Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Conflict of Laws - REVIEWERDocument54 pagesConflict of Laws - REVIEWERcherylmoralesnavarro81% (16)

- BUS5111 Written Assignment Unit 3Document7 pagesBUS5111 Written Assignment Unit 3DavePas encore d'évaluation

- Notarial Law PhilippinesDocument18 pagesNotarial Law PhilippinesMegan Mclaughlin100% (2)

- Judicial Affidavit RuleDocument4 pagesJudicial Affidavit RuleCaroline DulayPas encore d'évaluation

- Affidavit of Loss: I, - , of Legal Age, Filipino, Single, and A Resident ofDocument1 pageAffidavit of Loss: I, - , of Legal Age, Filipino, Single, and A Resident ofLindsay MillsPas encore d'évaluation

- !insanity CalendarDocument3 pages!insanity CalendarthenoysePas encore d'évaluation

- Advlegwriting ChecklistDocument20 pagesAdvlegwriting ChecklistMegan MclaughlinPas encore d'évaluation

- Warranty Slip: Salesperson Date Customer Phone Address City State ZIPDocument1 pageWarranty Slip: Salesperson Date Customer Phone Address City State ZIPMegan MclaughlinPas encore d'évaluation

- Digests Law and TechDocument8 pagesDigests Law and TechMegan MclaughlinPas encore d'évaluation

- Evidence Cases 1 ST BatchDocument245 pagesEvidence Cases 1 ST BatchMegan MclaughlinPas encore d'évaluation

- Evid Digest (Jap)Document7 pagesEvid Digest (Jap)Megan MclaughlinPas encore d'évaluation

- Legal Aspects of BusinessDocument33 pagesLegal Aspects of BusinessRaja Gopal100% (1)

- This Study Resource Was: AnswerDocument2 pagesThis Study Resource Was: AnswermerryPas encore d'évaluation

- Heres The Rest of Him-Kent H Steffgen-1968-192pgs-GOVDocument192 pagesHeres The Rest of Him-Kent H Steffgen-1968-192pgs-GOVJeffrey Smith100% (1)

- Module 3 BailmentDocument18 pagesModule 3 BailmentVaibhav GadhveerPas encore d'évaluation

- Request For Proposals: 2017 Lodging Tax FundDocument16 pagesRequest For Proposals: 2017 Lodging Tax FundPratitiPas encore d'évaluation

- IntroductionDocument3 pagesIntroductionMarilou D. BeronioPas encore d'évaluation

- Leasing 1Document41 pagesLeasing 1Aaryan SinghPas encore d'évaluation

- Chapter VI Just CompensationDocument8 pagesChapter VI Just CompensationLawStudent101412Pas encore d'évaluation

- Cusi Vs Domingo (Land Tits)Document2 pagesCusi Vs Domingo (Land Tits)Mary LeandaPas encore d'évaluation

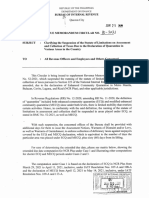

- RMC No. 80-2021Document2 pagesRMC No. 80-2021REX FABERPas encore d'évaluation

- IE235042Document3 pagesIE235042Tani SharmaPas encore d'évaluation

- Agribusiness Management Lesson Plan Library: Unit A: Introduction To AgribusinessDocument6 pagesAgribusiness Management Lesson Plan Library: Unit A: Introduction To AgribusinessHuyen NguyenPas encore d'évaluation

- Accounting Assignment (Group 3)Document5 pagesAccounting Assignment (Group 3)Ayush SatyamPas encore d'évaluation

- Brokers Accreditation AgreementDocument7 pagesBrokers Accreditation AgreementCharmaine CuynoPas encore d'évaluation

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Akhilesh GuptaPas encore d'évaluation

- DTC Agreement Between Cayman Islands and United KingdomDocument13 pagesDTC Agreement Between Cayman Islands and United KingdomOECD: Organisation for Economic Co-operation and DevelopmentPas encore d'évaluation

- Reading 13 International Trade and Capital Flows - AnswersDocument27 pagesReading 13 International Trade and Capital Flows - Answerslucifer morningstarPas encore d'évaluation

- Ingram Micro Malaysia SDN BHD (175932-M)Document10 pagesIngram Micro Malaysia SDN BHD (175932-M)akoolaPas encore d'évaluation

- GR 168557Document1 pageGR 168557Crestu JinPas encore d'évaluation

- Fundamental Cost Concepts: (Part 1)Document29 pagesFundamental Cost Concepts: (Part 1)zahirahsaffriPas encore d'évaluation

- Nike Inc q414 Press Release - 6-25-2014 6pm - CleanDocument9 pagesNike Inc q414 Press Release - 6-25-2014 6pm - CleanmanduramPas encore d'évaluation

- Unity University: Department: CourseDocument5 pagesUnity University: Department: CourseMike Dolla SignPas encore d'évaluation

- Gitanjali Gems Annual Report FY2012-13Document120 pagesGitanjali Gems Annual Report FY2012-13Himanshu JainPas encore d'évaluation

- 480 2019 Expenses Benefits PDFDocument146 pages480 2019 Expenses Benefits PDFmatejkahuPas encore d'évaluation

- OnGuard BrochureoldDocument11 pagesOnGuard Brochureoldmohamed Abo-EwishaPas encore d'évaluation

- Article On Slump SaleDocument3 pagesArticle On Slump SaledafriaPas encore d'évaluation

- Business Studies Notes MR RajabDocument57 pagesBusiness Studies Notes MR RajabsmmaabzPas encore d'évaluation

- 2020 Albany County BudgetDocument378 pages2020 Albany County BudgetDave LucasPas encore d'évaluation

- Demand ForecastingDocument16 pagesDemand ForecastingharithaPas encore d'évaluation