Vous aimerez peut-être aussi

- TBP Conf Oct 2012Document27 pagesTBP Conf Oct 2012annawitkowski88Pas encore d'évaluation

- Single SlideDocument1 pageSingle Slideannawitkowski88Pas encore d'évaluation

- People V JP Morgan ComplaintDocument31 pagesPeople V JP Morgan ComplaintJames EdwardsPas encore d'évaluation

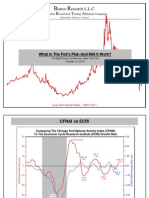

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Document44 pagesIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88Pas encore d'évaluation

- SSRN Id2023011Document54 pagesSSRN Id2023011sterkejanPas encore d'évaluation

- Richmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative AssessmentDocument11 pagesRichmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative Assessmentannawitkowski88Pas encore d'évaluation

- Research Division: Federal Reserve Bank of St. LouisDocument43 pagesResearch Division: Federal Reserve Bank of St. Louisannawitkowski88Pas encore d'évaluation

- The Boom and Bust of U.S. Housing Prices From Various Geographic PerspectivesDocument29 pagesThe Boom and Bust of U.S. Housing Prices From Various Geographic Perspectivesannawitkowski88Pas encore d'évaluation

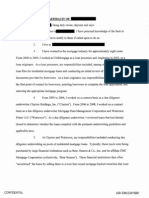

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 pagesExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Pas encore d'évaluation

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- Fed SideDocument1 pageFed Sideannawitkowski88Pas encore d'évaluation

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Pas encore d'évaluation

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Pas encore d'évaluation

- Woodford Rules Jackson Hole WyomingDocument97 pagesWoodford Rules Jackson Hole WyominglatecirclePas encore d'évaluation

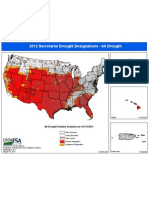

- Usda Drought Fast Track Designations 081512Document1 pageUsda Drought Fast Track Designations 081512annawitkowski88Pas encore d'évaluation

- Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CDocument36 pagesFinance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.Cannawitkowski88Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Case Digest Obligations of PartnersDocument8 pagesCase Digest Obligations of PartnersAnonymous STwyFh5uOPas encore d'évaluation

- 6 Advanced Accounting 2DDocument3 pages6 Advanced Accounting 2DRizky Nugroho SantosoPas encore d'évaluation

- Confirmatory Order Against Mohit Aggarwal in The Matter of Radford Global Ltd.Document3 pagesConfirmatory Order Against Mohit Aggarwal in The Matter of Radford Global Ltd.Shyam SunderPas encore d'évaluation

- Montes Et Al. (2016)Document16 pagesMontes Et Al. (2016)DiegoPachecoPas encore d'évaluation

- Cost Management Problems CA FinalDocument266 pagesCost Management Problems CA Finalksaqib89100% (1)

- Union Bank of IndiaDocument58 pagesUnion Bank of IndiaNitinAgnihotriPas encore d'évaluation

- Portfolio & Investment Analysis Efficient-Market HypothesisDocument137 pagesPortfolio & Investment Analysis Efficient-Market HypothesisVicky GowePas encore d'évaluation

- WHT ManualDocument166 pagesWHT ManualFaizan HyderPas encore d'évaluation

- Term-Lending Financial Institbttl (Qns India Level: Unit 11 ALLDocument15 pagesTerm-Lending Financial Institbttl (Qns India Level: Unit 11 ALLSiva Venkata RamanaPas encore d'évaluation

- CCCR ProjectDocument17 pagesCCCR ProjectVincsPas encore d'évaluation

- 14Document69 pages14Shoniqua Johnson100% (2)

- REAL 209 Midterm II Study GuideDocument4 pagesREAL 209 Midterm II Study GuidejuanPas encore d'évaluation

- CFPB Arbitration Letter 08.03.16Document8 pagesCFPB Arbitration Letter 08.03.16MarkWarnerPas encore d'évaluation

- Handout Caltex VS IacDocument4 pagesHandout Caltex VS IacKazumi ShioriPas encore d'évaluation

- Pac CarbonDocument172 pagesPac CarbonBob MackinPas encore d'évaluation

- History of Mutual FundDocument2 pagesHistory of Mutual FundArchana VishwakarmaPas encore d'évaluation

- BMATH 3rd Quarter Short and Long QuizDocument128 pagesBMATH 3rd Quarter Short and Long QuizEstephanie Abadz73% (11)

- TransactionHistory 3236776565Document2 pagesTransactionHistory 3236776565Badrulsyafiq -Pas encore d'évaluation

- 07 Trade Investment and Development Corp v. Asia Paces Corp.Document17 pages07 Trade Investment and Development Corp v. Asia Paces Corp.gabbyborPas encore d'évaluation

- Radio One Inc: M&A Case StudyDocument11 pagesRadio One Inc: M&A Case StudyRishav AgarwalPas encore d'évaluation

- 9780521461566Document303 pages9780521461566kronobonoPas encore d'évaluation

- Accounting Standard 6Document54 pagesAccounting Standard 6Sushil DixitPas encore d'évaluation

- IT Detections From Gross Total Income Pt-1Document25 pagesIT Detections From Gross Total Income Pt-1syedfareed596100% (1)

- Spring Sales BrochureDocument13 pagesSpring Sales BrochureGuy SparkesPas encore d'évaluation

- Unit 20 and 21 - Derivatives and CommoditiesDocument6 pagesUnit 20 and 21 - Derivatives and CommoditiesHemant bhanawatPas encore d'évaluation

- Judicial Affidavit Collection of Sum of MoneyDocument4 pagesJudicial Affidavit Collection of Sum of Moneypatricia.aniya80% (5)

- Mycem CementDocument89 pagesMycem CementushadgsPas encore d'évaluation

- 14 Financial Statement Analysis: Chapter SummaryDocument12 pages14 Financial Statement Analysis: Chapter SummaryGeoffrey Rainier CartagenaPas encore d'évaluation

- Anwar Ibrahim and The Money MachineDocument13 pagesAnwar Ibrahim and The Money MachineMalaysia_PoliticsPas encore d'évaluation

- Bus 306 Exam 2 - Fall 2012 (A) - SolutionDocument15 pagesBus 306 Exam 2 - Fall 2012 (A) - SolutionCyn SyjucoPas encore d'évaluation