Vous aimerez peut-être aussi

- SAPM 1st Internal Assessment Test QPDocument2 pagesSAPM 1st Internal Assessment Test QPVasantha NaikPas encore d'évaluation

- TT Handbook ImportanceDocument2 pagesTT Handbook ImportanceVasantha NaikPas encore d'évaluation

- What Is SwapDocument2 pagesWhat Is SwapVasantha NaikPas encore d'évaluation

- Prepared By: Puneet Sharma Vinay Patidar Viyappu Tharun Siddharth Khandelwal Rishu SinghDocument23 pagesPrepared By: Puneet Sharma Vinay Patidar Viyappu Tharun Siddharth Khandelwal Rishu SinghVasantha NaikPas encore d'évaluation

- Managing Commodity Price and Supply Risk: George A. Zsidisin, PH.D., C.P.MDocument34 pagesManaging Commodity Price and Supply Risk: George A. Zsidisin, PH.D., C.P.MVasantha NaikPas encore d'évaluation

- Challenges Amid The Global Economic Storm: Northwest Insurance Council 2009 Annual Luncheon Seattle, WA January 27, 2009Document70 pagesChallenges Amid The Global Economic Storm: Northwest Insurance Council 2009 Annual Luncheon Seattle, WA January 27, 2009Vasantha NaikPas encore d'évaluation

- R R R R: BA 440 Final Formula SheetDocument3 pagesR R R R: BA 440 Final Formula SheetVasantha NaikPas encore d'évaluation

- VasanthDocument2 pagesVasanthVasantha NaikPas encore d'évaluation

- Chap 5 - Vouching PDFDocument0 pageChap 5 - Vouching PDFVasantha NaikPas encore d'évaluation

- 2012 International Conference On Economics and Finance Research, IPEDR Vol.32 (2012)Document1 page2012 International Conference On Economics and Finance Research, IPEDR Vol.32 (2012)Vasantha NaikPas encore d'évaluation

- English Wheat LeafletDocument2 pagesEnglish Wheat LeafletVasantha NaikPas encore d'évaluation

- Testing Weak Form Efficiency For Indian Derivatives MarketDocument4 pagesTesting Weak Form Efficiency For Indian Derivatives MarketVasantha NaikPas encore d'évaluation

- 617746389Document6 pages617746389Vasantha NaikPas encore d'évaluation

- Expiration-Day Effects of The All Ordinaries Share Price Index Futures: Empirical Evidence and Alternative Settlement ProceduresDocument36 pagesExpiration-Day Effects of The All Ordinaries Share Price Index Futures: Empirical Evidence and Alternative Settlement ProceduresVasantha NaikPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

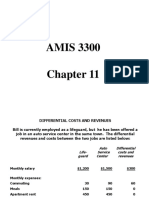

- Ch11PPSpring2016 1q5mpc0Document20 pagesCh11PPSpring2016 1q5mpc0RiskaPas encore d'évaluation

- Financial Analysis: 3.1. Consolidated Statement of Financial PositionDocument14 pagesFinancial Analysis: 3.1. Consolidated Statement of Financial PositionTalha Iftekhar Khan SwatiPas encore d'évaluation

- Payroll Management Software India - Best Online Payroll Software ?Document5 pagesPayroll Management Software India - Best Online Payroll Software ?Naveen Kumar NaiduPas encore d'évaluation

- PWC SWOT & Ratio AnalysisDocument10 pagesPWC SWOT & Ratio AnalysisRTS123asdfPas encore d'évaluation

- Classic Pen Case CMADocument2 pagesClassic Pen Case CMARheaPradhanPas encore d'évaluation

- Reading 20 Discounted Dividend ValuationDocument55 pagesReading 20 Discounted Dividend Valuationdhanh.bdn.hsv.neuPas encore d'évaluation

- TX 105 Estate TaxDocument2 pagesTX 105 Estate TaxRose Kristy SindayenPas encore d'évaluation

- Grant ProcedureDocument4 pagesGrant ProcedurerahulPas encore d'évaluation

- United States Court of Appeals, Eleventh CircuitDocument18 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsPas encore d'évaluation

- NAV As at 29th January 2021Document33 pagesNAV As at 29th January 2021Avinash GanesanPas encore d'évaluation

- Projected Cash Income For The Year 2021-2025 RevenuesDocument9 pagesProjected Cash Income For The Year 2021-2025 RevenuesAllia AntalanPas encore d'évaluation

- RHB-Product Disclosure Sheet-Personal FinancingDocument4 pagesRHB-Product Disclosure Sheet-Personal FinancingMohd Imran NoordinPas encore d'évaluation

- Worldwatch Institute, Jamaica Sustainable Energy Roadmap, October 2013Document199 pagesWorldwatch Institute, Jamaica Sustainable Energy Roadmap, October 2013Detlef LoyPas encore d'évaluation

- Option StrategiesDocument13 pagesOption StrategiesArunangshu BhattacharjeePas encore d'évaluation

- SBA Topic 1-Taylor Corporation-SolutionsDocument2 pagesSBA Topic 1-Taylor Corporation-SolutionsAli BasyaPas encore d'évaluation

- Review of Literature: Chapter-2Document5 pagesReview of Literature: Chapter-2Juan JacksonPas encore d'évaluation

- Financial Markets: Financial Markets (FMS) Are Organised and Highly RegulatedDocument12 pagesFinancial Markets: Financial Markets (FMS) Are Organised and Highly RegulatedShivain RoopraiPas encore d'évaluation

- 60 Year Intervals and October PanicsDocument3 pages60 Year Intervals and October Panicstrb301Pas encore d'évaluation

- The Definition of Small Business ManagementDocument2 pagesThe Definition of Small Business ManagementKul DeepPas encore d'évaluation

- Intercompany Accounting For Internal Order and Drop ShipmentDocument51 pagesIntercompany Accounting For Internal Order and Drop Shipmentrachaiah.vr9878Pas encore d'évaluation

- Geogia Filing Scott AndersonDocument2 pagesGeogia Filing Scott AndersonForeclosure FraudPas encore d'évaluation

- The Improved R2 StrategyDocument4 pagesThe Improved R2 Strategyhusserl01Pas encore d'évaluation

- Georgia Shacks Produces Small Outdoor Buildings The Company BegDocument1 pageGeorgia Shacks Produces Small Outdoor Buildings The Company BegAmit PandeyPas encore d'évaluation

- ASHMEAD-BARTLETT, E. - The Passing of The Shereefian Empire PDFDocument618 pagesASHMEAD-BARTLETT, E. - The Passing of The Shereefian Empire PDFbenshys100% (2)

- Case-Study - Laura Ashley.Document16 pagesCase-Study - Laura Ashley.inesvilafanhaPas encore d'évaluation

- State Investment Vs CA and MoulicDocument10 pagesState Investment Vs CA and MoulicArlyn R. RetardoPas encore d'évaluation

- Prospect Theory - Bounded RationalityDocument57 pagesProspect Theory - Bounded RationalityalishehzadPas encore d'évaluation

- APTB - A-SME PLATINUM-i - Application Form (SST) PDFDocument16 pagesAPTB - A-SME PLATINUM-i - Application Form (SST) PDFMuizz LynnPas encore d'évaluation

- Interim Order in Respect of Nirmal Infrahome Corporation LTDDocument24 pagesInterim Order in Respect of Nirmal Infrahome Corporation LTDShyam SunderPas encore d'évaluation

- Profit Planning, Activity-Based Budgeting, and E-Budgeting: Answers To Review QuestionsDocument73 pagesProfit Planning, Activity-Based Budgeting, and E-Budgeting: Answers To Review QuestionsMJ YaconPas encore d'évaluation