

- Answer Key CH 2Document8 pagesAnswer Key CH 2Thien HuongPas encore d'évaluation

- Swot AnalysisDocument12 pagesSwot AnalysisXandre AsisPas encore d'évaluation

- Income and Substitution Effects of A Wage ChangeDocument24 pagesIncome and Substitution Effects of A Wage ChangemanashchoudhuryPas encore d'évaluation

- 5-Supplier Selection & EvaluationDocument52 pages5-Supplier Selection & EvaluationshettarvijayPas encore d'évaluation

- RIC 601 ASSIGNMENT ANALYSIS OF INTERNATIONAL FINANCE TOPICSDocument11 pagesRIC 601 ASSIGNMENT ANALYSIS OF INTERNATIONAL FINANCE TOPICSmohithPas encore d'évaluation

- Bonds Valuation Practice ProblemsDocument6 pagesBonds Valuation Practice ProblemsMaria Danielle Fajardo CuysonPas encore d'évaluation

- Ken Black QA ch08Document43 pagesKen Black QA ch08Rushabh Vora0% (1)

- Supply DemandProblems With Solutions, Part 1Document16 pagesSupply DemandProblems With Solutions, Part 1deviPas encore d'évaluation

- Makerere University College of Business and Management Studies Master of Business AdministrationDocument15 pagesMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidPas encore d'évaluation

- Breaking Up Price Effect Into Income and Substitution EffectDocument9 pagesBreaking Up Price Effect Into Income and Substitution Effectanushka KumariPas encore d'évaluation

- Chap 03Document16 pagesChap 03Syed Hamdan100% (1)

- Assumptions of Kinked Demand CurveDocument2 pagesAssumptions of Kinked Demand CurveBhawna PuriPas encore d'évaluation

- 5 - The Behavior of Interest RatesDocument31 pages5 - The Behavior of Interest RatescihtanbioPas encore d'évaluation

- TRADITIONAL VS ABC COSTING FOR TWO PRODUCTSDocument16 pagesTRADITIONAL VS ABC COSTING FOR TWO PRODUCTSrsalicsicPas encore d'évaluation

- Demand in A Perfectly Competitive MarketDocument4 pagesDemand in A Perfectly Competitive MarketCrisielyn BuyanPas encore d'évaluation

- WTO Patent Rules and Access To Medicines: The Pressure MountsDocument11 pagesWTO Patent Rules and Access To Medicines: The Pressure MountsOxfamPas encore d'évaluation

- Comparative Vs Competitive AdvantageDocument19 pagesComparative Vs Competitive AdvantageSuntari CakSoenPas encore d'évaluation

- Supply, Demand & EquilibriumDocument4 pagesSupply, Demand & EquilibriumClarisse AnnPas encore d'évaluation

- Problems and Solutions Ratio Analysis Finance AssignmentDocument11 pagesProblems and Solutions Ratio Analysis Finance AssignmentGolf TigerPas encore d'évaluation

- Challenges of MRPDocument3 pagesChallenges of MRPOmotayoPas encore d'évaluation

- Lecture Notes - Welfare EconomicsDocument23 pagesLecture Notes - Welfare EconomicsJacksonPas encore d'évaluation

- Answers To Chapter 14 QuestionsDocument9 pagesAnswers To Chapter 14 QuestionsManuel SantanaPas encore d'évaluation

- (No. 6878. September 13, 1913.) MARCELINA EDROSO, Petitioner and Appellant, vs. PABLO and BASILIO SABLAN, Opponents and AppelleesDocument19 pages(No. 6878. September 13, 1913.) MARCELINA EDROSO, Petitioner and Appellant, vs. PABLO and BASILIO SABLAN, Opponents and AppelleesAira Mae P. LayloPas encore d'évaluation

- SEZA SummaryDocument6 pagesSEZA Summaryhatta18Pas encore d'évaluation

- 4 CIR Vs Reyes GR 159694-GR 163581 Jan 27 2006Document10 pages4 CIR Vs Reyes GR 159694-GR 163581 Jan 27 2006FredamoraPas encore d'évaluation

- Solution To Questions On Decision MakingDocument27 pagesSolution To Questions On Decision Makingdanishbashir786Pas encore d'évaluation

- Relevant Cost Examples EMBA-garrison Ch.13Document13 pagesRelevant Cost Examples EMBA-garrison Ch.13Aarti JPas encore d'évaluation

- Optimize Housekeeping ProgramDocument15 pagesOptimize Housekeeping ProgramFiras HamadPas encore d'évaluation

- Week 13 - In-class assignments and costing exercisesDocument20 pagesWeek 13 - In-class assignments and costing exercisesadms examzPas encore d'évaluation

- Solutions To Relevant Cost ProblemsDocument9 pagesSolutions To Relevant Cost ProblemsEljay VinsonPas encore d'évaluation

- Marketing Strategy of Mcdonalds ReportDocument9 pagesMarketing Strategy of Mcdonalds ReportahmadPas encore d'évaluation

- Concierge Service Business Model CanvasDocument1 pageConcierge Service Business Model CanvasartemisglassesPas encore d'évaluation

- PDF-Logistics & Supply Chain ManagementDocument34 pagesPDF-Logistics & Supply Chain ManagementShyam Khamniwala73% (15)

- Chapter 2 - The Nature of Organizational ChangeDocument19 pagesChapter 2 - The Nature of Organizational ChangeHira Salim33% (3)

- Sabmiller: Aidan Mcquade and Gerry JohnsonDocument9 pagesSabmiller: Aidan Mcquade and Gerry JohnsonDim SumPas encore d'évaluation

- Marketing Strategy of ParleDocument9 pagesMarketing Strategy of ParleSiddharth MishraPas encore d'évaluation

- Market Potential of New Energy Drinks in BangladeshDocument12 pagesMarket Potential of New Energy Drinks in BangladeshJishan PareraPas encore d'évaluation

- Sehalta Investments LTD Company Profile....Document20 pagesSehalta Investments LTD Company Profile....Shakes SMPas encore d'évaluation

- Cole Naldzin CVCompanionDocument7 pagesCole Naldzin CVCompanionCole Casola NaldzinPas encore d'évaluation

- SudhirDocument4 pagesSudhirSudhir JhaPas encore d'évaluation

- FIELD DESCRIPTIONS FOR SALES DOCUMENT HEADER DATADocument28 pagesFIELD DESCRIPTIONS FOR SALES DOCUMENT HEADER DATAGudipati Upender ReddyPas encore d'évaluation

- Sales PromotionDocument28 pagesSales PromotionNastasya Pro60% (5)

- Strategic Analysis of Sana SafinazDocument19 pagesStrategic Analysis of Sana SafinazAbbas KhanPas encore d'évaluation

- Exams Becvm Progresstest02Document5 pagesExams Becvm Progresstest02Sebastian2007Pas encore d'évaluation

- Minor Project Report On PhillipsDocument56 pagesMinor Project Report On PhillipsKeshav Maheshwari100% (2)

- Coca-Cola VS PepsiDocument3 pagesCoca-Cola VS PepsiNilesh GunjalPas encore d'évaluation

- HCC Strategic PPT Final 1Document15 pagesHCC Strategic PPT Final 1kevinPas encore d'évaluation

- Sales Negotiation Skills: The Flawless Way To Deal With Your ProspectsDocument48 pagesSales Negotiation Skills: The Flawless Way To Deal With Your ProspectsDr-Abhishek TiwariPas encore d'évaluation

- Answer 1: BiancaDocument4 pagesAnswer 1: BiancaHira NazPas encore d'évaluation

- Digital MarketingDocument10 pagesDigital Marketingvisual foxxPas encore d'évaluation

- SNL 01 General ExcellenceDocument125 pagesSNL 01 General ExcellenceSNLeaderPas encore d'évaluation

- Holistic MarketingDocument9 pagesHolistic MarketingSundar RajPas encore d'évaluation

- Impact of CRM On Customer Retention With Special Reference To Tata SkyDocument8 pagesImpact of CRM On Customer Retention With Special Reference To Tata SkySarit SinghPas encore d'évaluation

- True Chip Solutions Campus Recruitment - 2016 Batch (Only For Unplaced Students)Document3 pagesTrue Chip Solutions Campus Recruitment - 2016 Batch (Only For Unplaced Students)MAHESH VPas encore d'évaluation

- Burger King Mini CaseDocument17 pagesBurger King Mini CaseAccounting ClubPas encore d'évaluation

- Hecht, Michael F - Resume 02-10vDocument4 pagesHecht, Michael F - Resume 02-10vJulie LarsenPas encore d'évaluation

- CB - Kelloggs Assignment - Prateek Das - FT164056Document7 pagesCB - Kelloggs Assignment - Prateek Das - FT164056PrateekPas encore d'évaluation

- Identifying the Right Span of ControlDocument8 pagesIdentifying the Right Span of ControlmicahtanPas encore d'évaluation

- GFCO Certification ManualDocument72 pagesGFCO Certification Manualatila117Pas encore d'évaluation

- BECG QuestionsDocument3 pagesBECG Questionssampath kumarPas encore d'évaluation