Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Or Wcomp 0.72 or Wcomp 0.72Document1 pageOr Wcomp 0.72 or Wcomp 0.72aaronPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- CivPro RianoDocument219 pagesCivPro Rianojose100% (5)

- Corpo Law - SummarizedDocument119 pagesCorpo Law - SummarizedCelestino LawPas encore d'évaluation

- Arundeep's Icse History and Civics Mcq+Subjective Class 10 Final SampleDocument26 pagesArundeep's Icse History and Civics Mcq+Subjective Class 10 Final SampleSUVRA GAMING67% (3)

- Fire InsuranceDocument4 pagesFire InsuranceRoMeoPas encore d'évaluation

- La Planeación en La Gestión Pública Del Siglo XX: Planning in Public of The Twentieth CenturyDocument35 pagesLa Planeación en La Gestión Pública Del Siglo XX: Planning in Public of The Twentieth CenturyAngie Sierra VegaPas encore d'évaluation

- JPM Q3 EarningsDocument25 pagesJPM Q3 EarningsZerohedgePas encore d'évaluation

- Navigating The New Normal David A. RosenbergDocument73 pagesNavigating The New Normal David A. Rosenbergannawitkowski88Pas encore d'évaluation

- People V JP Morgan ComplaintDocument31 pagesPeople V JP Morgan ComplaintJames EdwardsPas encore d'évaluation

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 pagesExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Pas encore d'évaluation

- OSAM TheBigPicture 150ppi Arial-JPOS EditDocument28 pagesOSAM TheBigPicture 150ppi Arial-JPOS Editannawitkowski88Pas encore d'évaluation

- TBP Conf Oct 2012Document27 pagesTBP Conf Oct 2012annawitkowski88Pas encore d'évaluation

- OCT7BRDocument2 pagesOCT7BRannawitkowski88Pas encore d'évaluation

- Single SlideDocument1 pageSingle Slideannawitkowski88Pas encore d'évaluation

- Research Division: Federal Reserve Bank of St. LouisDocument43 pagesResearch Division: Federal Reserve Bank of St. Louisannawitkowski88Pas encore d'évaluation

- SSRN Id2023011Document54 pagesSSRN Id2023011sterkejanPas encore d'évaluation

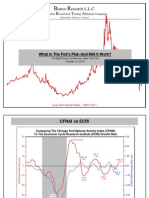

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Document44 pagesIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88Pas encore d'évaluation

- Gurtin Fixed Income Presentation - TBP Conference - 10.4.12Document16 pagesGurtin Fixed Income Presentation - TBP Conference - 10.4.12annawitkowski88Pas encore d'évaluation

- Richmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative AssessmentDocument11 pagesRichmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative Assessmentannawitkowski88Pas encore d'évaluation

- MBIA Vs Countrywide - Schedule Summary Judgement For Primary Liability Hearing On Nov 14th and 15th, 2012Document4 pagesMBIA Vs Countrywide - Schedule Summary Judgement For Primary Liability Hearing On Nov 14th and 15th, 2012annawitkowski88Pas encore d'évaluation

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- KPMG Pcaob 2012Document31 pagesKPMG Pcaob 2012Caleb NewquistPas encore d'évaluation

- Top 1 PercentDocument1 pageTop 1 Percentannawitkowski88Pas encore d'évaluation

- Exhibit 2 - Whistleblower Transcript (Redacted)Document56 pagesExhibit 2 - Whistleblower Transcript (Redacted)annawitkowski88Pas encore d'évaluation

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 pagesExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Pas encore d'évaluation

- Bartlett Laffer 2Document3 pagesBartlett Laffer 2annawitkowski88Pas encore d'évaluation

- Fed SideDocument1 pageFed Sideannawitkowski88Pas encore d'évaluation

- Federal ReserveDocument5 pagesFederal Reserveannawitkowski88Pas encore d'évaluation

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- FHFA OIG Report On Freddie MacDocument21 pagesFHFA OIG Report On Freddie MacForeclosure FraudPas encore d'évaluation

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Pas encore d'évaluation

- Fed SideDocument1 pageFed Sideannawitkowski88Pas encore d'évaluation

- Friction and Housing Market DynamicsDocument52 pagesFriction and Housing Market DynamicsLori NoblePas encore d'évaluation

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Pas encore d'évaluation

- Policy Insight 63Document13 pagesPolicy Insight 63annawitkowski88Pas encore d'évaluation

- Ronald ReaganDocument6 pagesRonald ReaganVictoria VeringaPas encore d'évaluation

- Digest Labor RemainingDocument6 pagesDigest Labor RemainingPaul Christopher PinedaPas encore d'évaluation

- Travis Laney DBA TJ Laney Trucking CC1703195 - AL Policy (TN)Document34 pagesTravis Laney DBA TJ Laney Trucking CC1703195 - AL Policy (TN)Caroline ColePas encore d'évaluation

- M C Mehta V Kamal NathDocument12 pagesM C Mehta V Kamal NathNavaneeth NeonPas encore d'évaluation

- Compagnie Financiere Sucres Et Denrees vs. Commissioner of Internal RevenueDocument5 pagesCompagnie Financiere Sucres Et Denrees vs. Commissioner of Internal RevenuejafernandPas encore d'évaluation

- Team Code - R-430 Before The Hon'Ble High Court of Wakanda: W.P. (C) N - 2020Document23 pagesTeam Code - R-430 Before The Hon'Ble High Court of Wakanda: W.P. (C) N - 2020kumar PritamPas encore d'évaluation

- The Philippine Environmental Assessment PoliciesDocument20 pagesThe Philippine Environmental Assessment PoliciesKringPas encore d'évaluation

- AO2012-0007-A Guidelines On The Grant of 20% Discount To Senior Citizens On Health-Related Goods and For Other Purposes (05-05)Document3 pagesAO2012-0007-A Guidelines On The Grant of 20% Discount To Senior Citizens On Health-Related Goods and For Other Purposes (05-05)Leah Rose Figueroa ParasPas encore d'évaluation

- Mitsubishi vs. BOCDocument6 pagesMitsubishi vs. BOCjoyfandialanPas encore d'évaluation

- White House Dinner Party Lesson PlanDocument9 pagesWhite House Dinner Party Lesson PlanJeff HollidayPas encore d'évaluation

- 138673-1978-People v. Galapia y Bacus PDFDocument7 pages138673-1978-People v. Galapia y Bacus PDFLeona SanchezPas encore d'évaluation

- Oath Keepers J6: Jason Dolan STMNT of Offense From Plea DealDocument6 pagesOath Keepers J6: Jason Dolan STMNT of Offense From Plea DealPatriots Soapbox InternalPas encore d'évaluation

- TEMPOCARDDocument25 pagesTEMPOCARDButch NorielPas encore d'évaluation

- Appeal Judgment Best V Minister of Home Affairs2Document41 pagesAppeal Judgment Best V Minister of Home Affairs2BernewsAdminPas encore d'évaluation

- Reaction - BATASDocument3 pagesReaction - BATASAISA BANSILPas encore d'évaluation

- A Documentacion CapecoDocument153 pagesA Documentacion CapecoDiálogo100% (1)

- I. Omnibus Election Code (Sec 118)Document43 pagesI. Omnibus Election Code (Sec 118)Jose Antonio BarrosoPas encore d'évaluation

- Zaccheo V UniversalDocument31 pagesZaccheo V UniversalTHROnlinePas encore d'évaluation

- Response and Objection To Motion To Reconsider VenueDocument3 pagesResponse and Objection To Motion To Reconsider Venuekc wildmoonPas encore d'évaluation

- Santillon vs. Miranda, 14 SCRA 563 (1965)Document8 pagesSantillon vs. Miranda, 14 SCRA 563 (1965)Luna KimPas encore d'évaluation

- Family LawDocument13 pagesFamily Lawshruti mandoraPas encore d'évaluation

- Western Sahara (Advisory Opinion) : Clemens FeinäugleDocument5 pagesWestern Sahara (Advisory Opinion) : Clemens Feinäuglejaleelh9898Pas encore d'évaluation

- Simon v. CHR, G.R. No. 100150, 5 January 1994Document14 pagesSimon v. CHR, G.R. No. 100150, 5 January 1994Jazem AnsamaPas encore d'évaluation

- People V HadjiDocument8 pagesPeople V HadjiCMLPas encore d'évaluation