Vous aimerez peut-être aussi

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsD'Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsPas encore d'évaluation

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryD'EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryPas encore d'évaluation

- Rahul Agrawal's Salary Income AnalysisDocument32 pagesRahul Agrawal's Salary Income AnalysiskiranshingotePas encore d'évaluation

- Rahul Agrawal's Salary Income AnalysisDocument32 pagesRahul Agrawal's Salary Income AnalysiskiranshingotePas encore d'évaluation

- Income From Salary' & Its Computation: TaxationDocument35 pagesIncome From Salary' & Its Computation: TaxationChintan ShahPas encore d'évaluation

- 40 40 Income From Salary BTDocument55 pages40 40 Income From Salary BTkiranshingotePas encore d'évaluation

- Meaning of Salary': Condition For Charging Income U/H "Salaries"Document21 pagesMeaning of Salary': Condition For Charging Income U/H "Salaries"kiranshingotePas encore d'évaluation

- Salary IncomeDocument47 pagesSalary Incomearchana_anuragiPas encore d'évaluation

- Income From Salary GuideDocument11 pagesIncome From Salary Guiderakshitha9reddy-1Pas encore d'évaluation

- Income From SalaryDocument54 pagesIncome From SalaryMohsin ShaikhPas encore d'évaluation

- Income From SalariesDocument70 pagesIncome From SalariesPratik AgrawalPas encore d'évaluation

- Income From SalaryDocument29 pagesIncome From SalaryIsmail SayyadPas encore d'évaluation

- Income From SalariesDocument30 pagesIncome From SalariesDeepak Gupta50% (2)

- Salary Includes: U/s 17Document14 pagesSalary Includes: U/s 17Ansh NayyarPas encore d'évaluation

- Income From SalariesDocument28 pagesIncome From SalariesAshok Kumar Meheta100% (2)

- Salary Income LawDocument25 pagesSalary Income Lawvishal singhPas encore d'évaluation

- Learn Income Tax in Easy StepsDocument79 pagesLearn Income Tax in Easy Stepsbushra_anwarPas encore d'évaluation

- Provisions of Salary Taxation and Deductions under Section 15, 16, 17Document46 pagesProvisions of Salary Taxation and Deductions under Section 15, 16, 17Dhiraj YAdavPas encore d'évaluation

- Module 2 - Income From SalariesDocument22 pagesModule 2 - Income From SalariesAishwarya NPas encore d'évaluation

- Income From SalariesDocument48 pagesIncome From Salarieskeerthana_hassan67% (6)

- 1.income From SalaryDocument10 pages1.income From Salaryshagunbhatnagar2Pas encore d'évaluation

- Tax Rules for Salary IncomeDocument16 pagesTax Rules for Salary IncomeNoob GamerPas encore d'évaluation

- Final Indirect Tax ProjectDocument39 pagesFinal Indirect Tax Projectssg1015Pas encore d'évaluation

- Income Under The Head Salaries: (Section 15 - 17)Document55 pagesIncome Under The Head Salaries: (Section 15 - 17)leela naga janaki rajitha attiliPas encore d'évaluation

- Tax ProjectDocument34 pagesTax Projectjinalshah21097946Pas encore d'évaluation

- tax Unit 4 (Tax on Individual)Document116 pagestax Unit 4 (Tax on Individual)Shivam PalPas encore d'évaluation

- O Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiDocument7 pagesO Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiRadhika SarawagiPas encore d'évaluation

- Unit V HR OperationsDocument43 pagesUnit V HR OperationssnehalPas encore d'évaluation

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalPas encore d'évaluation

- P2Document18 pagesP2YusufPas encore d'évaluation

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- Income From SalariesDocument19 pagesIncome From SalariesVineeta WadhwaniPas encore d'évaluation

- Salary IncomeDocument83 pagesSalary IncomechitkarashellyPas encore d'évaluation

- Financial Planning For Salaried Employee and Strategies For Tax SavingsDocument10 pagesFinancial Planning For Salaried Employee and Strategies For Tax Savingscity cyberPas encore d'évaluation

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaPas encore d'évaluation

- Salary SimplifiedDocument16 pagesSalary SimplifiedaruunstalinPas encore d'évaluation

- Income Chargeable Under The Head Salaries - Taxguru - inDocument12 pagesIncome Chargeable Under The Head Salaries - Taxguru - insayali jadhavPas encore d'évaluation

- Income From SalaryDocument22 pagesIncome From SalaryJatin DrallPas encore d'évaluation

- Income From SalaryDocument54 pagesIncome From SalaryJyoti Kalotra70% (10)

- Unit 2 Notes, Part 1Document19 pagesUnit 2 Notes, Part 1Sandip Kumar BhartiPas encore d'évaluation

- Income From Salary-FinalDocument42 pagesIncome From Salary-FinalPrathibha TiwariPas encore d'évaluation

- Income From SalaryDocument66 pagesIncome From SalaryShamika LloydPas encore d'évaluation

- Q&A: Income Tax Deductions and TDS ProvisionsDocument7 pagesQ&A: Income Tax Deductions and TDS ProvisionsAnamika VatsaPas encore d'évaluation

- Salary Income-Pg DTDocument11 pagesSalary Income-Pg DTOnkar BandichhodePas encore d'évaluation

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaPas encore d'évaluation

- Income Under The Head "Salaries"Document7 pagesIncome Under The Head "Salaries"Rahul AgarwalPas encore d'évaluation

- TDS & TCSDocument107 pagesTDS & TCSSANDEEP CHAUREPas encore d'évaluation

- Law of Taxation - Income Under The Head Salary (Autosaved)Document78 pagesLaw of Taxation - Income Under The Head Salary (Autosaved)Naman GoyalPas encore d'évaluation

- Lesson 4 Income Under The Head Salaries - I: StructureDocument14 pagesLesson 4 Income Under The Head Salaries - I: StructuredrcpjoshiPas encore d'évaluation

- Project On:-Income From SalaryDocument32 pagesProject On:-Income From SalaryNida UldayPas encore d'évaluation

- Income Tax Law and PracticesDocument26 pagesIncome Tax Law and Practicesremruata rascalraltePas encore d'évaluation

- Taxable Salary IncomeDocument253 pagesTaxable Salary IncomedjbbuzzzPas encore d'évaluation

- Chapter 4: Income From Salaries (Section 15 To 17) : Advance Direct Tax and Service Tax (Sub Code: 441)Document34 pagesChapter 4: Income From Salaries (Section 15 To 17) : Advance Direct Tax and Service Tax (Sub Code: 441)Puneeth DhondalePas encore d'évaluation

- Income From SalaryDocument16 pagesIncome From SalaryGurpreet Singh100% (1)

- Income TaxDocument16 pagesIncome TaxNikhil KumarPas encore d'évaluation

- Income Tax Planning for Salary and House Property IncomeDocument51 pagesIncome Tax Planning for Salary and House Property IncomeRavi SinghPas encore d'évaluation

- Income From Salary Final SEM 3Document49 pagesIncome From Salary Final SEM 3Baleshwar ChauhanPas encore d'évaluation

- SalariesDocument6 pagesSalariesrichaPas encore d'évaluation

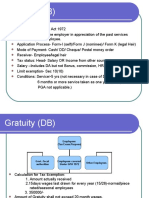

- GratuityDocument7 pagesGratuitySandeep TakPas encore d'évaluation

- Income From SalariesDocument19 pagesIncome From SalariesTaruna ShandilyaPas encore d'évaluation

- Business Ethics - Ch5 (Samandova&Huseynali) PDFDocument16 pagesBusiness Ethics - Ch5 (Samandova&Huseynali) PDFkiranshingotePas encore d'évaluation

- A Model of Business Ethics: Exploring Expectations, Perceptions, Evaluations and OutcomesDocument20 pagesA Model of Business Ethics: Exploring Expectations, Perceptions, Evaluations and OutcomesvirtualatallPas encore d'évaluation

- 17 Business Ethics ImpDocument21 pages17 Business Ethics ImpkiranshingotePas encore d'évaluation

- 41 Business EthicsDocument16 pages41 Business EthicsPrashant RaiPas encore d'évaluation

- Principles of Business EthicsDocument26 pagesPrinciples of Business EthicskiranshingotePas encore d'évaluation

- Environmental Report12 Fe PDFDocument17 pagesEnvironmental Report12 Fe PDFkiranshingotePas encore d'évaluation

- 31 31 EthicsDocument18 pages31 31 EthicskiranshingotePas encore d'évaluation

- Business Strategies of Wal MartDocument22 pagesBusiness Strategies of Wal MartkiranshingotePas encore d'évaluation

- CODE OF ETHICS AND AUDITOR INDEPENDENCEDocument17 pagesCODE OF ETHICS AND AUDITOR INDEPENDENCEkiranshingotePas encore d'évaluation

- Work Ethics and MotivationDocument16 pagesWork Ethics and Motivationsimply_coool100% (3)

- 15 15 InfyDocument21 pages15 15 InfykiranshingotePas encore d'évaluation

- 16 16 PPT On Business EthicsDocument28 pages16 16 PPT On Business EthicskiranshingotePas encore d'évaluation

- Woosley Introduction To Environmental Management SystemsDocument50 pagesWoosley Introduction To Environmental Management Systemschandro57Pas encore d'évaluation

- Business EthicsDocument322 pagesBusiness EthicssameerzakPas encore d'évaluation

- Designpatterns 12 PDFDocument40 pagesDesignpatterns 12 PDFkiranshingotePas encore d'évaluation

- Using Design Patterns With GRASP: G R A S PDocument34 pagesUsing Design Patterns With GRASP: G R A S PkiranshingotePas encore d'évaluation

- Designpatterns 11 PDFDocument32 pagesDesignpatterns 11 PDFkiranshingotePas encore d'évaluation

- Woosley Introduction To Environmental Management SystemsDocument50 pagesWoosley Introduction To Environmental Management Systemschandro57Pas encore d'évaluation

- Designpatterns 10 PDFDocument23 pagesDesignpatterns 10 PDFkiranshingotePas encore d'évaluation

- The Command Pattern for Software DesignDocument29 pagesThe Command Pattern for Software DesignkiranshingotePas encore d'évaluation

- The Observer Pattern: CSCI 3132 Summer 2011Document33 pagesThe Observer Pattern: CSCI 3132 Summer 2011kiranshingotePas encore d'évaluation

- Designpatterns 08 PDFDocument32 pagesDesignpatterns 08 PDFkiranshingotePas encore d'évaluation

- Designpatterns 02 RDD Strategy PDFDocument36 pagesDesignpatterns 02 RDD Strategy PDFkiranshingotePas encore d'évaluation

- Designpatterns 07 PDFDocument33 pagesDesignpatterns 07 PDFkiranshingotePas encore d'évaluation

- Strategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1Document16 pagesStrategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1kiranshingotePas encore d'évaluation

- Designpatterns 03 PDFDocument35 pagesDesignpatterns 03 PDFkiranshingotePas encore d'évaluation

- Designpatterns 06 PDFDocument19 pagesDesignpatterns 06 PDFkiranshingotePas encore d'évaluation

- Designpatterns 03 PDFDocument35 pagesDesignpatterns 03 PDFkiranshingotePas encore d'évaluation

- Designpatterns 01 Adapter Facade PDFDocument23 pagesDesignpatterns 01 Adapter Facade PDFkiranshingotePas encore d'évaluation

- Strategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1Document16 pagesStrategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1kiranshingotePas encore d'évaluation

- Maslow's Hierarchy of Needs & Herzberg's Two Factor Theory ExplainedDocument79 pagesMaslow's Hierarchy of Needs & Herzberg's Two Factor Theory ExplainedsoraruPas encore d'évaluation

- The Impact of Employee Smiles on Customer SatisfactionDocument6 pagesThe Impact of Employee Smiles on Customer Satisfactionnileshstat5Pas encore d'évaluation

- LABOR - Alilin v. Petron Corp.Document14 pagesLABOR - Alilin v. Petron Corp.LBAPas encore d'évaluation

- HR Success Story of India's Largest Thermal Company NTPCDocument14 pagesHR Success Story of India's Largest Thermal Company NTPCGyandeep PradhanPas encore d'évaluation

- 6 Performance ManagementDocument36 pages6 Performance ManagementHumaira RaoPas encore d'évaluation

- Human Resources or Office Manager or Payroll Clerk or HR AssistaDocument2 pagesHuman Resources or Office Manager or Payroll Clerk or HR Assistaapi-121456849Pas encore d'évaluation

- Convention Management - Managing Human ResourceDocument22 pagesConvention Management - Managing Human ResourceJenny NguPas encore d'évaluation

- Job Satisfaction BBADocument83 pagesJob Satisfaction BBAsudhirPas encore d'évaluation

- Hawthorne StudiesDocument13 pagesHawthorne Studiesparivesh16Pas encore d'évaluation

- Presentation RahulDocument15 pagesPresentation RahulRahul MandruPas encore d'évaluation

- Chap003 (C7 Maimunah) - Safety and Health at WorkDocument19 pagesChap003 (C7 Maimunah) - Safety and Health at WorkNik ZazlealizaPas encore d'évaluation

- PRS HRDocument13 pagesPRS HRSameydan MohamedPas encore d'évaluation

- ESIC BenefitsDocument12 pagesESIC Benefitsraktim100Pas encore d'évaluation

- Safety ManagementDocument4 pagesSafety ManagementBeauMattyPas encore d'évaluation

- AlienationDocument2 pagesAlienationEllen Bumal-oPas encore d'évaluation

- Employee WelfareDocument19 pagesEmployee Welfaresaurav meenaPas encore d'évaluation

- Building A High-Performance CultureDocument29 pagesBuilding A High-Performance CultureMazhar IrfanPas encore d'évaluation

- General Instruction - Domestic Vendors (For Service)Document5 pagesGeneral Instruction - Domestic Vendors (For Service)Ramu NallathambiPas encore d'évaluation

- Job Satisfaction: A Literature Review: Aziri BDocument16 pagesJob Satisfaction: A Literature Review: Aziri Brija ravindranPas encore d'évaluation

- Labor Cost AccountingDocument6 pagesLabor Cost AccountingleerenjyePas encore d'évaluation

- Problems Facing Men in OrganizationDocument11 pagesProblems Facing Men in OrganizationJosenia ConstantinoPas encore d'évaluation

- Labor Law Chapter-2Document9 pagesLabor Law Chapter-2Toriqul IslamPas encore d'évaluation

- US DOL Fact Sheet 73 Break Time For Nursing MothersDocument2 pagesUS DOL Fact Sheet 73 Break Time For Nursing MothersMolly DiBiancaPas encore d'évaluation

- The History of Human Resource ManagementDocument7 pagesThe History of Human Resource ManagementFarahZahidiPas encore d'évaluation

- Cts Question Paper 27 JUNE 2005Document2 pagesCts Question Paper 27 JUNE 2005Janardhan DevaraPas encore d'évaluation

- 4.elaine D. Pulakos.A Fresh Look PDFDocument44 pages4.elaine D. Pulakos.A Fresh Look PDFChris CheonggPas encore d'évaluation

- Chapter 6Document27 pagesChapter 6Hong AnhPas encore d'évaluation

- Business Continuity Planning Policy SampleDocument2 pagesBusiness Continuity Planning Policy SamplePatricio Alejandro Vargas FuenzalidaPas encore d'évaluation

- Soal UKK Kelas X Bahasa InggrisDocument4 pagesSoal UKK Kelas X Bahasa InggrisSalman FauziPas encore d'évaluation

- Darden Case Book 2013Document173 pagesDarden Case Book 2013Swapnika Nag0% (1)