Vous aimerez peut-être aussi

- Understanding The Guilty Plea Process - Criminal Defence Articles by Tushar K. PainDocument4 pagesUnderstanding The Guilty Plea Process - Criminal Defence Articles by Tushar K. PainEdgar Roberto AcostaPas encore d'évaluation

- Civil Procedure DoctrinesDocument51 pagesCivil Procedure DoctrinesEricha Joy GonadanPas encore d'évaluation

- Lifting The Corporate VeilDocument6 pagesLifting The Corporate VeilChanda ZmPas encore d'évaluation

- Doing Business Under The Name and Style of : Smart Speed, IncDocument7 pagesDoing Business Under The Name and Style of : Smart Speed, IncAira Dee SuarezPas encore d'évaluation

- Financial Leverage Ratios, Sometimes Called Equity or Debt Ratios, MeasureDocument11 pagesFinancial Leverage Ratios, Sometimes Called Equity or Debt Ratios, MeasureBonDocEldRicPas encore d'évaluation

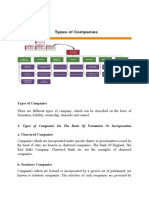

- Types of Companies and OPC - NotesDocument8 pagesTypes of Companies and OPC - Notes23Mansi JainIPas encore d'évaluation

- "Penny For Your Thoughts": Live Webcast Hosted byDocument78 pages"Penny For Your Thoughts": Live Webcast Hosted byZerohedgePas encore d'évaluation

- Duty of DirectorDocument10 pagesDuty of DirectorRenee WongPas encore d'évaluation

- Chapter 3 Strateging & Structuing M & A ActivityDocument13 pagesChapter 3 Strateging & Structuing M & A ActivityNareshPas encore d'évaluation

- Companies Law: Presented by Deepshikha Meeta Nikita ShivaniDocument63 pagesCompanies Law: Presented by Deepshikha Meeta Nikita ShivaniSahil SherasiyaPas encore d'évaluation

- D Mercer - Private Client Case Study-V1Document5 pagesD Mercer - Private Client Case Study-V1kapoor_mukesh4uPas encore d'évaluation

- Tax Compliance On PayrollDocument2 pagesTax Compliance On PayrollJoycePas encore d'évaluation

- Registration Procedure Under Central Sales Act (SectionDocument23 pagesRegistration Procedure Under Central Sales Act (SectionkgudiyaPas encore d'évaluation

- 2.) Mendiola-vs-CADocument3 pages2.) Mendiola-vs-CARusty SeymourPas encore d'évaluation

- Start BusinessDocument3 pagesStart BusinessBayari E EricPas encore d'évaluation

- Employee Handbook: Welcome To Archetive Solutions PVT - LTDDocument24 pagesEmployee Handbook: Welcome To Archetive Solutions PVT - LTDAnindita SahaPas encore d'évaluation

- Chapter 4 Due DiligenceDocument23 pagesChapter 4 Due DiligenceAshish DavePas encore d'évaluation

- Amazing Facts About Big 4 Accounting FirmsDocument20 pagesAmazing Facts About Big 4 Accounting FirmssandyskadamPas encore d'évaluation

- Law Firm Partnership AgreementsDocument7 pagesLaw Firm Partnership Agreementsgivamathan100% (2)

- Law of PersonsDocument21 pagesLaw of PersonsFatma KhamisPas encore d'évaluation

- Direct Tax CodeDocument25 pagesDirect Tax CodeHk MeherPas encore d'évaluation

- Singleton v. Cannizzaro FILED 10 17 17Document62 pagesSingleton v. Cannizzaro FILED 10 17 17Monique Judge100% (1)

- Chapter 1.introduction To AccountingDocument63 pagesChapter 1.introduction To AccountingIan SumastrePas encore d'évaluation

- Chapter-5-Drafting Fundamental Documents PDFDocument4 pagesChapter-5-Drafting Fundamental Documents PDFShubham AgarwalPas encore d'évaluation

- Legal Aspects of Business Unit 4 Ms Neha RaniDocument123 pagesLegal Aspects of Business Unit 4 Ms Neha Ranihari haranPas encore d'évaluation

- The Corporation Code of The Philippines B.P. Blg. 68: Lecture 3 (Parts 1 and 2) June 22, 2011Document86 pagesThe Corporation Code of The Philippines B.P. Blg. 68: Lecture 3 (Parts 1 and 2) June 22, 2011MaanParrenoVillarPas encore d'évaluation

- Sales Tax GuideDocument6 pagesSales Tax GuideakhileshkantPas encore d'évaluation

- Complaint (ECF File Stamp)Document34 pagesComplaint (ECF File Stamp)Mark Crabtree LawsuitPas encore d'évaluation

- Corporate Leagal Framework 3Document553 pagesCorporate Leagal Framework 3Gurpreet SainiPas encore d'évaluation

- Deductions From Gross IncomeDocument2 pagesDeductions From Gross Incomericamae saladagaPas encore d'évaluation

- SRA Principles and Code of ConductDocument35 pagesSRA Principles and Code of ConductDang DangPas encore d'évaluation

- The Company Act, 1956 PDFDocument34 pagesThe Company Act, 1956 PDFSahitya SoniPas encore d'évaluation

- DTC ProvisionsDocument3 pagesDTC ProvisionsrajdeeppawarPas encore d'évaluation

- The 4 Major Business Organization FormsDocument3 pagesThe 4 Major Business Organization FormsRemo Task RivbPas encore d'évaluation

- Advanced Tax Laws CS Professional, YES AcademyDocument33 pagesAdvanced Tax Laws CS Professional, YES AcademyKaran AroraPas encore d'évaluation

- Political Law DoctrinesDocument19 pagesPolitical Law DoctrinesRoselle IsonPas encore d'évaluation

- Duty of DirectorDocument11 pagesDuty of DirectorNur Afiza TaliPas encore d'évaluation

- Directors DutiesDocument24 pagesDirectors DutiesselvavishnuPas encore d'évaluation

- Ganzon V CADocument4 pagesGanzon V CAMarefel AnoraPas encore d'évaluation

- Pasong Bayabas V. Ca Darab V. Ca: (G.R. No. 142980. May 25, 2004)Document4 pagesPasong Bayabas V. Ca Darab V. Ca: (G.R. No. 142980. May 25, 2004)Jun RiveraPas encore d'évaluation

- NG Hee Thong - CLJ - 1995 - 1 - 609 - PSB PDFDocument10 pagesNG Hee Thong - CLJ - 1995 - 1 - 609 - PSB PDFMaisarah Md IsaPas encore d'évaluation

- Quizzer On Corporation Code Oft He Philippines: By: Atty. Bryan Jasper D. SolisDocument4 pagesQuizzer On Corporation Code Oft He Philippines: By: Atty. Bryan Jasper D. SolisBryan Jasper D. Solis0% (1)

- Chapter 10-Advanced VariancesDocument36 pagesChapter 10-Advanced VariancesKevin Kausiyo100% (5)

- University of London La3021 OctoberDocument6 pagesUniversity of London La3021 OctoberdaneelPas encore d'évaluation

- The Legal Nature of A Company in ZimbabweDocument11 pagesThe Legal Nature of A Company in ZimbabweVincent MutambirwaPas encore d'évaluation

- Introduction of CompanyDocument45 pagesIntroduction of CompanykritiPas encore d'évaluation

- Accounting TerminologiesDocument16 pagesAccounting TerminologiesRidhanrhsnPas encore d'évaluation

- CS Executive Corporate and Management AccountingDocument17 pagesCS Executive Corporate and Management AccountingSuraj Srivatsav.SPas encore d'évaluation

- The Consumer Protection Act Was Implemented in Order To Provide Better Protection To The Rights of The ConsumersDocument15 pagesThe Consumer Protection Act Was Implemented in Order To Provide Better Protection To The Rights of The ConsumersSuraj DewasiPas encore d'évaluation

- The Duty of Loyalty From Directors, Partners and Senior Employees - Gaby Hardwicke SolicitorsDocument17 pagesThe Duty of Loyalty From Directors, Partners and Senior Employees - Gaby Hardwicke SolicitorsAndres RestrepoPas encore d'évaluation

- Corporate PersonalityDocument6 pagesCorporate PersonalityRizvan NoorPas encore d'évaluation

- Company Law-Legal Entity of A CompanyDocument12 pagesCompany Law-Legal Entity of A CompanyElvinPas encore d'évaluation

- ACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Document66 pagesACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Harshit Kumar GuptaPas encore d'évaluation

- Company LawDocument474 pagesCompany LawSimranPas encore d'évaluation

- Public and Private CompanyDocument3 pagesPublic and Private CompanyGarima GarimaPas encore d'évaluation

- Directors Fiduciary Duty To A Company (India)Document19 pagesDirectors Fiduciary Duty To A Company (India)AKHIL H KRISHNANPas encore d'évaluation

- Incorporation of A Company Business LawDocument12 pagesIncorporation of A Company Business LawRiya Aggarwal100% (1)

- Cash Control GuidelinesDocument4 pagesCash Control GuidelinesEsmeldo MicasPas encore d'évaluation

- Nature and Formation of A CompanyDocument15 pagesNature and Formation of A CompanyCOLLINS MWANGI NJOROGEPas encore d'évaluation

- Joint Stock CompanyDocument40 pagesJoint Stock Companyarun447Pas encore d'évaluation

- PWC Directors' Duties Checklist PDFDocument24 pagesPWC Directors' Duties Checklist PDFpanaglawPas encore d'évaluation

- Project On Corporate GovernanceDocument22 pagesProject On Corporate GovernancePallavi PradhanPas encore d'évaluation

- Corporate Bylaws FormDocument12 pagesCorporate Bylaws FormYong Loon NgPas encore d'évaluation

- Consumerism: Presented ByDocument18 pagesConsumerism: Presented ByMadhupriya SinghPas encore d'évaluation

- Limited Liability Companies Act Chapter 151 of The Revised Laws of Saint Vincent and The Grenadines, 2009Document63 pagesLimited Liability Companies Act Chapter 151 of The Revised Laws of Saint Vincent and The Grenadines, 2009Logan's LtdPas encore d'évaluation

- Strategic Tax Management - Week 2Document44 pagesStrategic Tax Management - Week 2Arman DalisayPas encore d'évaluation

- Veil of IncorporationDocument2 pagesVeil of IncorporationShrestha Steve SalvatorePas encore d'évaluation

- TX ZAF Examiner's ReportDocument9 pagesTX ZAF Examiner's ReportKevin KausiyoPas encore d'évaluation

- Student Accountant Hub Page: Analytical ProceduresDocument4 pagesStudent Accountant Hub Page: Analytical ProceduresKevin KausiyoPas encore d'évaluation

- Motivation Letter For A Shop AssistantDocument1 pageMotivation Letter For A Shop AssistantKevin KausiyoPas encore d'évaluation

- F2 TranscriptDocument16 pagesF2 TranscriptKevin KausiyoPas encore d'évaluation

- Paper 2 Information For Management Control: Study Guide - Upto November 2011 Certified Accounting Technician ExaminationDocument7 pagesPaper 2 Information For Management Control: Study Guide - Upto November 2011 Certified Accounting Technician ExaminationKevin KausiyoPas encore d'évaluation

- Uy Ek Liong Vs CastilloDocument9 pagesUy Ek Liong Vs CastilloCamille Benjamin RemorozaPas encore d'évaluation

- Contract For The Sale of Goods Seller Friendly VersionDocument3 pagesContract For The Sale of Goods Seller Friendly VersionSomnath BabanagarPas encore d'évaluation

- The Place of The Minor in The AdministraDocument22 pagesThe Place of The Minor in The AdministraRANDAN SADIQPas encore d'évaluation

- Atienza Vs EspidolDocument17 pagesAtienza Vs EspidolAtty. R. PerezPas encore d'évaluation

- EriazariDiisi MbararaTradingStoresDocument8 pagesEriazariDiisi MbararaTradingStoresReal TrekstarPas encore d'évaluation

- Company Law ProjectDocument10 pagesCompany Law ProjectdevPas encore d'évaluation

- Deed of Guarantee For MTN ServicesDocument2 pagesDeed of Guarantee For MTN Servicesnanayaw asarePas encore d'évaluation

- Morigo v. PeopleDocument6 pagesMorigo v. PeoplecyhaaangelaaaPas encore d'évaluation

- Administrative LawDocument248 pagesAdministrative Lawmohd sakibPas encore d'évaluation

- Citibank V CaDocument18 pagesCitibank V CaCarrie Anne GarciaPas encore d'évaluation

- Module Law On Obligations and ContractsDocument32 pagesModule Law On Obligations and ContractsMariecris Martinez100% (1)

- Third Division (G.R. No. 224650, July 15, 2020) People of The Philippines, Petitioner, vs. Adolfo A. Goyala, JR., Respondent. Decision Gesmundo, J.Document6 pagesThird Division (G.R. No. 224650, July 15, 2020) People of The Philippines, Petitioner, vs. Adolfo A. Goyala, JR., Respondent. Decision Gesmundo, J.christian villamantePas encore d'évaluation

- Orders 12 & 13 (Civil Pro.) - Appearance & Default of AppearanceDocument7 pagesOrders 12 & 13 (Civil Pro.) - Appearance & Default of AppearancesamcessPas encore d'évaluation

- Albert vs. SandiganbayanDocument6 pagesAlbert vs. SandiganbayanRencePas encore d'évaluation

- Nluo Imam Claimant MemorandumDocument38 pagesNluo Imam Claimant MemorandumMuktesh SwamyPas encore d'évaluation

- Torts II. NegligenceDocument115 pagesTorts II. NegligenceRuby Capinig InocencioPas encore d'évaluation

- ABCs of Remedial LawDocument18 pagesABCs of Remedial LawEden RachoPas encore d'évaluation

- Public LiabilityDocument9 pagesPublic LiabilityKhouloud FerchichiPas encore d'évaluation

- Incorporators.: 2. That The Purpose or Purposes of The Corporation AreDocument7 pagesIncorporators.: 2. That The Purpose or Purposes of The Corporation AreLaw StudentPas encore d'évaluation

- LL.B I Contract SlidesDocument136 pagesLL.B I Contract Slidesyusuph ntegaz100% (1)

- Maid FormDocument2 pagesMaid FormhutuguoPas encore d'évaluation

- Global Business Holding, Inc. vs. Surecomp Sofware, B.V.Document7 pagesGlobal Business Holding, Inc. vs. Surecomp Sofware, B.V.Alexander Julio ValeraPas encore d'évaluation

- Definition of Partnership FirmDocument3 pagesDefinition of Partnership FirmAditya VermaPas encore d'évaluation