Vous aimerez peut-être aussi

- Operations On Vectors and MatricesDocument19 pagesOperations On Vectors and MatricessamiseechPas encore d'évaluation

- Linear Algebra Assignment MathematicsDocument20 pagesLinear Algebra Assignment MathematicssamiseechPas encore d'évaluation

- Edu 2012 04 MLC ExamDocument30 pagesEdu 2012 04 MLC ExamsamiseechPas encore d'évaluation

- Accounts AssignmentDocument7 pagesAccounts AssignmentsamiseechPas encore d'évaluation

- Conducting Scientific ResearchDocument15 pagesConducting Scientific ResearchsamiseechPas encore d'évaluation

- Operations On Vectors and MatricesDocument19 pagesOperations On Vectors and MatricessamiseechPas encore d'évaluation

- Home Work SolutionsDocument3 pagesHome Work SolutionssamiseechPas encore d'évaluation

- Human Rights CouncilDocument10 pagesHuman Rights CouncilsamiseechPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 4.2 Shell Oil Workers' Union Vs Shell CompanyDocument2 pages4.2 Shell Oil Workers' Union Vs Shell CompanyHiroshi AdrianoPas encore d'évaluation

- Stay Hungry - Steve Job (Apple)Document21 pagesStay Hungry - Steve Job (Apple)Joe XavierPas encore d'évaluation

- CSR in Banking Sector: International Journal of Economics, Commerce and ManagementDocument22 pagesCSR in Banking Sector: International Journal of Economics, Commerce and ManagementmustafaPas encore d'évaluation

- Guide To Composition of Safety CommitteeDocument2 pagesGuide To Composition of Safety CommitteeDexter Abrenica AlfonsoPas encore d'évaluation

- Hult Prize 2019 ChallengeDocument24 pagesHult Prize 2019 ChallengeManar HosnyPas encore d'évaluation

- What Is Internal RecruitmentDocument2 pagesWhat Is Internal RecruitmentTanvir FuadPas encore d'évaluation

- Himachal Pradesh Staff Selection Commission Hamirpur Distt. HAMIRPUR (H.P.) - 177001Document26 pagesHimachal Pradesh Staff Selection Commission Hamirpur Distt. HAMIRPUR (H.P.) - 177001Known 6192Pas encore d'évaluation

- Ankrah Vol.5 PDFDocument10 pagesAnkrah Vol.5 PDFWahyu Kurniawan AjiPas encore d'évaluation

- Labor Economics 7Th Edition George Borjas Solutions Manual Full Chapter PDFDocument34 pagesLabor Economics 7Th Edition George Borjas Solutions Manual Full Chapter PDFphualexandrad3992% (12)

- Case Study AnalysisDocument10 pagesCase Study AnalysisRupali Pratap SinghPas encore d'évaluation

- Revised Press Release - Mphasis Transfers Significant Portion of Its Domestic India Business To Hinduja Global Solutions (Company Update)Document1 pageRevised Press Release - Mphasis Transfers Significant Portion of Its Domestic India Business To Hinduja Global Solutions (Company Update)Shyam SunderPas encore d'évaluation

- LM A1.1Document17 pagesLM A1.1Dat HoangPas encore d'évaluation

- Exit InterviewDocument3 pagesExit InterviewAugustya DuttaPas encore d'évaluation

- Doctrine of Piercing The Corporate Veil - Case DigestDocument2 pagesDoctrine of Piercing The Corporate Veil - Case DigestlookalikenilongPas encore d'évaluation

- Advisory Board Membership AgreementDocument5 pagesAdvisory Board Membership Agreementbforemny100% (2)

- 38 - Suico v. NLRC, January 30, 2007Document2 pages38 - Suico v. NLRC, January 30, 2007Christine ValidoPas encore d'évaluation

- Fin e 327 2019Document4 pagesFin e 327 2019Gunalan GunaPas encore d'évaluation

- FlashcardsDocument5 pagesFlashcardsNitin ParasPas encore d'évaluation

- Maersk Vs RamosDocument3 pagesMaersk Vs RamosSheryl Ogoc100% (1)

- Contract For Tutor Services For Website VersionDocument5 pagesContract For Tutor Services For Website VersiongigiPas encore d'évaluation

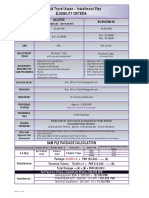

- Labbaik Travel Asaan - Installment Plan Eligibility CriteriaDocument1 pageLabbaik Travel Asaan - Installment Plan Eligibility CriteriamuhammadTzPas encore d'évaluation

- Big Data and Data EthicsDocument153 pagesBig Data and Data Ethicsvishal_pup0% (1)

- Caste System in IndiaDocument13 pagesCaste System in Indiazeeshanahmad1110% (1)

- The Trade Unions Act, 1926Document37 pagesThe Trade Unions Act, 1926Huzaifa SalimPas encore d'évaluation

- SPRP PPT Farah Aisyah - Sesi 15Document27 pagesSPRP PPT Farah Aisyah - Sesi 15elearninglsprPas encore d'évaluation

- Cost of Goods SoldDocument14 pagesCost of Goods Soldmuhammad irfan50% (2)

- H.R Policies & Strategies in Reliance CommunicationsDocument122 pagesH.R Policies & Strategies in Reliance CommunicationsNazma MirzaPas encore d'évaluation

- PagesDocument82 pagesPagesEslam EltaweelPas encore d'évaluation

- LA TONDEÑA WORKERS UNION Vs Sec of LAborDocument2 pagesLA TONDEÑA WORKERS UNION Vs Sec of LAborJessy FrancisPas encore d'évaluation

- Barangay Ordinance Number 1 Series of 2019 PWD DeskDocument4 pagesBarangay Ordinance Number 1 Series of 2019 PWD DeskArniel Fred Tormis Fernandez100% (2)