Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Ubben ValueInvestingCongress 100212Document27 pagesUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Third Point Q3 2012 Investor Letter TPOIDocument11 pagesThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Value Investing Congress Presentation-Tilson-10!1!12Document93 pagesValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Mauldin ValueInvestingCongress 100112Document11 pagesMauldin ValueInvestingCongress 100112VALUEWALK LLCPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- 8th Annual New York: Value Investing CongressDocument53 pages8th Annual New York: Value Investing CongressVALUEWALK LLCPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Roepers ValueInvestingCongress 100212Document30 pagesRoepers ValueInvestingCongress 100212VALUEWALK LLCPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Best of Charlie Munger 1994 2011Document349 pagesThe Best of Charlie Munger 1994 2011VALUEWALK LLC100% (6)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- 8th Annual New York: Value Investing CongressDocument46 pages8th Annual New York: Value Investing CongressVALUEWALK LLCPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- 8th Annual New York: Value Investing CongressDocument51 pages8th Annual New York: Value Investing CongressVALUEWALK LLCPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- Ghazi ValueInvestingCongress 100112Document70 pagesGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- Buckley ValueInvestingCongress 100112Document45 pagesBuckley ValueInvestingCongress 100112VALUEWALK LLCPas encore d'évaluation

- McGuire ValueInvestingCongress 100112Document70 pagesMcGuire ValueInvestingCongress 100112VALUEWALK LLCPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Rockstone Research VDR1 EnglishDocument28 pagesRockstone Research VDR1 EnglishVALUEWALK LLC100% (1)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- TAF 3Q 2012 Report and Shareholder LettersDocument77 pagesTAF 3Q 2012 Report and Shareholder LettersVALUEWALK LLCPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDocument8 pagesGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilantePas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Rockstone Research URS1 EnglishDocument32 pagesRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- SHLDDocument18 pagesSHLDduwe7809100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Buffett in Beijing Report JuneDocument15 pagesBuffett in Beijing Report JuneVALUEWALK LLCPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- MW Edu 07182012Document97 pagesMW Edu 07182012VALUEWALK LLCPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- Greenlight Q2 Letter To InvestorsDocument5 pagesGreenlight Q2 Letter To InvestorsVALUEWALK LLCPas encore d'évaluation

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCPas encore d'évaluation

- T2 Accredited Fund Letter To Investors June 12Document10 pagesT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCPas encore d'évaluation

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Document15 pagesMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugPas encore d'évaluation

- HP PresentationDocument69 pagesHP Presentationssc320Pas encore d'évaluation

- GMCR Profits Overstated or MisunderstoodDocument8 pagesGMCR Profits Overstated or MisunderstoodVALUEWALK LLCPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Dan Loeb Hedge Fund Letter June 2012Document2 pagesDan Loeb Hedge Fund Letter June 2012VALUEWALK LLCPas encore d'évaluation

- R. A. Podar College of Commerce and Economics:, (Autonomous)Document45 pagesR. A. Podar College of Commerce and Economics:, (Autonomous)Rashi thiPas encore d'évaluation

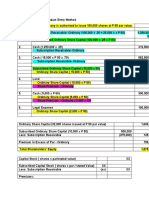

- Valix Chapter 20Document22 pagesValix Chapter 20criszel4sobejanaPas encore d'évaluation

- High-Frequency Trading, Order Types, and The Evolution of The Securities Market StructureDocument31 pagesHigh-Frequency Trading, Order Types, and The Evolution of The Securities Market StructuretabbforumPas encore d'évaluation

- Influencer Marketing Proposal 5Document11 pagesInfluencer Marketing Proposal 5Paul0% (1)

- Bladex - Yankee CD Info MemoDocument2 pagesBladex - Yankee CD Info MemoGuido ValderramaPas encore d'évaluation

- Darwin Capuno PT 2 Las 4Document3 pagesDarwin Capuno PT 2 Las 4Darwin CapunoPas encore d'évaluation

- Recognition and MeasurementDocument16 pagesRecognition and MeasurementajishPas encore d'évaluation

- Define AccountingDocument28 pagesDefine Accountingheart lelimPas encore d'évaluation

- Secondary Markets ExplainedDocument27 pagesSecondary Markets ExplainedNhi VõPas encore d'évaluation

- Mba Mba Batchno 171Document104 pagesMba Mba Batchno 171Different Point100% (1)

- KCM Valuation ReportDocument228 pagesKCM Valuation Reportpldev100% (1)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- BRS Statement IllustrationsDocument3 pagesBRS Statement Illustrationssurekha khandebharadPas encore d'évaluation

- A real value risk model for emerging marketsDocument35 pagesA real value risk model for emerging marketsbutch28butch28Pas encore d'évaluation

- Book BuildingDocument19 pagesBook Buildingmonilsonaiya_91Pas encore d'évaluation

- F2022 Z Midterm AnalyticalDocument6 pagesF2022 Z Midterm AnalyticalRonak Jyot KlerPas encore d'évaluation

- Options, Futures, and Other Derivatives, 8th Edition, 1Document25 pagesOptions, Futures, and Other Derivatives, 8th Edition, 1Anissa Nurlia KusumaningtyasPas encore d'évaluation

- Analyisis Report Tesla Statement of ConditionDocument13 pagesAnalyisis Report Tesla Statement of ConditionAmel BarghutiPas encore d'évaluation

- AFAR TestbankDocument56 pagesAFAR TestbankDrama SubsPas encore d'évaluation

- CFAS Week 2 OverviewDocument21 pagesCFAS Week 2 OverviewJohnray ParanPas encore d'évaluation

- Study on Performance of SBI Merchant BankingDocument73 pagesStudy on Performance of SBI Merchant BankingSonia Jacob50% (4)

- Executive Summary: Financial AnalysisDocument67 pagesExecutive Summary: Financial AnalysisSachin JainPas encore d'évaluation

- Valuation Models Summary: Discounted Cash Flow and Relative Valuation ApproachesDocument47 pagesValuation Models Summary: Discounted Cash Flow and Relative Valuation Approachesarmani2coolPas encore d'évaluation

- UTS Pengantar Akutansi 2Document3 pagesUTS Pengantar Akutansi 2Pia panPas encore d'évaluation

- 2021 Q1 Investor Letter Desert Lion Capital Non LPsDocument10 pages2021 Q1 Investor Letter Desert Lion Capital Non LPsYog MehtaPas encore d'évaluation

- KBSL - Branded Retail SectorDocument30 pagesKBSL - Branded Retail SectorRahulPas encore d'évaluation

- Dcom510 Financial DerivativesDocument238 pagesDcom510 Financial DerivativesRavi Kant sfs 1Pas encore d'évaluation

- Fimm 04.01.2021Document427 pagesFimm 04.01.2021srinivasPas encore d'évaluation

- Nism PGPSM Placements Batch 2012 13Document24 pagesNism PGPSM Placements Batch 2012 13P.A. Vinay KumarPas encore d'évaluation

- AccountingDocument7 pagesAccountingAnnaPas encore d'évaluation

- Role of FIIs in Volatility of Indian Stock MarketDocument58 pagesRole of FIIs in Volatility of Indian Stock MarketAniket SharmaPas encore d'évaluation