Vous aimerez peut-être aussi

- Commonwealth Act No. 63Document4 pagesCommonwealth Act No. 63Sherill Padua GapasinPas encore d'évaluation

- Art. 333 - 346 - Crimes Against ChastityDocument6 pagesArt. 333 - 346 - Crimes Against ChastityLeomar Despi LadongaPas encore d'évaluation

- Aznar Vs GarciaDocument1 pageAznar Vs GarciaLeomar Despi LadongaPas encore d'évaluation

- Art. 171 - 184Document8 pagesArt. 171 - 184Leomar Despi LadongaPas encore d'évaluation

- ObligationDocument2 pagesObligationLeomar Despi LadongaPas encore d'évaluation

- Gregorio Araneta Vs RodasDocument2 pagesGregorio Araneta Vs RodasLeomar Despi LadongaPas encore d'évaluation

- CRIMES AGAINST CIVIL STATUSDocument4 pagesCRIMES AGAINST CIVIL STATUSLeomar Despi LadongaPas encore d'évaluation

- Phil Bank Vs EchiverriDocument1 pagePhil Bank Vs EchiverriLeomar Despi LadongaPas encore d'évaluation

- Conflict CasesDocument28 pagesConflict CasesLeomar Despi LadongaPas encore d'évaluation

- Phil Bank Vs EchiverriDocument1 pagePhil Bank Vs EchiverriLeomar Despi LadongaPas encore d'évaluation

- NEGLIGENT ACTS UNDER PHILIPPINE LAWDocument3 pagesNEGLIGENT ACTS UNDER PHILIPPINE LAWLeomar Despi Ladonga100% (3)

- Full CasesDocument70 pagesFull CasesLeomar Despi LadongaPas encore d'évaluation

- Aznar Vs GarciaDocument1 pageAznar Vs GarciaLeomar Despi LadongaPas encore d'évaluation

- Art. 353 - 364 - Crimes Against HonorDocument13 pagesArt. 353 - 364 - Crimes Against HonorLeomar Despi Ladonga88% (8)

- Crimes Against State LawsDocument4 pagesCrimes Against State LawsLeomar Despi LadongaPas encore d'évaluation

- Book VDocument19 pagesBook VLeomar Despi LadongaPas encore d'évaluation

- January 11-20 2013 Civil CasesDocument1 pageJanuary 11-20 2013 Civil CasesLeomar Despi LadongaPas encore d'évaluation

- Mercantile Law 2013 October Bar ExamsDocument17 pagesMercantile Law 2013 October Bar ExamsNeil RiveraPas encore d'évaluation

- Bar Exams QuestionsDocument43 pagesBar Exams QuestionsLeomar Despi LadongaPas encore d'évaluation

- FActsDocument2 pagesFActsLeomar Despi LadongaPas encore d'évaluation

- MANPOWER SUPPLY AGREEMENTDocument3 pagesMANPOWER SUPPLY AGREEMENTLeomar Despi LadongaPas encore d'évaluation

- Complaint: X IncorporatedDocument6 pagesComplaint: X IncorporatedLeomar Despi LadongaPas encore d'évaluation

- Monte de Piedad Earthquake Relief Funds DisputeDocument11 pagesMonte de Piedad Earthquake Relief Funds DisputeLeomar Despi LadongaPas encore d'évaluation

- Spouses Yap vs. International Exchange BankDocument1 pageSpouses Yap vs. International Exchange BankLeomar Despi LadongaPas encore d'évaluation

- Bildner V IlusorioDocument8 pagesBildner V IlusorioLeomar Despi LadongaPas encore d'évaluation

- Basco V PagcorDocument1 pageBasco V PagcorLeomar Despi LadongaPas encore d'évaluation

- Chan Robles Virtual Law LibraryDocument7 pagesChan Robles Virtual Law LibraryLeomar Despi LadongaPas encore d'évaluation

- Simple Tenses and Perfect Tenses ExplainedDocument3 pagesSimple Tenses and Perfect Tenses ExplainedLeomar Despi LadongaPas encore d'évaluation

- BDO Bank Account Authorization CertificateDocument3 pagesBDO Bank Account Authorization CertificateLeomar Despi LadongaPas encore d'évaluation

- RTC Hilongos Leyte People Philippines vs AB arson informationDocument1 pageRTC Hilongos Leyte People Philippines vs AB arson informationLeomar Despi LadongaPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Lecture 4 Corp Personality 130917-4 PDFDocument23 pagesLecture 4 Corp Personality 130917-4 PDF靳雪娇Pas encore d'évaluation

- PB-OBLIGATIONS-SET B Q&A - AnswersDocument28 pagesPB-OBLIGATIONS-SET B Q&A - AnswersKenneth John TomasPas encore d'évaluation

- Company Regulation SampleDocument13 pagesCompany Regulation SampleJames Oludele Etu67% (3)

- Home Loan Process at Dena BankDocument57 pagesHome Loan Process at Dena BankDeshrajsingh SengarPas encore d'évaluation

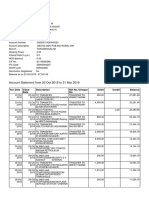

- Account Statement From 16 Sep 2019 To 16 Mar 2020Document2 pagesAccount Statement From 16 Sep 2019 To 16 Mar 2020SUNYYRPas encore d'évaluation

- SEBI ICDR Chapter V Preferential Issue ExemptionsDocument2 pagesSEBI ICDR Chapter V Preferential Issue Exemptionskpved92Pas encore d'évaluation

- How To Take Money From ATM: Procedure TextDocument1 pageHow To Take Money From ATM: Procedure TextOctavinaPas encore d'évaluation

- Law 204: Easy Way To Read Section 17 of The Registration Act 1908Document6 pagesLaw 204: Easy Way To Read Section 17 of The Registration Act 1908Efaz Mahamud AzadPas encore d'évaluation

- SPOUSES EDUARDO and LYDIA SILOS, Petitioners, Philippine National Bank, Respondent. FACTS: Spouses Eduardo and Lydia Silos (Petitioners) Have Been inDocument4 pagesSPOUSES EDUARDO and LYDIA SILOS, Petitioners, Philippine National Bank, Respondent. FACTS: Spouses Eduardo and Lydia Silos (Petitioners) Have Been indaryllPas encore d'évaluation

- Handouts For Credit TransactionsDocument15 pagesHandouts For Credit TransactionsIrene Sheeran100% (1)

- Corpus Christi Town Club Order Authorizing Auction SaleDocument1 pageCorpus Christi Town Club Order Authorizing Auction SalecallertimesPas encore d'évaluation

- Quick Reference To Base 24 Error CodesDocument2 pagesQuick Reference To Base 24 Error Codesthangella_nagendra0% (1)

- Income From House PropertyDocument12 pagesIncome From House PropertydipxxxPas encore d'évaluation

- FABM2 - Statement of Financial PositionDocument36 pagesFABM2 - Statement of Financial PositionVron Blatz100% (6)

- Debt Collection in India Why Is It So DifficultDocument2 pagesDebt Collection in India Why Is It So DifficultSoumiki GhoshPas encore d'évaluation

- Adjustments To Financial Statements - Students - ACCA Global - ACCA GlobalDocument4 pagesAdjustments To Financial Statements - Students - ACCA Global - ACCA Globalacca_kaplan100% (1)

- TATA Card - PaynetmarchDocument2 pagesTATA Card - PaynetmarchabhilashaupadhyayaPas encore d'évaluation

- Instructions For Completing This Form 13.1 Financial StatementDocument33 pagesInstructions For Completing This Form 13.1 Financial StatementMy Support CalculatorPas encore d'évaluation

- Max Gardner's Top 200 Signs You've Got A False Document As Published by The Florida Bar in 2008Document18 pagesMax Gardner's Top 200 Signs You've Got A False Document As Published by The Florida Bar in 2008lizinsarasota100% (2)

- 2003 Hbos RaDocument124 pages2003 Hbos RasaxobobPas encore d'évaluation

- Deed of Antichresis ExplainedDocument2 pagesDeed of Antichresis Explainedjoshboracay100% (8)

- Transcribe 2nd MeetingDocument4 pagesTranscribe 2nd MeetingGian Paula MonghitPas encore d'évaluation

- Plaintiff-Appellee Vs Vs Defendant-Appellant Araneta & Zaragosa Ross, Lawrence & Selph Andres NicolasDocument7 pagesPlaintiff-Appellee Vs Vs Defendant-Appellant Araneta & Zaragosa Ross, Lawrence & Selph Andres NicolasCams Tres ReyesPas encore d'évaluation

- Paper8 Solution PDFDocument22 pagesPaper8 Solution PDFbinuPas encore d'évaluation

- Keshavlal Khemchand and Sons Private Ltd. v. Union of India PDFDocument52 pagesKeshavlal Khemchand and Sons Private Ltd. v. Union of India PDFBar & BenchPas encore d'évaluation

- Philippine Financial System StructureDocument28 pagesPhilippine Financial System StructureJenielyn Delamata83% (6)

- Klkiulm QDQ PK 4 SXDocument8 pagesKlkiulm QDQ PK 4 SXkarthickPas encore d'évaluation

- Araneta V PaternoDocument5 pagesAraneta V PaternopurplebasketPas encore d'évaluation

- Topic 2 Guide - Due Diligence and Takeover LawDocument5 pagesTopic 2 Guide - Due Diligence and Takeover LawHubibPas encore d'évaluation

- Balus Vs Balus Case DigestDocument3 pagesBalus Vs Balus Case DigestHanna TevesPas encore d'évaluation