Vous aimerez peut-être aussi

- Audit Con Solid Taed NotesDocument2 pagesAudit Con Solid Taed Noteshussainf04Pas encore d'évaluation

- Regulation NotesDocument3 pagesRegulation Noteshussainf04Pas encore d'évaluation

- Secured Party Rights to Purchase CollateralDocument4 pagesSecured Party Rights to Purchase Collateralhussainf04Pas encore d'évaluation

- Regulation NotesDocument3 pagesRegulation Noteshussainf04Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Record Retention GuideDocument10 pagesRecord Retention GuidepghmalePas encore d'évaluation

- Budget Synopsis 2015-16 PDFDocument12 pagesBudget Synopsis 2015-16 PDFBhagwan PalPas encore d'évaluation

- Sinking Fund and Present Value FormulasDocument32 pagesSinking Fund and Present Value FormulasniginkabrahamPas encore d'évaluation

- PEnsioni CalculatDocument27 pagesPEnsioni CalculatA2 Section CollectoratePas encore d'évaluation

- Book Review - CH 14 - Investment Life CycleDocument24 pagesBook Review - CH 14 - Investment Life CycleApu DharPas encore d'évaluation

- Labor Relations Development Structure Process 12Th Edition Fossum Solutions Manual Full Chapter PDFDocument49 pagesLabor Relations Development Structure Process 12Th Edition Fossum Solutions Manual Full Chapter PDFNancyWardDDSrods100% (8)

- Legal Last Name Change - TXDocument4 pagesLegal Last Name Change - TXPenny LanePas encore d'évaluation

- TX04 Allowable Deductionsv2Document12 pagesTX04 Allowable Deductionsv2Ace DesabillePas encore d'évaluation

- Problem BankDocument10 pagesProblem BankSimona NistorPas encore d'évaluation

- Pension Accounting QuizDocument8 pagesPension Accounting QuizCarl Dhaniel Garcia SalenPas encore d'évaluation

- 46 Re Request of Atty. Bernardo ZialcitaDocument9 pages46 Re Request of Atty. Bernardo ZialcitaYaz CarlomanPas encore d'évaluation

- Rythu Bandhu Scheme Claim Form 1Document2 pagesRythu Bandhu Scheme Claim Form 1CHETTI SAGARPas encore d'évaluation

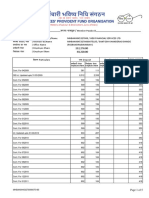

- Passbook PFDocument5 pagesPassbook PFDarshan SarodePas encore d'évaluation

- UO Football Coach ContractDocument23 pagesUO Football Coach ContractSinclair Broadcast Group - EugenePas encore d'évaluation

- Plaid Cymru Easy Read Manifesto 2017Document21 pagesPlaid Cymru Easy Read Manifesto 2017Plaid CymruPas encore d'évaluation

- Voluntary Retirement Scheme ExplainedDocument5 pagesVoluntary Retirement Scheme ExplainedpsychicnutPas encore d'évaluation

- Tax CalculationDocument6 pagesTax CalculationClarencia VeronicaPas encore d'évaluation

- Treaties Between The Uk and The State of Somaliland 1960Document15 pagesTreaties Between The Uk and The State of Somaliland 1960Garyaqaan Muuse YuusufPas encore d'évaluation

- Valuation of Life Insurance Liabilities On A Market-Consistent Basis: Experience From The United KingdomDocument41 pagesValuation of Life Insurance Liabilities On A Market-Consistent Basis: Experience From The United KingdomammaPas encore d'évaluation

- Guidelines To Plan & Claim FBPDocument9 pagesGuidelines To Plan & Claim FBPPrasannaPas encore d'évaluation

- BSF, ItbpDocument1 pageBSF, Itbpajay chaturvediPas encore d'évaluation

- A Study On The Awareness of Tax Saving Instruments of Individual Tax PayersDocument11 pagesA Study On The Awareness of Tax Saving Instruments of Individual Tax Payersadebabay amsaluPas encore d'évaluation

- Annuities BasicxcxDocument31 pagesAnnuities BasicxcxPineapple FreedommPas encore d'évaluation

- RR 1-68Document10 pagesRR 1-68Crnc Navidad100% (1)

- PRBS Update Form for Retirees, Survivors, TransfereesDocument1 pagePRBS Update Form for Retirees, Survivors, TransfereesEPSPD PRE RETIREMENT100% (2)

- Fringe Benefits in Tanzania Meaning Objectives TYPES PROBLEMS Prepared by Charles J. MwamtobeDocument6 pagesFringe Benefits in Tanzania Meaning Objectives TYPES PROBLEMS Prepared by Charles J. MwamtobeABILAH SALUMPas encore d'évaluation

- Mallin - Corporate-Governance PDFDocument407 pagesMallin - Corporate-Governance PDFSharron Shatil88% (17)

- Finance (Pension) Department G.O. No.72, DATED 19th March, 2003Document4 pagesFinance (Pension) Department G.O. No.72, DATED 19th March, 2003Brooks OrtizPas encore d'évaluation

- Time Value of Money FMDocument28 pagesTime Value of Money FMMonkey DLuffyyyPas encore d'évaluation

- Questions On Income From SalaryDocument3 pagesQuestions On Income From SalaryAniket AgrawalPas encore d'évaluation