Vous aimerez peut-être aussi

- List of ItemsDocument1 pageList of ItemsUpasana GuptaPas encore d'évaluation

- ToyotaDocument1 pageToyotaUpasana GuptaPas encore d'évaluation

- Japan's Aging Population: Crisis or Manageable ProblemDocument24 pagesJapan's Aging Population: Crisis or Manageable ProblemUpasana GuptaPas encore d'évaluation

- Steps For GameDocument2 pagesSteps For GameUpasana GuptaPas encore d'évaluation

- Upasana TdesDocument12 pagesUpasana TdesUpasana GuptaPas encore d'évaluation

- Things To Do - Daily BasisDocument2 pagesThings To Do - Daily BasisUpasana GuptaPas encore d'évaluation

- Questions: Nature & Scope of Marketing Core ConceptsDocument5 pagesQuestions: Nature & Scope of Marketing Core ConceptsUpasana GuptaPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Economic CrisisDocument3 pagesEconomic Crisisshoaibishrat_87Pas encore d'évaluation

- The Great Depression Scavenger HuntDocument2 pagesThe Great Depression Scavenger Huntvickiajones60% (5)

- List of Stock Market Crashes and Bear Markets - Wikipedia PDFDocument22 pagesList of Stock Market Crashes and Bear Markets - Wikipedia PDFBhanwar Singh ParmarPas encore d'évaluation

- Bfs Foreclosed Properties For Sales As of 2017-01-10Document25 pagesBfs Foreclosed Properties For Sales As of 2017-01-10Ren MacatangayPas encore d'évaluation

- Reinforcing Causal LoopDocument1 pageReinforcing Causal LoopMark Billy EspinosaPas encore d'évaluation

- Witn LehmanDocument2 pagesWitn LehmanpurnomoPas encore d'évaluation

- APUSH SynthesisDocument1 pageAPUSH SynthesisthaticeskatergirlPas encore d'évaluation

- Lecture 16Document12 pagesLecture 16Tanya SinghPas encore d'évaluation

- Project 3 FinalDocument11 pagesProject 3 Finalapi-261340346Pas encore d'évaluation

- Lessons From Collapse - Lehman Brothers (Eco)Document19 pagesLessons From Collapse - Lehman Brothers (Eco)sweet_hitiksha299942Pas encore d'évaluation

- Debt Elimination Discharge Set Off, Law, TruthDocument5 pagesDebt Elimination Discharge Set Off, Law, TruthLandiBrown100% (7)

- Understanding the Global Financial CrisisDocument13 pagesUnderstanding the Global Financial CrisisvarshikaPas encore d'évaluation

- Global Financial Crisis-TgDocument4 pagesGlobal Financial Crisis-TgCharlesPas encore d'évaluation

- Financial Crisis and Its Effect On BanksDocument5 pagesFinancial Crisis and Its Effect On BanksTejo SajjaPas encore d'évaluation

- Us Foreclosure Lists March 2019Document113 pagesUs Foreclosure Lists March 2019Virginia HolmesPas encore d'évaluation

- Financial CrisisDocument25 pagesFinancial Crisisnuwan tharakaPas encore d'évaluation

- 2016 05 11 - Southey Capital Distressed and Illiquid PricingDocument8 pages2016 05 11 - Southey Capital Distressed and Illiquid PricingSouthey CapitalPas encore d'évaluation

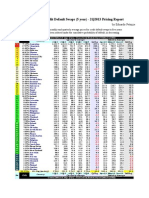

- Sovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportDocument1 pageSovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportEduardo PetazzePas encore d'évaluation

- Timeline of The Lehman Brothers CollapseDocument3 pagesTimeline of The Lehman Brothers CollapseJonas MondalaPas encore d'évaluation

- FC08: Causes and Consequences of the 2008 Financial CrisisDocument16 pagesFC08: Causes and Consequences of the 2008 Financial CrisisSchanzae ShabbirPas encore d'évaluation

- New Deal Alphabet Soup WorksheetDocument3 pagesNew Deal Alphabet Soup Worksheetapi-348656364100% (1)

- All The Devils Are HereDocument1 pageAll The Devils Are Heresudhanshur0% (3)

- PS Forclosure ReportDocument2 pagesPS Forclosure ReportJustin HendrixPas encore d'évaluation

- Euro Crisis For Dummies PDFDocument2 pagesEuro Crisis For Dummies PDFLauraPas encore d'évaluation

- Financial Crisis - Group 6Document10 pagesFinancial Crisis - Group 6Anonymous ZCvBMCO9Pas encore d'évaluation

- CDOs and Synthetic CDOs ExplainedDocument3 pagesCDOs and Synthetic CDOs ExplainedJIGYASA KUMARIPas encore d'évaluation

- BFS Property Listing For Posting As of 02.01.2019 Public FinalDocument11 pagesBFS Property Listing For Posting As of 02.01.2019 Public FinalNicole Paola Liva TalingtingPas encore d'évaluation

- Combating The Judicial Foreclosure Slaughterhouse Aug 4th 530pm West Palm Beach FL Monthly Happy HourDocument1 pageCombating The Judicial Foreclosure Slaughterhouse Aug 4th 530pm West Palm Beach FL Monthly Happy HourForeclosure FraudPas encore d'évaluation

- The Stock Market Crash and The Great DepressionDocument10 pagesThe Stock Market Crash and The Great DepressionJaysonPas encore d'évaluation

- BFS All Foreclosed Properties for sale as of December 15, 2016Document20 pagesBFS All Foreclosed Properties for sale as of December 15, 2016xandie_sacroPas encore d'évaluation