Vous aimerez peut-être aussi

- A Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank, Vennikulam Branch (Kerala)Document71 pagesA Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank, Vennikulam Branch (Kerala)Lini Susan John100% (4)

- Banking Module 1Document26 pagesBanking Module 1mansisharma8301Pas encore d'évaluation

- Retail Banking JUNE 2022Document10 pagesRetail Banking JUNE 2022Rajni KumariPas encore d'évaluation

- Shyamala Gopinath: Retail Banking - Opportunities and ChallengesDocument5 pagesShyamala Gopinath: Retail Banking - Opportunities and ChallengesAmol ShindePas encore d'évaluation

- Retail BankingDocument15 pagesRetail BankingjazzrulzPas encore d'évaluation

- Retail BankingDocument10 pagesRetail BankingAtul MadPas encore d'évaluation

- ChapterDocument16 pagesChapterAjay YadavPas encore d'évaluation

- Retail Lending Business Importance & Strategies For Maintaining GrowthDocument21 pagesRetail Lending Business Importance & Strategies For Maintaining Growthjpradnya4451Pas encore d'évaluation

- Retail BakingDocument29 pagesRetail BakingdarshpujPas encore d'évaluation

- Banking Retail ProductsDocument7 pagesBanking Retail ProductsaadisssPas encore d'évaluation

- Synopsis 1Document16 pagesSynopsis 1Vipul GuptaPas encore d'évaluation

- Indian Retail Banking Industry: Drivers & Dooms - An Empirical StudyDocument16 pagesIndian Retail Banking Industry: Drivers & Dooms - An Empirical StudyApoorva PandeyPas encore d'évaluation

- Challenges To Retail Banking in IndiaDocument2 pagesChallenges To Retail Banking in IndiapadmajammulaPas encore d'évaluation

- Retail Banking in IndiaDocument17 pagesRetail Banking in Indianitinsuba198050% (2)

- Impact of Retail Banking in Indian Economy: Research Article Parmanand Barodiya and Anita Singh ChauhanDocument5 pagesImpact of Retail Banking in Indian Economy: Research Article Parmanand Barodiya and Anita Singh ChauhanthPas encore d'évaluation

- Akshu Full ProjectDocument73 pagesAkshu Full ProjectAshwini VenugopalPas encore d'évaluation

- Retail Banking - A Real Growing Concept in The Present Scenario Dr.A.SelvarajDocument8 pagesRetail Banking - A Real Growing Concept in The Present Scenario Dr.A.Selvarajrajeshraj0112Pas encore d'évaluation

- Project On Retail BankingDocument44 pagesProject On Retail BankingabhinaykasarePas encore d'évaluation

- Dissertation Project IqbalDocument85 pagesDissertation Project Iqbalsunnychauhan89Pas encore d'évaluation

- Introduction To Topic Meaning of Retail BankingDocument8 pagesIntroduction To Topic Meaning of Retail Bankingpriyanka guptaPas encore d'évaluation

- Full)Document60 pagesFull)Neeraj BhatiPas encore d'évaluation

- Chapter - 1Document8 pagesChapter - 1rajkumariPas encore d'évaluation

- A Study On Contemporary Challenges and Opportunities of Retail Banking in IndiaDocument12 pagesA Study On Contemporary Challenges and Opportunities of Retail Banking in IndiakokoPas encore d'évaluation

- Banking IndustryDocument30 pagesBanking IndustrySagar Damani100% (1)

- Page 11-37Document28 pagesPage 11-37Preeti MishraPas encore d'évaluation

- BANKING INDUSTRY-Fundamental AnalysisDocument19 pagesBANKING INDUSTRY-Fundamental AnalysisGopi Krishnan.nPas encore d'évaluation

- BANKING INDUSTRY-Fundamental AnalysisDocument19 pagesBANKING INDUSTRY-Fundamental AnalysisGopi Krishnan.nPas encore d'évaluation

- Name: Jay Ketanbhai Changela Enrollment No.: 20fomba11508 For The Submission Of: SeeDocument26 pagesName: Jay Ketanbhai Changela Enrollment No.: 20fomba11508 For The Submission Of: SeeMAANPas encore d'évaluation

- 2.0 Introduction To Retail Banking: The Retail Banking Environment Today Is Changing Fast. The ChangingDocument45 pages2.0 Introduction To Retail Banking: The Retail Banking Environment Today Is Changing Fast. The ChangingViraat Ashok SudPas encore d'évaluation

- Retail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudyDocument9 pagesRetail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudySandeep KumarPas encore d'évaluation

- Finance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)Document40 pagesFinance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)AneesAnsariPas encore d'évaluation

- Kotak FinalDocument46 pagesKotak FinalRahul FaliyaPas encore d'évaluation

- Retail Banking Front Office Management ActivityDocument66 pagesRetail Banking Front Office Management ActivitysargunkaurPas encore d'évaluation

- A Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank Vennikulam Branch KeralaDocument71 pagesA Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank Vennikulam Branch KeralaRajasekaranPas encore d'évaluation

- Comm ReportDocument5 pagesComm ReportvarunsalwanPas encore d'évaluation

- Retail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To StudentDocument51 pagesRetail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To Studentganeshkhale7052Pas encore d'évaluation

- Banking ProjectDocument35 pagesBanking Projectvarun_varunsharmaPas encore d'évaluation

- International Journal of Information Technology and Knowledge ManagementDocument6 pagesInternational Journal of Information Technology and Knowledge Managementrakeshkmr1186Pas encore d'évaluation

- Study On Retail BankingDocument47 pagesStudy On Retail Bankingzaru1121Pas encore d'évaluation

- Challenges and Opportunities To Commercial Banks in RuralDocument16 pagesChallenges and Opportunities To Commercial Banks in RuralRaghav guptaPas encore d'évaluation

- Ancillary Services Provided by BankersDocument17 pagesAncillary Services Provided by BankersLogan Davis100% (2)

- The Indian Kaleidoscope: Emerging Trends in RetailDocument52 pagesThe Indian Kaleidoscope: Emerging Trends in RetailSwati Agarwal100% (1)

- Retail Fs MarketDocument6 pagesRetail Fs MarketAvikalmmPas encore d'évaluation

- Retail Banking at HDFCDocument56 pagesRetail Banking at HDFCutkarsh jaiswalPas encore d'évaluation

- I. Overall Market Size: Question-4Document4 pagesI. Overall Market Size: Question-4Himanshu ShuklaPas encore d'évaluation

- 10 Nishith Devraj Paper For Jbfsir 1 PDFDocument10 pages10 Nishith Devraj Paper For Jbfsir 1 PDFpareek gopalPas encore d'évaluation

- Yes Bank Mainstreaming Development Into Indian BankingDocument20 pagesYes Bank Mainstreaming Development Into Indian Bankinggauarv_singh13Pas encore d'évaluation

- Synopsis Cannra BankDocument3 pagesSynopsis Cannra BankGagan KauraPas encore d'évaluation

- Sector Project 1Document5 pagesSector Project 12k20dmba102 RiyaGoelPas encore d'évaluation

- Credit Score EssayDocument24 pagesCredit Score EssaypavistatsPas encore d'évaluation

- 2.10 Retail BankingDocument14 pages2.10 Retail BankingSrinivas RaoPas encore d'évaluation

- Meaning of Retail: Banking Regulation Act 1949Document22 pagesMeaning of Retail: Banking Regulation Act 1949chinu1303Pas encore d'évaluation

- Banking Sector: 1.1 Introduction To The TaskDocument23 pagesBanking Sector: 1.1 Introduction To The TaskRIYA CHALKEPas encore d'évaluation

- Industry Profile: Excellence in Indian Banking', India's Gross Domestic Product (GDP) Growth Will Make TheDocument27 pagesIndustry Profile: Excellence in Indian Banking', India's Gross Domestic Product (GDP) Growth Will Make TheNekta PinchaPas encore d'évaluation

- Banking India: Accepting Deposits for the Purpose of LendingD'EverandBanking India: Accepting Deposits for the Purpose of LendingPas encore d'évaluation

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)D'EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Pas encore d'évaluation

- JAIIB Legal Sample Questions by MuruganDocument63 pagesJAIIB Legal Sample Questions by MuruganRizz Ahammad80% (5)

- Hand Book On Know Your Circular Andhra Bank PromotionDocument81 pagesHand Book On Know Your Circular Andhra Bank PromotionSubrat Satyaranjan KanungoPas encore d'évaluation

- Monetary Policy and CB Module-7Document18 pagesMonetary Policy and CB Module-7Eleine Taroma AlvarezPas encore d'évaluation

- Libra To Vashu TradingDocument1 pageLibra To Vashu TradingLL Lawwise Consultech India Pvt LtdPas encore d'évaluation

- Incoming Payment InstructionDocument2 pagesIncoming Payment InstructionCapitol COPas encore d'évaluation

- The Roman Eagle On A Red ShieldDocument2 pagesThe Roman Eagle On A Red ShieldARBITRAJ COMERCIAL -Mircea Halaciuga,Esq. aka. Mike SerbanPas encore d'évaluation

- Contract Account FormatDocument3 pagesContract Account FormatVishakh Nag100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument21 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancemani kantaPas encore d'évaluation

- List of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameDocument102 pagesList of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameSusanPas encore d'évaluation

- Deposit Mobilization of Nabil Bank LimitedDocument41 pagesDeposit Mobilization of Nabil Bank Limitedram binod yadav76% (38)

- Classroom Exercises On Receivables AnswersDocument4 pagesClassroom Exercises On Receivables AnswersJohn Cedfrey Narne100% (1)

- Proc No. 129-155 dt.14.12.2018Document7 pagesProc No. 129-155 dt.14.12.2018Maku RajkumarPas encore d'évaluation

- Moi Chapter I Simple InterestDocument17 pagesMoi Chapter I Simple InterestBadtuan Asliya E.Pas encore d'évaluation

- Banking System of India: Presented By-Sohini MukherjeeDocument31 pagesBanking System of India: Presented By-Sohini MukherjeeShivam AgarwalITF43Pas encore d'évaluation

- Total: Tax Invoice For..Document10 pagesTotal: Tax Invoice For..Sarun SunnyPas encore d'évaluation

- Coldwell Banker Home Buyer's GuidebookDocument25 pagesColdwell Banker Home Buyer's GuidebookLani Rosales100% (2)

- Chanda KochharDocument39 pagesChanda KochharviveknayeePas encore d'évaluation

- Accounting For Musyarakah FinancingDocument16 pagesAccounting For Musyarakah FinancingHadyan AntoroPas encore d'évaluation

- Samudra Milk Bill 01.04.19 To 10.04.19Document102 pagesSamudra Milk Bill 01.04.19 To 10.04.19SanjayVermaPas encore d'évaluation

- FIN435 Asgmnt UpdatedDocument10 pagesFIN435 Asgmnt UpdatedNazirah Mohamed KauziPas encore d'évaluation

- Split 162013 190909 - 20220331Document5 pagesSplit 162013 190909 - 20220331NUR FASIHAH BINTIPas encore d'évaluation

- Amtb Eft Format SpaDocument7 pagesAmtb Eft Format SpaDavid GómezPas encore d'évaluation

- Statement EUDocument41 pagesStatement EUuyên đỗPas encore d'évaluation

- Quiz On Audit of CashDocument11 pagesQuiz On Audit of CashY JPas encore d'évaluation

- OpTransactionHistoryTpr09 04 2019 PDFDocument9 pagesOpTransactionHistoryTpr09 04 2019 PDFSAMEER AHMADPas encore d'évaluation

- A Study On Customer Prefernces Towards Credit Cards in HDFC BankDocument40 pagesA Study On Customer Prefernces Towards Credit Cards in HDFC BankSharathPas encore d'évaluation

- Fees Structure For Kabojja International SchoolDocument2 pagesFees Structure For Kabojja International SchoolTheCampusTimes100% (1)

- IBPS (Institute of Banking and Personal Selection)Document3 pagesIBPS (Institute of Banking and Personal Selection)Nikhil KumarPas encore d'évaluation

- Chapter 1 - Financial System in NepalDocument9 pagesChapter 1 - Financial System in NepalMukul Bhatia67% (6)

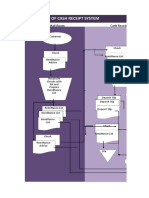

- Flowchart of Cash Receipt System: Mail Room Cash ReceiptsDocument17 pagesFlowchart of Cash Receipt System: Mail Room Cash ReceiptsStephanie Diane SabadoPas encore d'évaluation