Vous aimerez peut-être aussi

- Everything You Need to Know About Leasing, Hire Purchase, and Financing OptionsDocument33 pagesEverything You Need to Know About Leasing, Hire Purchase, and Financing OptionsSoumendra RoyPas encore d'évaluation

- Indemnity AgreementDocument4 pagesIndemnity AgreementJustin LoredoPas encore d'évaluation

- HR Generalist Executive Resume Samples - ResumeDocument7 pagesHR Generalist Executive Resume Samples - ResumeP RajendraPas encore d'évaluation

- SHRM Certified Professional in PakistanDocument5 pagesSHRM Certified Professional in PakistanAdnan QamarPas encore d'évaluation

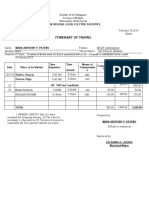

- Iterenary Travel FormDocument3 pagesIterenary Travel Formsplef lguPas encore d'évaluation

- Operations Research P Rama Murthy PDFDocument716 pagesOperations Research P Rama Murthy PDFPaban Raj LohaniPas encore d'évaluation

- Er 1-94 Program Issuance Fund Allocation - Doe PDFDocument52 pagesEr 1-94 Program Issuance Fund Allocation - Doe PDFMelvin John CabelinPas encore d'évaluation

- Coquia Vs Fieldmen's Insurance CoDocument1 pageCoquia Vs Fieldmen's Insurance CoSuiPas encore d'évaluation

- BP Time Charter Party AgreementDocument30 pagesBP Time Charter Party Agreementahong100100% (2)

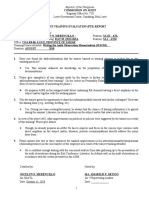

- Post-Training Evaluation Report for Writing the Audit Observation MemorandumDocument1 pagePost-Training Evaluation Report for Writing the Audit Observation Memorandumrocky CadizPas encore d'évaluation

- Sample Bidding Documents For The Procurement of Supply For Janitorial ServicesDocument95 pagesSample Bidding Documents For The Procurement of Supply For Janitorial ServicesAlvin Claridades100% (1)

- ACCOUNTING FOR SPECIAL EDUCATION FUNDSDocument12 pagesACCOUNTING FOR SPECIAL EDUCATION FUNDSIrdo KwanPas encore d'évaluation

- 1 How To Write A Feasibility Study - MartinaDocument23 pages1 How To Write A Feasibility Study - MartinaJb JaybeePas encore d'évaluation

- 1 How To Write A Feasibility Study - MartinaDocument23 pages1 How To Write A Feasibility Study - MartinaJb JaybeePas encore d'évaluation

- Office of The Lupong Tagapamayapa Affidavit: - Lupon MemberDocument6 pagesOffice of The Lupong Tagapamayapa Affidavit: - Lupon MemberMichael EgotPas encore d'évaluation

- Final Exam in Business Mathematics GAS 1, 2, 3 & ABM 12: Department of EducationDocument3 pagesFinal Exam in Business Mathematics GAS 1, 2, 3 & ABM 12: Department of EducationRainy Wagas100% (1)

- PPSAS Report For PowerpointDocument6 pagesPPSAS Report For PowerpointButchoy GemaoPas encore d'évaluation

- Anonymized Competency Based RecruitmentDocument46 pagesAnonymized Competency Based Recruitmentmelizze100% (1)

- Solving Business Math Problems with Fractions, Decimals & PercentDocument7 pagesSolving Business Math Problems with Fractions, Decimals & PercentJoyen AtilloPas encore d'évaluation

- Rules On LeaveDocument9 pagesRules On LeaveAnonymous 1lYUUy5T89% (9)

- Rules On LeaveDocument9 pagesRules On LeaveAnonymous 1lYUUy5T89% (9)

- Rules On LeaveDocument9 pagesRules On LeaveAnonymous 1lYUUy5T89% (9)

- BUSINESS PERMITS AND LICENSING EXEMPTIONSDocument10 pagesBUSINESS PERMITS AND LICENSING EXEMPTIONSMecs NidPas encore d'évaluation

- PNP Ops Manual 2013Document222 pagesPNP Ops Manual 2013ianlayno100% (2)

- Civil Service Form No.6 Revised 2020 Republic of The Philippines City Government of LucenaDocument2 pagesCivil Service Form No.6 Revised 2020 Republic of The Philippines City Government of LucenaCriselda Cabangon DavidPas encore d'évaluation

- Master-charterer relationship and key shipping termsDocument5 pagesMaster-charterer relationship and key shipping termsDaniel M. MartinPas encore d'évaluation

- Proforma-Recon of SCBA and SFPDocument3 pagesProforma-Recon of SCBA and SFPdianajeanbucuPas encore d'évaluation

- System Development of Market Mobile Application For Sustainable Local Industry in The Philippines by Analiza v. MuñozDocument31 pagesSystem Development of Market Mobile Application For Sustainable Local Industry in The Philippines by Analiza v. MuñozmelizzePas encore d'évaluation

- NA SG-24: Republic of The Philippines Position Description Form DBM-CSC Form No. 1Document14 pagesNA SG-24: Republic of The Philippines Position Description Form DBM-CSC Form No. 1KristelaMarieU.VasquezPas encore d'évaluation

- Barangay Tax PresentationDocument14 pagesBarangay Tax PresentationKriston LipatPas encore d'évaluation

- CA upholds DOLE order but exempts company officer from liabilityDocument7 pagesCA upholds DOLE order but exempts company officer from liabilityRae100% (1)

- Letter Transmittal-Dbm Atello - Submission of Aip2020Document1 pageLetter Transmittal-Dbm Atello - Submission of Aip2020LGU PadadaPas encore d'évaluation

- DBM Dilg Joint Memorandum Circular No 2021 1 Dated August 11 2021Document56 pagesDBM Dilg Joint Memorandum Circular No 2021 1 Dated August 11 2021Tristan Lindsey Kaamiño AresPas encore d'évaluation

- RR 2-98 Section 2.57 (B) - CWTDocument3 pagesRR 2-98 Section 2.57 (B) - CWTZenaida LatorrePas encore d'évaluation

- PCSO Deed of DonationDocument1 pagePCSO Deed of DonationGarry A. CabotajePas encore d'évaluation

- Public Service Values PDFDocument99 pagesPublic Service Values PDFcool08coolPas encore d'évaluation

- Framework Operational ResearchDocument72 pagesFramework Operational Researchmelizze100% (1)

- Hon. Carlos M. Padilla: Provincial Cooperative and Enterprise Development OfficeDocument1 pageHon. Carlos M. Padilla: Provincial Cooperative and Enterprise Development OfficeRoel Jr Pinaroc DolaypanPas encore d'évaluation

- Executive Order No - Hotline 8888Document2 pagesExecutive Order No - Hotline 8888Pj Tigniman0% (1)

- Letter of Request To SPDocument1 pageLetter of Request To SPAlvin PateresPas encore d'évaluation

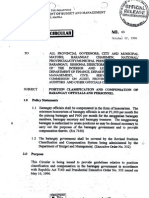

- Local Budget Circular: 'BaranpayDocument7 pagesLocal Budget Circular: 'BaranpayElizalde Teo BobbyPas encore d'évaluation

- 1601e Form PDFDocument3 pages1601e Form PDFLee GhaiaPas encore d'évaluation

- Audit Report - TuburanDocument87 pagesAudit Report - TuburanMaria100% (1)

- Annex A.1.1 - Sworn Declaration of Taxpayers ProfileDocument2 pagesAnnex A.1.1 - Sworn Declaration of Taxpayers ProfileKimberly MayPas encore d'évaluation

- Possession or Transport of Forest Products Without The Required Permit Is Considered Illegal Under Section 2 of DAO 97Document2 pagesPossession or Transport of Forest Products Without The Required Permit Is Considered Illegal Under Section 2 of DAO 97Jay EmmanuelPas encore d'évaluation

- LNB CamSur MC No 03 S 2022 Remittance Annual DuesDocument2 pagesLNB CamSur MC No 03 S 2022 Remittance Annual Duesfinance2018 approPas encore d'évaluation

- Activity-Design-Community Service ActivityDocument4 pagesActivity-Design-Community Service ActivityJanJan BoragayPas encore d'évaluation

- 027 - 2015 SB Res. - 10 Tricycle FranchiseDocument4 pages027 - 2015 SB Res. - 10 Tricycle FranchiseSBGuinobatanPas encore d'évaluation

- Environmental Planning Profession in the PhilippinesDocument11 pagesEnvironmental Planning Profession in the PhilippinesJam Steve RianomaPas encore d'évaluation

- 2.3 POPS-Planning-Presentation-2023-2025Document78 pages2.3 POPS-Planning-Presentation-2023-2025yna garcesPas encore d'évaluation

- Erpo Memo 921 Re BoeDocument7 pagesErpo Memo 921 Re BoeJadeBocoPas encore d'évaluation

- Form 1945 - Application For Certificate of Tax Exemption For CooperativesDocument4 pagesForm 1945 - Application For Certificate of Tax Exemption For CooperativesDarryl Jay Medina100% (1)

- GUIDELINES TO LGUs ENJOINING PARTICIPATION IN THE PALENG-QR PH PROGRAMDocument15 pagesGUIDELINES TO LGUs ENJOINING PARTICIPATION IN THE PALENG-QR PH PROGRAMLGU KALAMANSIG BPLOPas encore d'évaluation

- 2014-Creation of Hrmo Ordinance-No - 443Document3 pages2014-Creation of Hrmo Ordinance-No - 443jori mart morenoPas encore d'évaluation

- JJWC PDF Flowchart C1 Diversion KPambarangay PDFDocument1 pageJJWC PDF Flowchart C1 Diversion KPambarangay PDFRNJPas encore d'évaluation

- NMIS - Procedure For The Certificate of Accreditation To Meat Transport Vehicles (MTV)Document1 pageNMIS - Procedure For The Certificate of Accreditation To Meat Transport Vehicles (MTV)mj santosPas encore d'évaluation

- Ease of Doing Business PDFDocument1 pageEase of Doing Business PDFEmily Mag-alasinPas encore d'évaluation

- Final Resolution-Authorizing Lgu To Sign MoaDocument2 pagesFinal Resolution-Authorizing Lgu To Sign MoaDeil L. NaveaPas encore d'évaluation

- DILP Beneficiary ProfileDocument1 pageDILP Beneficiary ProfileMhayne DumpasPas encore d'évaluation

- Bplo Unified Business Application Form Final20201216 - 05939Document1 pageBplo Unified Business Application Form Final20201216 - 05939Elmer ZabalaPas encore d'évaluation

- SB Resolution TemplateDocument1 pageSB Resolution TemplateJe PascualPas encore d'évaluation

- DBM Cicular Letter 2013-16Document16 pagesDBM Cicular Letter 2013-16Elizabeth VasquezPas encore d'évaluation

- Recommendation Letter 3Document1 pageRecommendation Letter 3Rnm ZltaPas encore d'évaluation

- SK Chairperson'S Certification: SKCC No.: 2020-08-001 Date: August 25, 2020 To: The Bank ManagerDocument2 pagesSK Chairperson'S Certification: SKCC No.: 2020-08-001 Date: August 25, 2020 To: The Bank Managerjho frondaPas encore d'évaluation

- Revenue Code of The Municipality of Trinidad, BoholDocument100 pagesRevenue Code of The Municipality of Trinidad, BoholMaan Pastor MananzanPas encore d'évaluation

- Lecture-Npos in The PhilippinesDocument14 pagesLecture-Npos in The PhilippinesAngela PaduaPas encore d'évaluation

- Brgy. Cert. (Cattle)Document1 pageBrgy. Cert. (Cattle)BluboyPas encore d'évaluation

- SAOR 2015 Additional AOM DO ZDNDocument9 pagesSAOR 2015 Additional AOM DO ZDNrussel1435Pas encore d'évaluation

- LNB Constitution and ByLawsDocument20 pagesLNB Constitution and ByLawsLovely RoblesPas encore d'évaluation

- Restricts 4Ps Cash Cards as Loan CollateralDocument4 pagesRestricts 4Ps Cash Cards as Loan CollateralMSSBPas encore d'évaluation

- Letter Request For The Creation of Tourism Operations Officer I and Administrative Assistant VDocument4 pagesLetter Request For The Creation of Tourism Operations Officer I and Administrative Assistant Vjori mart morenoPas encore d'évaluation

- EO FirecrackerDocument4 pagesEO FirecrackerVinvin EsoenPas encore d'évaluation

- Contract of Service HandlerDocument4 pagesContract of Service HandlerClaire CabactulanPas encore d'évaluation

- PhilHealth NCR Procurement of Office SuppliesDocument21 pagesPhilHealth NCR Procurement of Office Suppliesjertin0% (1)

- Training Design Legal DraftDocument2 pagesTraining Design Legal DraftMark Gene Salga100% (1)

- Agenda of The 110th Regular SessionDocument67 pagesAgenda of The 110th Regular SessionCdeoCityCouncilPas encore d'évaluation

- Certificate of Appearance 2023Document3 pagesCertificate of Appearance 2023Armando Mendoza Jr.Pas encore d'évaluation

- BIR FORM 2307 SampleDocument6 pagesBIR FORM 2307 SampleEasyHear Philippines by NuGen Hearing Devices, Inc.Pas encore d'évaluation

- Donation LetterDocument1 pageDonation LetterKangPas encore d'évaluation

- A AtcDocument2 pagesA Atckupalking100% (1)

- FinalDocument2 pagesFinalJessica FordPas encore d'évaluation

- Orientation On Gender and Development (GAD) Basic Guidelines and Mandates For The Education SectorDocument28 pagesOrientation On Gender and Development (GAD) Basic Guidelines and Mandates For The Education SectormelizzePas encore d'évaluation

- Women, Gender and Society: Soc/WMST 308Document11 pagesWomen, Gender and Society: Soc/WMST 308melizzePas encore d'évaluation

- Concepts, Policies, Principles and MandatesDocument36 pagesConcepts, Policies, Principles and MandatesmelizzePas encore d'évaluation

- Module 10 Violence Against WomenDocument39 pagesModule 10 Violence Against WomenmelizzePas encore d'évaluation

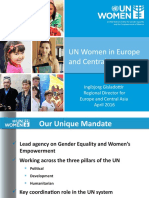

- 9 GEC Meeting Presentation Ingibjorg Gisladottir UNWOMENDocument17 pages9 GEC Meeting Presentation Ingibjorg Gisladottir UNWOMENmelizzePas encore d'évaluation

- System Development of Market Mobile Application For Sustainable Local Industry in The Philippines by Analiza v. MuñozDocument23 pagesSystem Development of Market Mobile Application For Sustainable Local Industry in The Philippines by Analiza v. MuñozmelizzePas encore d'évaluation

- AnnounceDocument6 pagesAnnouncemelizzePas encore d'évaluation

- nrcs142p2 031587Document17 pagesnrcs142p2 031587melizzePas encore d'évaluation

- The Future of Development AdministrationDocument10 pagesThe Future of Development AdministrationmelizzePas encore d'évaluation

- Anonymized Competency Based Recruitment and Selection ProcessDocument17 pagesAnonymized Competency Based Recruitment and Selection ProcessmelizzePas encore d'évaluation

- Announcement No. 63, S. 2018Document1 pageAnnouncement No. 63, S. 2018melizzePas encore d'évaluation

- Announcement No 07 S 2017Document2 pagesAnnouncement No 07 S 2017melizzePas encore d'évaluation

- Managing Across CulturesDocument12 pagesManaging Across CulturesmelizzePas encore d'évaluation

- How To Write A Feasibility StudyDocument34 pagesHow To Write A Feasibility StudymelizzePas encore d'évaluation

- MC 19 S 1999Document40 pagesMC 19 S 1999melizzePas encore d'évaluation

- Optimize Operations with OR ToolsDocument50 pagesOptimize Operations with OR ToolsmelizzePas encore d'évaluation

- INTERNATIONAL MANAGEMENT+questionsDocument21 pagesINTERNATIONAL MANAGEMENT+questionsmelizzePas encore d'évaluation

- CS Reporter 2nd Quarter 2018 IssueDocument40 pagesCS Reporter 2nd Quarter 2018 IssuemelizzePas encore d'évaluation

- International Management+QuestionsDocument4 pagesInternational Management+QuestionsAli Arnaouti100% (1)

- DGSND - Gov.in CgoDocument3 pagesDGSND - Gov.in CgosselmtpdrPas encore d'évaluation

- Great DepressionDocument44 pagesGreat Depressiondaniel watson58% (12)

- Project FinanceDocument10 pagesProject FinanceElj LabPas encore d'évaluation

- Surrender FormDocument2 pagesSurrender Formvi_sharPas encore d'évaluation

- Apollo Munich Optima Restore BrochureDocument2 pagesApollo Munich Optima Restore BrochureAmit SawantPas encore d'évaluation

- Financial Institutions Markets and ServicesDocument2 pagesFinancial Institutions Markets and ServicesPavneet Kaur Bhatia100% (1)

- FlexiproDocument5 pagesFlexiprotanelynnnn01Pas encore d'évaluation

- The Oriental Insurance Company LimitedDocument3 pagesThe Oriental Insurance Company Limitedecommerce11.2020Pas encore d'évaluation

- Concept of InsuranceDocument4 pagesConcept of InsuranceNazrul HoquePas encore d'évaluation

- 17 Altprob 7eDocument6 pages17 Altprob 7eAshish BhallaPas encore d'évaluation

- SUNLIFE v. Sandra Tan KitDocument14 pagesSUNLIFE v. Sandra Tan KitAngelie AbangPas encore d'évaluation

- Nefas Silk Poly Technic College: Learning GuideDocument39 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuPas encore d'évaluation

- D037434231 980906345227435 TpschedulescDocument2 pagesD037434231 980906345227435 Tpschedulescpratish mokashiPas encore d'évaluation

- Company ProfileDocument13 pagesCompany ProfileTerefe Gebremariam AregehagnPas encore d'évaluation

- Tio Khe Chio V Court of Appeals (202 SCRA 119)Document5 pagesTio Khe Chio V Court of Appeals (202 SCRA 119)katherine magbanuaPas encore d'évaluation

- Just Energy Assurance of Discontinuance-REDUCEDDocument58 pagesJust Energy Assurance of Discontinuance-REDUCEDheatherloneyPas encore d'évaluation

- Senate Finds Massive Fraud Washington Mutual Special Delivery For Wamu VictimsDocument666 pagesSenate Finds Massive Fraud Washington Mutual Special Delivery For Wamu Victimsthomasfamily98_68860Pas encore d'évaluation

- 2Document3 pages2Ruth TenajerosPas encore d'évaluation

- Thorsten Beck, Heiko Hesse, Thomas Kick and Natalja Von Westernhagen (2009)Document61 pagesThorsten Beck, Heiko Hesse, Thomas Kick and Natalja Von Westernhagen (2009)Ahmad KhaliqPas encore d'évaluation

- Contribution of Insurance Sector in Nepalese EconomyDocument10 pagesContribution of Insurance Sector in Nepalese EconomySharad Pyakurel100% (1)