Vous aimerez peut-être aussi

- Tower Hamlets Council's Saturation Zone Proposal For Brick LaneDocument24 pagesTower Hamlets Council's Saturation Zone Proposal For Brick LaneMike PollittPas encore d'évaluation

- AEF's Evidence On Airport CapacityDocument14 pagesAEF's Evidence On Airport CapacityMike PollittPas encore d'évaluation

- Darren Johnson AM: 10 Myths Housing Benefit Sept 2012Document3 pagesDarren Johnson AM: 10 Myths Housing Benefit Sept 2012Mike PollittPas encore d'évaluation

- English Heritage's London List 2011Document52 pagesEnglish Heritage's London List 2011Mike PollittPas encore d'évaluation

- Clapton Park Estate MapDocument1 pageClapton Park Estate MapMike PollittPas encore d'évaluation

- Notting Hill Carnival Map From The Met PoliceDocument2 pagesNotting Hill Carnival Map From The Met PoliceMike PollittPas encore d'évaluation

- Urban Foxes LeafletDocument18 pagesUrban Foxes LeafletMike PollittPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- CIT V Tulip Proceedings in The Income Tax TribunalDocument34 pagesCIT V Tulip Proceedings in The Income Tax TribunalCA Pallavi KPas encore d'évaluation

- Prospects of Economic Cooperation in The Bangladesh, China, India and Myanmar Region: A Quantitative AssessmentDocument42 pagesProspects of Economic Cooperation in The Bangladesh, China, India and Myanmar Region: A Quantitative AssessmentTariqur Rahman ChanchalPas encore d'évaluation

- Sanco Annual Report 2019Document187 pagesSanco Annual Report 2019Sonu KumariPas encore d'évaluation

- Case StudyDocument2 pagesCase StudyApril Joy Sumagit HidalgoPas encore d'évaluation

- National Mineral Policy-2008Document36 pagesNational Mineral Policy-2008Bharath Kumar GoudPas encore d'évaluation

- Adjudication Order against Shri. Bhanwarlal H Ranka, Shri. Pradeep B Ranka, Ms. Kusum B Ranka, Ms. Sangeetha P Ranka, Ms. Anjana B Ranka, Shri. Arun B Ranka , Ms. Rachana A Ranka and Shri. Kantilal G Bafna in the matter of Residency Projects and Infratech Ltd.Document8 pagesAdjudication Order against Shri. Bhanwarlal H Ranka, Shri. Pradeep B Ranka, Ms. Kusum B Ranka, Ms. Sangeetha P Ranka, Ms. Anjana B Ranka, Shri. Arun B Ranka , Ms. Rachana A Ranka and Shri. Kantilal G Bafna in the matter of Residency Projects and Infratech Ltd.Shyam SunderPas encore d'évaluation

- Goh Cheng Poh ProfilesDocument5 pagesGoh Cheng Poh ProfilesGoh Cheng PohPas encore d'évaluation

- NR 37 19 Saramacca First Ore en - SurinameDocument1 pageNR 37 19 Saramacca First Ore en - SurinameSuriname MirrorPas encore d'évaluation

- R.132.9 Westmont vs. Francia PDFDocument17 pagesR.132.9 Westmont vs. Francia PDFMark Gabriel B. MarangaPas encore d'évaluation

- FIN3130 Exam SolutionsDocument9 pagesFIN3130 Exam SolutionsSimbarashe MupfupiPas encore d'évaluation

- Digital BankingDocument3 pagesDigital BankingDPC GymPas encore d'évaluation

- ITIL At-A-Glance v1.1 PDFDocument7 pagesITIL At-A-Glance v1.1 PDFhowelaiPas encore d'évaluation

- From To: RealityDocument96 pagesFrom To: RealityAw Yuong TuckPas encore d'évaluation

- Annual Report 2016-17 of MSEB CPF TrustDocument21 pagesAnnual Report 2016-17 of MSEB CPF TrustAbhishek MusaddiPas encore d'évaluation

- Corporate Governance CIA 3 Group 4Document13 pagesCorporate Governance CIA 3 Group 4Sunny PatelPas encore d'évaluation

- Transforming Darden RestaurantsDocument294 pagesTransforming Darden RestaurantsArun KumarPas encore d'évaluation

- Financial MathematicsDocument5 pagesFinancial MathematicsTAFARA MAROZVAPas encore d'évaluation

- RUSSIA 2010 & What It Means For The WorldDocument348 pagesRUSSIA 2010 & What It Means For The WorldElder FutharkPas encore d'évaluation

- DCR 58 Mill LandDocument6 pagesDCR 58 Mill LandojasmodyPas encore d'évaluation

- UTI Comman Appl. Form Equity & BalanceDocument2 pagesUTI Comman Appl. Form Equity & Balancedrashti.investments1614Pas encore d'évaluation

- FTSE4Good All-World IndexDocument4 pagesFTSE4Good All-World Indexdjfoo000Pas encore d'évaluation

- Determinants of Lending Behaviour of Commercial BanksDocument3 pagesDeterminants of Lending Behaviour of Commercial BanksMichelle MilanesPas encore d'évaluation

- JSW Steel LTD.: Key Stock IndicatorsDocument8 pagesJSW Steel LTD.: Key Stock IndicatorsAmit KumarPas encore d'évaluation

- Micro InsuranceDocument13 pagesMicro InsuranceLanang TanuPas encore d'évaluation

- LBC Express Holdings' Financial AnalysisDocument9 pagesLBC Express Holdings' Financial AnalysisJerry ManatadPas encore d'évaluation

- 1 Assignment-1-O.mDocument2 pages1 Assignment-1-O.mshannel jacksonPas encore d'évaluation

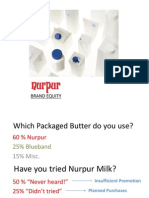

- Nurpur Brand EquityDocument19 pagesNurpur Brand EquityBilal100% (2)

- Research Title: Challengs and Prospects of Private Business Investment (In Case of Arbaminch Town)Document5 pagesResearch Title: Challengs and Prospects of Private Business Investment (In Case of Arbaminch Town)Mebratu MazePas encore d'évaluation

- 4.cash Flow Statement (CFS)Document16 pages4.cash Flow Statement (CFS)Efrelyn Grethel Baraya AlejandroPas encore d'évaluation

- Sample SOW - Security ServicesDocument14 pagesSample SOW - Security ServicesLongLacHong100% (1)