Vous aimerez peut-être aussi

- ABC: Activity-based costingDocument12 pagesABC: Activity-based costingDurga Tripathy DptPas encore d'évaluation

- CMA Viva Prep 190309Document5 pagesCMA Viva Prep 190309Md. Nazmul Huda ShantoPas encore d'évaluation

- Cost Accounting DefinationsDocument7 pagesCost Accounting DefinationsJâmâl HassanPas encore d'évaluation

- Cost Accounting ProjectDocument27 pagesCost Accounting ProjectKishan KudiaPas encore d'évaluation

- MGT Acctg Cost ConceptDocument30 pagesMGT Acctg Cost ConceptApril Pearl VenezuelaPas encore d'évaluation

- Managerial Accounting DefinitionsDocument15 pagesManagerial Accounting Definitionskamal sahabPas encore d'évaluation

- Cost Concepts Product Costs and Period CostsDocument10 pagesCost Concepts Product Costs and Period CostsRain AgrasihPas encore d'évaluation

- Absorption CostingDocument23 pagesAbsorption Costingarman_277276271Pas encore d'évaluation

- Karina-Managerial AccountingDocument13 pagesKarina-Managerial AccountingKarinaPas encore d'évaluation

- Acc 3200 MidtermDocument5 pagesAcc 3200 MidtermCici ZhouPas encore d'évaluation

- Cost Analysis Project ReportDocument6 pagesCost Analysis Project ReportNouman BaigPas encore d'évaluation

- Cost of AccountingDocument9 pagesCost of Accountingnadeemahad98Pas encore d'évaluation

- Cost Terminology and Classification ExplainedDocument8 pagesCost Terminology and Classification ExplainedKanbiro Orkaido100% (1)

- Cost & Management Accounting (ACT 301) : Department: BBA Group: 1Document7 pagesCost & Management Accounting (ACT 301) : Department: BBA Group: 1Mony MstPas encore d'évaluation

- Common Accounting Terminology Glossary Nov 08Document10 pagesCommon Accounting Terminology Glossary Nov 08mbilal1985Pas encore d'évaluation

- Cost Management Accounting April 2021Document10 pagesCost Management Accounting April 2021Nageshwar SinghPas encore d'évaluation

- Marginal Costing and Absorption CostingDocument9 pagesMarginal Costing and Absorption CostingKhushboo AgarwalPas encore d'évaluation

- Marginal Costing and Budgetary ControlDocument5 pagesMarginal Costing and Budgetary ControlThigilpandi07 YTPas encore d'évaluation

- Classification of CostDocument5 pagesClassification of CostCharlotte ChanPas encore d'évaluation

- CostingDocument32 pagesCostingnidhiPas encore d'évaluation

- Unit 1 Lesson 3Document4 pagesUnit 1 Lesson 3avan4052asPas encore d'évaluation

- Cost Accounting - Meaning and ScopeDocument27 pagesCost Accounting - Meaning and ScopemenakaPas encore d'évaluation

- Management Accounting GlossaryDocument10 pagesManagement Accounting GlossaryPooja GuptaPas encore d'évaluation

- Glossary: Absorption CostingDocument11 pagesGlossary: Absorption CostingHome UserPas encore d'évaluation

- MadmDocument9 pagesMadmRuchika SinghPas encore d'évaluation

- Management AccountingDocument87 pagesManagement AccountingYashveer MachraPas encore d'évaluation

- Managerial Accounting - Chapter3Document27 pagesManagerial Accounting - Chapter3Nazia AdeelPas encore d'évaluation

- Accounting 202 Exam 1 Study Guide: Chapter 1: Managerial Accounting and Cost Concepts (12 Questions)Document4 pagesAccounting 202 Exam 1 Study Guide: Chapter 1: Managerial Accounting and Cost Concepts (12 Questions)zoedmolePas encore d'évaluation

- Cost Classification and TerminologyDocument13 pagesCost Classification and TerminologyHussen AbdulkadirPas encore d'évaluation

- Cost AccountingDocument15 pagesCost Accountingesayas goysaPas encore d'évaluation

- 79 52 ET V1 S1 - Unit - 6 PDFDocument19 pages79 52 ET V1 S1 - Unit - 6 PDFTanmay JagetiaPas encore d'évaluation

- Assignment 1 BUSI 3008Document21 pagesAssignment 1 BUSI 3008Irena MatutePas encore d'évaluation

- Marginal and Absorption CostingDocument5 pagesMarginal and Absorption CostingHrutik DeshmukhPas encore d'évaluation

- Module 2 - Introduction To Cost ConceptsDocument51 pagesModule 2 - Introduction To Cost Conceptskaizen4apexPas encore d'évaluation

- Cost Capter FourDocument11 pagesCost Capter FourAbayineh MesenbetPas encore d'évaluation

- Nature and Scope of Cost & Management Accounting: Unit 1Document24 pagesNature and Scope of Cost & Management Accounting: Unit 1umang8808Pas encore d'évaluation

- Absorption CostingDocument76 pagesAbsorption CostingMustafa KamalPas encore d'évaluation

- 11th Sem - Cost ACT 1st NoteDocument5 pages11th Sem - Cost ACT 1st NoteRobin420420Pas encore d'évaluation

- Atp 106 LPM Accounting - Topic 6 - Costing and BudgetingDocument17 pagesAtp 106 LPM Accounting - Topic 6 - Costing and BudgetingTwain JonesPas encore d'évaluation

- Cost Classification and Procedures ReportDocument11 pagesCost Classification and Procedures Reportreyman rosalijosPas encore d'évaluation

- Marginal CostingDocument42 pagesMarginal CostingAbdifatah SaidPas encore d'évaluation

- CostDocument33 pagesCostversmajardoPas encore d'évaluation

- Management AccountingDocument11 pagesManagement AccountingVishnu SharmaPas encore d'évaluation

- cost management allDocument26 pagescost management allranveer78krPas encore d'évaluation

- Management InformationDocument2 pagesManagement InformationRup KothaPas encore d'évaluation

- LEC 02 COST CLASSIFICATION 16032023 115705amDocument19 pagesLEC 02 COST CLASSIFICATION 16032023 115705amZeeshan MajeedPas encore d'évaluation

- A. Detailed Organizational Structure of Finance DepartmentDocument22 pagesA. Detailed Organizational Structure of Finance Departmentk_harlalkaPas encore d'évaluation

- Elements of Cost: Management Accounting Costs Profitability GaapDocument8 pagesElements of Cost: Management Accounting Costs Profitability GaapstefdrocksPas encore d'évaluation

- Introduction To Food CostingDocument17 pagesIntroduction To Food CostingSunil YogiPas encore d'évaluation

- Definition of Cost AccountingDocument11 pagesDefinition of Cost Accountingkenshi ihsnekPas encore d'évaluation

- Costing ConceptsDocument16 pagesCosting ConceptskrimishaPas encore d'évaluation

- Cost ConceptDocument6 pagesCost ConceptDeepti KumariPas encore d'évaluation

- Introduction To Cost Accounting Final With PDFDocument19 pagesIntroduction To Cost Accounting Final With PDFLemon EnvoyPas encore d'évaluation

- Characteristics of Marginal CostingDocument2 pagesCharacteristics of Marginal CostingLJBernardoPas encore d'évaluation

- Marginal CostingDocument14 pagesMarginal CostingVijay DangwaniPas encore d'évaluation

- Cost Ch. IIDocument83 pagesCost Ch. IIMagarsaa AmaanPas encore d'évaluation

- Advanced Cost Accounting and Management Control System: Mekonnen Mengistie (PHD Candidate)Document62 pagesAdvanced Cost Accounting and Management Control System: Mekonnen Mengistie (PHD Candidate)Kalkidan ZerihunPas encore d'évaluation

- Intro To Managerial and Cost Accounting. CostsDocument19 pagesIntro To Managerial and Cost Accounting. Costsmehnaz kPas encore d'évaluation

- Fixed Cost (FC)Document3 pagesFixed Cost (FC)alcuinomarianessajeanPas encore d'évaluation

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageD'EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageÉvaluation : 5 sur 5 étoiles5/5 (1)

- Powerpoint MCQ Bank PDFDocument21 pagesPowerpoint MCQ Bank PDFquickincometips0% (1)

- Powerpoint MCQ Bank PDFDocument21 pagesPowerpoint MCQ Bank PDFquickincometips0% (1)

- Operating Systems MCQ BankDocument21 pagesOperating Systems MCQ BankJamal Hossain Shuvo100% (1)

- CRM Slide Jamal50duDocument18 pagesCRM Slide Jamal50duJamal Hossain ShuvoPas encore d'évaluation

- Bear Call Spread Strategy ExplainedDocument2 pagesBear Call Spread Strategy ExplainedJamal Hossain ShuvoPas encore d'évaluation

- Comparative Short NotesDocument1 pageComparative Short NotesJamal Hossain ShuvoPas encore d'évaluation

- JSC composition suggestionsDocument3 pagesJSC composition suggestionsJamal Hossain ShuvoPas encore d'évaluation

- Main Body Part - CRGDocument24 pagesMain Body Part - CRGJamal Hossain ShuvoPas encore d'évaluation

- 1 Managing-ProjectsDocument9 pages1 Managing-ProjectsJamal Hossain ShuvoPas encore d'évaluation

- Interpersonal CommunicationDocument2 pagesInterpersonal CommunicationJamal Hossain ShuvoPas encore d'évaluation

- Arif's CVDocument3 pagesArif's CVJamal Hossain ShuvoPas encore d'évaluation

- Management Foundations Assessment 2 Business Report 2013Document7 pagesManagement Foundations Assessment 2 Business Report 2013Jamal Hossain ShuvoPas encore d'évaluation

- Bbbaa VivaDocument4 pagesBbbaa VivaJamal Hossain ShuvoPas encore d'évaluation

- Internship Report - CRM (Credit Risk Management) Practice of BASIC Bank Limited, BangladeshDocument67 pagesInternship Report - CRM (Credit Risk Management) Practice of BASIC Bank Limited, BangladeshJamal Hossain Shuvo100% (2)

- Ent MGT Assignment 1 Detailed GuidelineDocument2 pagesEnt MGT Assignment 1 Detailed GuidelineJamal Hossain ShuvoPas encore d'évaluation

- Essay Mid-Semester Exam - 6 August 2013Document2 pagesEssay Mid-Semester Exam - 6 August 2013Jamal Hossain ShuvoPas encore d'évaluation

- AuditDocument3 pagesAuditJamal Hossain ShuvoPas encore d'évaluation

- Islamic BankingDocument1 pageIslamic BankingJamal Hossain ShuvoPas encore d'évaluation

- Shantii Marketing AssignmentDocument4 pagesShantii Marketing AssignmentJamal Hossain ShuvoPas encore d'évaluation

- Assessment 2 International Marketing StrategyDocument4 pagesAssessment 2 International Marketing StrategyJamal Hossain ShuvoPas encore d'évaluation

- CV of Jamal HossainDocument2 pagesCV of Jamal HossainJamal Hossain ShuvoPas encore d'évaluation

- Statistics Term Paper FINALDocument60 pagesStatistics Term Paper FINALJamal Hossain ShuvoPas encore d'évaluation

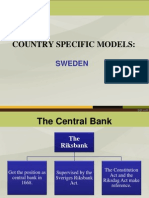

- SWEDEN'S CENTRAL BANK AND PARLIAMENTARY OVERSIGHTDocument8 pagesSWEDEN'S CENTRAL BANK AND PARLIAMENTARY OVERSIGHTJamal Hossain ShuvoPas encore d'évaluation

- Ethics Case Study ADocument2 pagesEthics Case Study AJamal Hossain ShuvoPas encore d'évaluation

- Assessment 1 International Marketing StrategyDocument2 pagesAssessment 1 International Marketing StrategyJamal Hossain ShuvoPas encore d'évaluation

- AuditDocument3 pagesAuditJamal Hossain ShuvoPas encore d'évaluation

- Investment BankingDocument3 pagesInvestment BankingJamal Hossain ShuvoPas encore d'évaluation

- Step10 PlagiarismDocument15 pagesStep10 PlagiarismJamal Hossain Shuvo100% (1)

- Audit FinalDocument4 pagesAudit FinalJamal Hossain ShuvoPas encore d'évaluation

- HRMDocument5 pagesHRMJamal Hossain ShuvoPas encore d'évaluation

- De So 2 de Kiem Tra Giua Ki 2 Tieng Anh 8 Moi 1677641450Document4 pagesDe So 2 de Kiem Tra Giua Ki 2 Tieng Anh 8 Moi 1677641450phuong phamthihongPas encore d'évaluation

- Arpia Lovely Rose Quiz - Chapter 6 - Joint Arrangements - 2020 EditionDocument4 pagesArpia Lovely Rose Quiz - Chapter 6 - Joint Arrangements - 2020 EditionLovely ArpiaPas encore d'évaluation

- Notes Socialism in Europe and RussianDocument11 pagesNotes Socialism in Europe and RussianAyaan ImamPas encore d'évaluation

- The Five Laws of Light - Suburban ArrowsDocument206 pagesThe Five Laws of Light - Suburban Arrowsjorge_calvo_20Pas encore d'évaluation

- Supply Chain AssignmentDocument29 pagesSupply Chain AssignmentHisham JackPas encore d'évaluation

- The Future of Indian Economy Past Reforms and Challenges AheadDocument281 pagesThe Future of Indian Economy Past Reforms and Challenges AheadANJALIPas encore d'évaluation

- AVK Butterfly Valves Centric 75 - TADocument1 pageAVK Butterfly Valves Centric 75 - TANam Nguyễn ĐứcPas encore d'évaluation

- ms3 Seq 01 Expressing Interests With Adverbs of FrequencyDocument3 pagesms3 Seq 01 Expressing Interests With Adverbs of Frequencyg27rimaPas encore d'évaluation

- P.E 4 Midterm Exam 2 9Document5 pagesP.E 4 Midterm Exam 2 9Xena IngalPas encore d'évaluation

- Arx Occasional Papers - Hospitaller Gunpowder MagazinesDocument76 pagesArx Occasional Papers - Hospitaller Gunpowder MagazinesJohn Spiteri GingellPas encore d'évaluation

- AVX EnglishDocument70 pagesAVX EnglishLeo TalisayPas encore d'évaluation

- Battery Genset Usage 06-08pelj0910Document4 pagesBattery Genset Usage 06-08pelj0910b400013Pas encore d'évaluation

- CP ON PUD (1) ADocument20 pagesCP ON PUD (1) ADeekshitha DanthuluriPas encore d'évaluation

- 11th AccountancyDocument13 pages11th AccountancyNarendar KumarPas encore d'évaluation

- 2010 Economics Syllabus For SHSDocument133 pages2010 Economics Syllabus For SHSfrimpongbenardghPas encore d'évaluation

- Introduction to History Part 1: Key ConceptsDocument32 pagesIntroduction to History Part 1: Key ConceptsMaryam14xPas encore d'évaluation

- Red Orchid - Best PracticesDocument80 pagesRed Orchid - Best PracticeslabiaernestoPas encore d'évaluation

- February / March 2010Document16 pagesFebruary / March 2010Instrulife OostkampPas encore d'évaluation

- Equity Valuation Concepts and Basic Tools (CFA) CH 10Document28 pagesEquity Valuation Concepts and Basic Tools (CFA) CH 10nadeem.aftab1177Pas encore d'évaluation

- Jesus' Death on the Cross Explored Through Theological ModelsDocument13 pagesJesus' Death on the Cross Explored Through Theological ModelsKhristian Joshua G. JuradoPas encore d'évaluation

- Classification of Boreal Forest Ecosystem Goods and Services in FinlandDocument197 pagesClassification of Boreal Forest Ecosystem Goods and Services in FinlandSivamani SelvarajuPas encore d'évaluation

- Codilla Vs MartinezDocument3 pagesCodilla Vs MartinezMaria Recheille Banac KinazoPas encore d'évaluation

- Speech Writing MarkedDocument3 pagesSpeech Writing MarkedAshley KyawPas encore d'évaluation

- Purposive Communication Module 1Document18 pagesPurposive Communication Module 1daphne pejo100% (4)

- Device Exp 2 Student ManualDocument4 pagesDevice Exp 2 Student Manualgg ezPas encore d'évaluation

- Activity 1 DIASSDocument3 pagesActivity 1 DIASSLJ FamatiganPas encore d'évaluation

- Full Discography List at Wrathem (Dot) ComDocument38 pagesFull Discography List at Wrathem (Dot) ComwrathemPas encore d'évaluation

- MW Scenario Handbook V 12 ADocument121 pagesMW Scenario Handbook V 12 AWilliam HamiltonPas encore d'évaluation

- Adic PDFDocument25 pagesAdic PDFDejan DeksPas encore d'évaluation

- Overlord Volume 1 - The Undead King Black EditionDocument291 pagesOverlord Volume 1 - The Undead King Black EditionSaadAmir100% (11)