Vous aimerez peut-être aussi

- Grammatical Categories of Word N Their InflectionsDocument16 pagesGrammatical Categories of Word N Their InflectionsMohd Uzair YahyaPas encore d'évaluation

- Workplace CounselingDocument5 pagesWorkplace CounselingMohd Uzair Yahya100% (1)

- CMPF112-module3 3Document50 pagesCMPF112-module3 3Mohd Uzair YahyaPas encore d'évaluation

- Counselling ModelsDocument5 pagesCounselling ModelsMohd Uzair Yahya83% (6)

- Counseling in Corporate Industry-WorkplaceDocument16 pagesCounseling in Corporate Industry-WorkplaceMohd Uzair YahyaPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Conceptual Framework of TaxDocument9 pagesConceptual Framework of Taxdpak bhusalPas encore d'évaluation

- Capshaw WagesDocument2 pagesCapshaw Wagesapi-583619940Pas encore d'évaluation

- Electric Bill Backup PDFDocument1 pageElectric Bill Backup PDFfahmad_cmsPas encore d'évaluation

- Registration Form ISAR 2023 LatestDocument2 pagesRegistration Form ISAR 2023 LatestNinerMike MysPas encore d'évaluation

- 08 Portillo vs. CIRDocument2 pages08 Portillo vs. CIRBasil MaguigadPas encore d'évaluation

- Essentials of Federal Income Taxation For Individuals and BusinessDocument860 pagesEssentials of Federal Income Taxation For Individuals and BusinessAbhisek chudalPas encore d'évaluation

- State Bank CollectDocument3 pagesState Bank CollectKartik PrajapatiPas encore d'évaluation

- Review Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Document11 pagesReview Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Ulaş GüllenoğluPas encore d'évaluation

- 1604 CFDocument8 pages1604 CFNette CutinPas encore d'évaluation

- Corporate Taxation & Financial PlanningDocument29 pagesCorporate Taxation & Financial PlanningMonalisa BagdePas encore d'évaluation

- ICAN NoticeDocument1 pageICAN NoticehawaPas encore d'évaluation

- Cfs 9268 MDocument1 pageCfs 9268 Mdavidigoro26Pas encore d'évaluation

- Boat Storm Pro Smartwatch 1.68" Amoled Screen Display With Cloud FacesDocument1 pageBoat Storm Pro Smartwatch 1.68" Amoled Screen Display With Cloud Facesentertainment king0% (2)

- Pas 12 Income Taxes FinalDocument17 pagesPas 12 Income Taxes FinalKeycie Ann ArevaloPas encore d'évaluation

- CIR v. BCDADocument2 pagesCIR v. BCDAChariPas encore d'évaluation

- Capital Gains - An Overview: Ca Ameet PatelDocument51 pagesCapital Gains - An Overview: Ca Ameet PatelPrasun TiwariPas encore d'évaluation

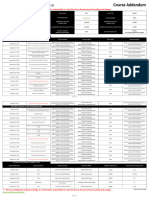

- Fall 2023 ACC400 NKK Course AddendumDocument2 pagesFall 2023 ACC400 NKK Course AddendumGKPas encore d'évaluation

- Zuellig Vs CIRDocument36 pagesZuellig Vs CIRMagenic Manila IncPas encore d'évaluation

- Dispute Transaction FormDocument1 pageDispute Transaction FormAli Naeem SheikhPas encore d'évaluation

- Cgi DD XML MappingDocument3 pagesCgi DD XML MappingRajendra PilludaPas encore d'évaluation

- Payslip of Jun-22Document1 pagePayslip of Jun-22Rohit VenisettyPas encore d'évaluation

- Bob StatementDocument18 pagesBob StatementShreya AgrawalPas encore d'évaluation

- BSNL Wishes All Its Esteemed Customers A Very Happy and Safe DiwaliDocument3 pagesBSNL Wishes All Its Esteemed Customers A Very Happy and Safe DiwaliFiroz ShaikhPas encore d'évaluation

- BIR Ruling 98-97Document1 pageBIR Ruling 98-97Kenneth BuriPas encore d'évaluation

- Module 07 - Overview of Regular Income TaxationDocument32 pagesModule 07 - Overview of Regular Income TaxationTrixie OnglaoPas encore d'évaluation

- System TcodeDocument2 pagesSystem TcodeHridya PrasadPas encore d'évaluation

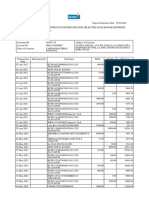

- OD225544536120314000Document2 pagesOD225544536120314000The AnonymousPas encore d'évaluation

- AAETA0890J - Order Us 80G - 1019180029Document2 pagesAAETA0890J - Order Us 80G - 1019180029Donor CrewPas encore d'évaluation

- Acct Statement - XX9414 - 03102023Document20 pagesAcct Statement - XX9414 - 03102023Saravana RajPas encore d'évaluation

- Jawaban Perhitungan Dan Akumulasi BiayaDocument7 pagesJawaban Perhitungan Dan Akumulasi BiayaEka OematanPas encore d'évaluation