Vous aimerez peut-être aussi

- Financial AccountingDocument455 pagesFinancial AccountingKalGeorgePas encore d'évaluation

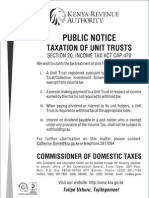

- Taxation of Unit TrustsDocument1 pageTaxation of Unit TrustsKalGeorgePas encore d'évaluation

- Admin TQMDocument28 pagesAdmin TQMManuel Sanchez QuispePas encore d'évaluation

- Work Injury Benefits ACT 2007Document49 pagesWork Injury Benefits ACT 2007KalGeorge100% (1)

- Manual TransmissionDocument16 pagesManual TransmissionKalGeorgePas encore d'évaluation

- 2015 Syllabus PDFDocument5 pages2015 Syllabus PDFKalGeorgePas encore d'évaluation

- Tax Procedures Act, 2015 FullDocument82 pagesTax Procedures Act, 2015 FullKalGeorgePas encore d'évaluation

- Motor Vehicles Cycle Mc-2013rrrDocument1 pageMotor Vehicles Cycle Mc-2013rrrKalGeorgePas encore d'évaluation

- Value Added TaxDocument27 pagesValue Added TaxKalGeorgePas encore d'évaluation

- Zuku Payments Format PDFDocument2 pagesZuku Payments Format PDFKalGeorgePas encore d'évaluation

- Kenya's 2016/17 Budget Statement focuses on consolidating economic gainsDocument35 pagesKenya's 2016/17 Budget Statement focuses on consolidating economic gainsMwende KyaniaPas encore d'évaluation

- Print - Minimum Wage Rates in KenyaDocument2 pagesPrint - Minimum Wage Rates in KenyaKalGeorgePas encore d'évaluation

- PKF Kenya Quick Tax Guide 2016Document10 pagesPKF Kenya Quick Tax Guide 2016KalGeorgePas encore d'évaluation

- Zuku Payments Format PDFDocument2 pagesZuku Payments Format PDFKalGeorgePas encore d'évaluation

- Seed Catolgue 2014-1 PDFDocument12 pagesSeed Catolgue 2014-1 PDFKalGeorgePas encore d'évaluation

- Kenya passport application formDocument4 pagesKenya passport application formKalGeorgePas encore d'évaluation

- Accountanct Firm RankingDocument3 pagesAccountanct Firm RankingKalGeorgePas encore d'évaluation

- 01 H 20120814135404Document1 page01 H 20120814135404KalGeorgePas encore d'évaluation

- Hague Proceedings 7th April 2011Document4 pagesHague Proceedings 7th April 2011KalGeorgePas encore d'évaluation

- Vat Act 2008Document150 pagesVat Act 2008Githinji GatheruPas encore d'évaluation

- Enabling Multiple Currency in Tally: Operations Alteration ScreenDocument15 pagesEnabling Multiple Currency in Tally: Operations Alteration ScreenKalGeorgePas encore d'évaluation

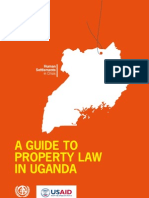

- A Guide To Property Law in UgandaDocument60 pagesA Guide To Property Law in UgandaEmmanuel OtengPas encore d'évaluation

- 8 Steps For Redeeming MARRIAGEDocument3 pages8 Steps For Redeeming MARRIAGEKalGeorgePas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Fap Module ObjectivesDocument25 pagesFap Module ObjectivesHông HoaPas encore d'évaluation

- Narrative DescriptionDocument2 pagesNarrative DescriptionAnonymous N9dx4ATEghPas encore d'évaluation

- NPS statement shows Rs. 39,000 voluntary contributionsDocument1 pageNPS statement shows Rs. 39,000 voluntary contributionsamit_saxena_10Pas encore d'évaluation

- Acca f6 Smart Notes Fa19 40 PagesDocument43 pagesAcca f6 Smart Notes Fa19 40 PagesAlex RomarioPas encore d'évaluation

- Salary Packaging - Smart SalaryDocument9 pagesSalary Packaging - Smart SalaryraogongfuPas encore d'évaluation

- Ias 12Document5 pagesIas 12Ahmed NiazPas encore d'évaluation

- Faculty Recruitment Emeritus Professor 2023-24 AdvDocument3 pagesFaculty Recruitment Emeritus Professor 2023-24 AdvSk Arif AhmedPas encore d'évaluation

- Unit 5 Social Security SchemesDocument58 pagesUnit 5 Social Security SchemesKanwaljeet SinghPas encore d'évaluation

- TCS India Process - Separation Kit - 16 Sep 2020Document26 pagesTCS India Process - Separation Kit - 16 Sep 2020KrishnaTejaPas encore d'évaluation

- Lesson Plan Planet - Paycheck - LP - 2 (1) .13.1Document15 pagesLesson Plan Planet - Paycheck - LP - 2 (1) .13.1Dayton Rogalski [Legacy HS]Pas encore d'évaluation

- Chapter 2 RRL FINAL UpdatedDocument13 pagesChapter 2 RRL FINAL UpdatedCoke Aidenry SaludoPas encore d'évaluation

- Under Rule - : Subject: HoldingDocument4 pagesUnder Rule - : Subject: HoldingamlegalPas encore d'évaluation

- Assignment 2 - Termination of EmploymentDocument5 pagesAssignment 2 - Termination of EmploymentAraceli Gloria-FranciscoPas encore d'évaluation

- Jamia Milia Islamia: Faculty of LawDocument9 pagesJamia Milia Islamia: Faculty of LawMđ ĞåùsPas encore d'évaluation

- Case Safilo-Luxottica PART A 2018 V - 1Document5 pagesCase Safilo-Luxottica PART A 2018 V - 1Reyansh SharmaPas encore d'évaluation

- 2020 Employer Toolkit V12 1Document22 pages2020 Employer Toolkit V12 1sachinitsmePas encore d'évaluation

- Non-Employment AcknowledgementDocument1 pageNon-Employment AcknowledgementEmily De JesusPas encore d'évaluation

- Reading 9 Employee Compensation - Post-Employment and Share-Based - AnswersDocument21 pagesReading 9 Employee Compensation - Post-Employment and Share-Based - Answerstristan.riolsPas encore d'évaluation

- Tutorial 10 QsDocument4 pagesTutorial 10 QsDylan Rabin PereiraPas encore d'évaluation

- Format of Income Affidavit For MCM & SC-ST Scholarship (4833) PDFDocument1 pageFormat of Income Affidavit For MCM & SC-ST Scholarship (4833) PDFshubhamPas encore d'évaluation

- Mragr00028620000020847 2023Document2 pagesMragr00028620000020847 202394116521Pas encore d'évaluation

- Assn #3 - SKDocument2 pagesAssn #3 - SKRUBY SHARMAPas encore d'évaluation

- Tutorial 6aDocument2 pagesTutorial 6aYeong Zi YingPas encore d'évaluation

- Protect Family & DreamsDocument6 pagesProtect Family & Dreamspradeep kumarPas encore d'évaluation

- Homework on savings, investments, annuities and loans (Deadline 27 NovDocument2 pagesHomework on savings, investments, annuities and loans (Deadline 27 NovcbarajPas encore d'évaluation

- Gratuity PolicyDocument2 pagesGratuity PolicyVishala GudageriPas encore d'évaluation

- Tutorial On How To Request PUA Payments: 1. Which Weeks Can I Claim Benefits?Document2 pagesTutorial On How To Request PUA Payments: 1. Which Weeks Can I Claim Benefits?Tina MartinezPas encore d'évaluation

- Black BookDocument66 pagesBlack BookYuvrajPas encore d'évaluation

- Chapter 3 - The Government Process (Autosaved)Document52 pagesChapter 3 - The Government Process (Autosaved)Rovey JPas encore d'évaluation

- What Is A 401Document6 pagesWhat Is A 401KidMonkey2299Pas encore d'évaluation