Vous aimerez peut-être aussi

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionD'EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionPas encore d'évaluation

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionD'EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionPas encore d'évaluation

- 438Document6 pages438Rehan AshrafPas encore d'évaluation

- 106 1648004706 PDFDocument15 pages106 1648004706 PDFMohd AmanullahPas encore d'évaluation

- Financial Accounting Question SetDocument24 pagesFinancial Accounting Question SetAlireza KafaeiPas encore d'évaluation

- Bcom TaxDocument6 pagesBcom TaxAditya .cPas encore d'évaluation

- AFA IP.l II QuestionDec 2019Document4 pagesAFA IP.l II QuestionDec 2019HossainPas encore d'évaluation

- Tax Accounting Set ADocument4 pagesTax Accounting Set AGopti EmmanuelPas encore d'évaluation

- Question-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamDocument4 pagesQuestion-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamMuhammad ArslanPas encore d'évaluation

- Chapter 49-Pfrs For SmesDocument6 pagesChapter 49-Pfrs For SmesEmma Mariz Garcia40% (5)

- TX Zwe Examiner's Report June 2022Document10 pagesTX Zwe Examiner's Report June 2022Sean ChigagaPas encore d'évaluation

- Test Papers: FoundationDocument23 pagesTest Papers: FoundationUmesh TurankarPas encore d'évaluation

- Principles of Taxation ND2020Document2 pagesPrinciples of Taxation ND2020Sharif MahmudPas encore d'évaluation

- Mock Sep 2023 - Question PaperDocument8 pagesMock Sep 2023 - Question Paperfahadkhn871Pas encore d'évaluation

- Advanced Tax Laws and PracticeDocument8 pagesAdvanced Tax Laws and PracticenikhilPas encore d'évaluation

- Rise Tax Mock QP With SolutionDocument18 pagesRise Tax Mock QP With SolutionEmperor YasuoPas encore d'évaluation

- Anfin208 Mid Term AssignmentDocument6 pagesAnfin208 Mid Term Assignmentprince matamboPas encore d'évaluation

- Application Level Corporate Laws Practices Nov Dec 2013Document3 pagesApplication Level Corporate Laws Practices Nov Dec 2013Timothy GillespiePas encore d'évaluation

- Income Tax Assessment and Procedure - 1Document3 pagesIncome Tax Assessment and Procedure - 1amaljacobjogilinkedinPas encore d'évaluation

- Division B - Descriptive Questions Question No. 1 Is CompulsoryDocument5 pagesDivision B - Descriptive Questions Question No. 1 Is CompulsoryUrvashi RPas encore d'évaluation

- Pe III Taxation II May Jun 2010Document3 pagesPe III Taxation II May Jun 2010swarna dasPas encore d'évaluation

- Q&A, November 2023Document9 pagesQ&A, November 2023Cerealis FelicianPas encore d'évaluation

- Afa 1 Icmab QuestionsDocument65 pagesAfa 1 Icmab QuestionsKamrul HassanPas encore d'évaluation

- 10 2005 Dec QDocument6 pages10 2005 Dec Qspinster40% (1)

- S3 3-TaxationDocument12 pagesS3 3-TaxationMartin NzamutumaPas encore d'évaluation

- Tax Laws: NOTE: All References To Sections Mentioned in Part-A of The Question Paper Relate To TheDocument8 pagesTax Laws: NOTE: All References To Sections Mentioned in Part-A of The Question Paper Relate To ThePriya MalhotraPas encore d'évaluation

- CFM 100-Introduction To Taxation DAYDocument4 pagesCFM 100-Introduction To Taxation DAYDan StephenPas encore d'évaluation

- Advanced Corporate AccountingDocument6 pagesAdvanced Corporate Accountingamensinkai3133Pas encore d'évaluation

- ACT 2100 Worksheet IIIDocument4 pagesACT 2100 Worksheet IIIAshmini PershadPas encore d'évaluation

- IMT 57 Financial Accounting M1Document4 pagesIMT 57 Financial Accounting M1solvedcarePas encore d'évaluation

- CA School of Accountancy's Mock Exam: PAPER: Financial Accounting (FA) TUTOR: Roshan BhujelDocument18 pagesCA School of Accountancy's Mock Exam: PAPER: Financial Accounting (FA) TUTOR: Roshan BhujelMan Ish K DasPas encore d'évaluation

- Taxation-Ii: (A) What Do You Mean by "Arm's Length Price" and What Are The Methods To Be Used For TheDocument4 pagesTaxation-Ii: (A) What Do You Mean by "Arm's Length Price" and What Are The Methods To Be Used For Theswarna dasPas encore d'évaluation

- Book-Keeping and Accounts/Series-3-2004 (Code2006)Document16 pagesBook-Keeping and Accounts/Series-3-2004 (Code2006)Hein Linn Kyaw100% (1)

- F3 Specimen Exam 2014 PDFDocument21 pagesF3 Specimen Exam 2014 PDFgrrrklPas encore d'évaluation

- f3 Specimen j14 PDFDocument21 pagesf3 Specimen j14 PDFBestPas encore d'évaluation

- (April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Document3 pages(April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Bhuvaneswari karuturiPas encore d'évaluation

- KL Taxtaion I May June 2012Document2 pagesKL Taxtaion I May June 2012asdfghjkl007Pas encore d'évaluation

- Requirements:: Taxation-Ii Time Allowed - 3 Hours Total Marks - 100Document5 pagesRequirements:: Taxation-Ii Time Allowed - 3 Hours Total Marks - 100Srikrishna DharPas encore d'évaluation

- Tax Question Bank 2020Document37 pagesTax Question Bank 2020Tawanda Tatenda HerbertPas encore d'évaluation

- Account - 2Document6 pagesAccount - 2kakajumaPas encore d'évaluation

- FINANCIAL ACCOUNTING I 2019 MinDocument6 pagesFINANCIAL ACCOUNTING I 2019 MinKedarPas encore d'évaluation

- Taxtion II Nov Dec 2014Document5 pagesTaxtion II Nov Dec 2014Md HasanPas encore d'évaluation

- MF0012Document3 pagesMF0012Rajesh SinghPas encore d'évaluation

- QuickBooks For BeginnersDocument9 pagesQuickBooks For BeginnersZain U DdinPas encore d'évaluation

- Acct 2005 Practice Exam 2Document17 pagesAcct 2005 Practice Exam 2laujenny64Pas encore d'évaluation

- Financial Accounting Atc 1Document3 pagesFinancial Accounting Atc 1hshing02Pas encore d'évaluation

- Higher Level Paper 2 2010Document8 pagesHigher Level Paper 2 2010Mark MoloneyPas encore d'évaluation

- P5 Syl2012 InterDocument27 pagesP5 Syl2012 InterViswanathan SrkPas encore d'évaluation

- Specimen Examen F3 AccaDocument21 pagesSpecimen Examen F3 AccaGPas encore d'évaluation

- Technician Pilot Papers PDFDocument133 pagesTechnician Pilot Papers PDFCasius Mubamba100% (4)

- Ac5007 QuestionsDocument8 pagesAc5007 QuestionsyinlengPas encore d'évaluation

- Mock Exam Paper: Time AllowedDocument9 pagesMock Exam Paper: Time AllowedVannak2015Pas encore d'évaluation

- Taxation Management and PlanningDocument10 pagesTaxation Management and PlanningJoel EdauPas encore d'évaluation

- Draft Solutions Diploma in IFRS For SMEs Final Exam JD21Document84 pagesDraft Solutions Diploma in IFRS For SMEs Final Exam JD21Vuthy DaraPas encore d'évaluation

- Ca Foundation AccountsDocument7 pagesCa Foundation AccountssmartshivenduPas encore d'évaluation

- Easy Method Institute: Adjusting EntriesDocument6 pagesEasy Method Institute: Adjusting EntriesKader Jewel100% (1)

- Intermediate Group I Test PapersDocument57 pagesIntermediate Group I Test Paperssantbaksmishra1261Pas encore d'évaluation

- Fca Tax Ican November 2023 Mock QuestionsDocument8 pagesFca Tax Ican November 2023 Mock QuestionsArogundade kamaldeenPas encore d'évaluation

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionD'EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionPas encore d'évaluation

- AUDITDocument6 pagesAUDITCean MhangoPas encore d'évaluation

- TC9 (A)Document12 pagesTC9 (A)Cean MhangoPas encore d'évaluation

- Business KnowledgeDocument6 pagesBusiness KnowledgeCean MhangoPas encore d'évaluation

- AUDITDocument6 pagesAUDITCean MhangoPas encore d'évaluation

- ECONOMICSDocument6 pagesECONOMICSCean MhangoPas encore d'évaluation

- Company LawDocument5 pagesCompany LawCean MhangoPas encore d'évaluation

- Cost and Benefit Analysis BookDocument361 pagesCost and Benefit Analysis Book9315875729100% (7)

- SG 2Document29 pagesSG 2creatine2Pas encore d'évaluation

- Final Exam in Readings in Philippine HistoryDocument8 pagesFinal Exam in Readings in Philippine HistoryJeremy Espino-Santos100% (12)

- Hanlon Dan Heitzman (2010)Document52 pagesHanlon Dan Heitzman (2010)Vanica AudiPas encore d'évaluation

- Activity 1 Wih AnswersDocument2 pagesActivity 1 Wih AnswersDianna Tercino IIPas encore d'évaluation

- Business Ethics ReviewerDocument6 pagesBusiness Ethics ReviewerMa. Kyla Wayne Lacasandile100% (1)

- Federal GV Grant - txt-1Document5 pagesFederal GV Grant - txt-1Rhonda Heyman87% (31)

- Karnataka Engineering Company Limited (KECL)Document13 pagesKarnataka Engineering Company Limited (KECL)miku hrshPas encore d'évaluation

- Castlegar/Slocan Valley Pennywise Nov. 28, 2017Document36 pagesCastlegar/Slocan Valley Pennywise Nov. 28, 2017Pennywise PublishingPas encore d'évaluation

- Jacob PDFDocument12 pagesJacob PDFPrashant JacobPas encore d'évaluation

- 2 DIGEST Madrigal Vs Rafferty DigestDocument1 page2 DIGEST Madrigal Vs Rafferty DigestLeo FelicildaPas encore d'évaluation

- Business StructureDocument9 pagesBusiness StructureSuharthi SriramPas encore d'évaluation

- En PDF Toolkit HSS FinancingDocument14 pagesEn PDF Toolkit HSS FinancingRetno FebriantiPas encore d'évaluation

- Solar Purchase BillDocument2 pagesSolar Purchase BillMansi ShahPas encore d'évaluation

- Emirates Fare ConditionsDocument6 pagesEmirates Fare ConditionsMPC RaoPas encore d'évaluation

- 3.09 Set 3 Mock Exam ReaDocument5 pages3.09 Set 3 Mock Exam Reabhobot riveraPas encore d'évaluation

- IFM TB ch16Document9 pagesIFM TB ch16Faizan Ch100% (1)

- Regulation of Intermediaries, Including Tax Advisers, in The EU/Member States and Best Practices From Inside and Outside The EUDocument64 pagesRegulation of Intermediaries, Including Tax Advisers, in The EU/Member States and Best Practices From Inside and Outside The EUKgjkg KjkgPas encore d'évaluation

- 2015 AtcDocument27 pages2015 Atcmilanfan1984Pas encore d'évaluation

- GSTDocument59 pagesGSTkeval Chavan88% (8)

- EFU General Wins Achievement Award / Gold Medal of FPCCIDocument32 pagesEFU General Wins Achievement Award / Gold Medal of FPCCIawaisPas encore d'évaluation

- Employee Downsizing: Downsizing Blues All Over The WorldDocument11 pagesEmployee Downsizing: Downsizing Blues All Over The WorldZoya KhanPas encore d'évaluation

- Case Study 5.2Document5 pagesCase Study 5.2Jessa Beloy100% (6)

- NDC Vs CIR Source of InterestDocument4 pagesNDC Vs CIR Source of InterestEvan NervezaPas encore d'évaluation

- Begun and Held in Metro Manila, On Monday, The Twenty-Sixth Day of July, Nineteen Hundred and Ninety-ThreeDocument6 pagesBegun and Held in Metro Manila, On Monday, The Twenty-Sixth Day of July, Nineteen Hundred and Ninety-ThreeJILL ANGELESPas encore d'évaluation

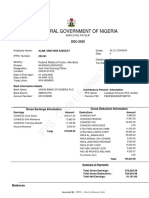

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- PRTC TAX-1stPB 0522 220221 091723Document16 pagesPRTC TAX-1stPB 0522 220221 091723MOTC INTERNAL AUDIT SECTIONPas encore d'évaluation

- Crossword MoneyDocument3 pagesCrossword MoneyÁgnes JassóPas encore d'évaluation

- Nishit MarvaniaDocument3 pagesNishit Marvaniaone_and_only_you0076406Pas encore d'évaluation

- Personal Finance ActivitiesDocument32 pagesPersonal Finance ActivitiesRonald CatapangPas encore d'évaluation