Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Kevin Cope Seeing The Big PictureDocument350 pagesKevin Cope Seeing The Big Pictureadnan80% (5)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Agricultures Connected Future How Technology Can Yield New Growth FDocument10 pagesAgricultures Connected Future How Technology Can Yield New Growth Fgeopan88100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Akmen Chapter 12 (Putri Ramadhani)Document22 pagesAkmen Chapter 12 (Putri Ramadhani)Putri RamadhaniPas encore d'évaluation

- Exercise 18Document9 pagesExercise 18raihan aqilPas encore d'évaluation

- Tax 101 PDFDocument11 pagesTax 101 PDFEmerson Peralta0% (2)

- Samsung Financial Performance PresentationDocument28 pagesSamsung Financial Performance PresentationMazed100% (1)

- Marasigan TransactionDocument20 pagesMarasigan TransactionE.D.J100% (2)

- Case 1.4Document4 pagesCase 1.4Nam Hong Joo88% (8)

- Business Planning Tools - Customer AnalysisDocument16 pagesBusiness Planning Tools - Customer Analysisgeopan88Pas encore d'évaluation

- Silvano Group 2017Document64 pagesSilvano Group 2017geopan88Pas encore d'évaluation

- Contents Tool 7: Your ResourcesDocument19 pagesContents Tool 7: Your Resourcesgeopan88Pas encore d'évaluation

- Presentation Pharma EngDocument40 pagesPresentation Pharma Enggeopan88Pas encore d'évaluation

- Contents Tool 6: Your Business EnvironmentDocument14 pagesContents Tool 6: Your Business Environmentgeopan88Pas encore d'évaluation

- Contents Tool 8: Strategy FormulationDocument10 pagesContents Tool 8: Strategy Formulationgeopan88Pas encore d'évaluation

- Smart Learning PublishingDocument31 pagesSmart Learning Publishinggeopan88Pas encore d'évaluation

- Grow Sme GuideDocument24 pagesGrow Sme Guidegeopan88Pas encore d'évaluation

- Biz Planning For Success 2005Document124 pagesBiz Planning For Success 2005geopan88Pas encore d'évaluation

- Russian and Ukrainian Fast Food Industry OverviewDocument8 pagesRussian and Ukrainian Fast Food Industry Overviewgeopan88Pas encore d'évaluation

- Investment in GermanyDocument228 pagesInvestment in Germanygeopan88Pas encore d'évaluation

- How - Much Does Industry Matter-RumeltDocument12 pagesHow - Much Does Industry Matter-Rumeltgeopan88Pas encore d'évaluation

- Book Market in Greece-2011Document12 pagesBook Market in Greece-2011geopan88Pas encore d'évaluation

- A Window of Opportunity For Europe Full ReportDocument64 pagesA Window of Opportunity For Europe Full ReportmunshikdPas encore d'évaluation

- Avangardco Ipl Annual Report 2013Document65 pagesAvangardco Ipl Annual Report 2013geopan88Pas encore d'évaluation

- FinalmrpDocument153 pagesFinalmrpAmbresh Pratap SinghPas encore d'évaluation

- Lesson 1: Nature, Purpose, and Scope of Financial Management Learning ObjectivesDocument6 pagesLesson 1: Nature, Purpose, and Scope of Financial Management Learning ObjectivesAngelyn MortelPas encore d'évaluation

- Sept 2021 Insight PartiiDocument133 pagesSept 2021 Insight Partiirowan betPas encore d'évaluation

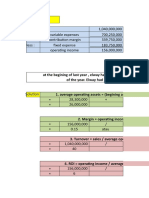

- Accounting For CSR Transactions - 22-10-2022Document14 pagesAccounting For CSR Transactions - 22-10-2022maharshPas encore d'évaluation

- BSBFIM601 Assessment 1: Sales and Profit BudgetsDocument8 pagesBSBFIM601 Assessment 1: Sales and Profit Budgetsprasannareddy9989100% (1)

- Trend AnalysisDocument4 pagesTrend AnalysisKha DijaPas encore d'évaluation

- Session 1 Financial Accounting Infor Manju JaiswallDocument41 pagesSession 1 Financial Accounting Infor Manju JaiswallpremoshinPas encore d'évaluation

- Financial Statement Analysis (Pepsi)Document9 pagesFinancial Statement Analysis (Pepsi)che gatelaPas encore d'évaluation

- DLF - IciciDocument55 pagesDLF - IciciYatendra AdireddyPas encore d'évaluation

- Taxes Deadline For Filing Prescribed BIR Forms Place of Filing and Payment Income Tax - IndividualDocument3 pagesTaxes Deadline For Filing Prescribed BIR Forms Place of Filing and Payment Income Tax - IndividualIsabella Gimao100% (1)

- Deloitte Vietnam - Tax Newsletter - May 2019Document27 pagesDeloitte Vietnam - Tax Newsletter - May 2019Nguyen Hoang ThoPas encore d'évaluation

- UTS TA Chapter 4 FIX by Hafidz & FitriaDocument17 pagesUTS TA Chapter 4 FIX by Hafidz & FitriaApriana RahmawatiPas encore d'évaluation

- Pasta Manufacturer Business PlanDocument29 pagesPasta Manufacturer Business PlanMARY GRACE TORALLO BINLAYOPas encore d'évaluation

- CH 5Document13 pagesCH 5rhggPas encore d'évaluation

- Excel Practice SheetDocument154 pagesExcel Practice SheetAndrew KohPas encore d'évaluation

- Far460 Group Project 2Document4 pagesFar460 Group Project 2NURAMIRA AQILAPas encore d'évaluation

- ACC 557 Week 2, QuizDocument3 pagesACC 557 Week 2, QuizacurashahPas encore d'évaluation

- Uniform CPA Examination. Questions and Unofficial Answers 1991 NDocument100 pagesUniform CPA Examination. Questions and Unofficial Answers 1991 NAbdifatah AbdilahiPas encore d'évaluation

- Session 6-Enredamev5 PDFDocument9 pagesSession 6-Enredamev5 PDFLaura GómezPas encore d'évaluation

- Intermediate Accounting: Reporting Financial PerformanceDocument45 pagesIntermediate Accounting: Reporting Financial PerformancenasduioahwaPas encore d'évaluation

- Flexible Budget ExampleDocument2 pagesFlexible Budget Examplebrenica_2000Pas encore d'évaluation

- Balrampur Chini Mills Limited.: Analysis of Annual Report OFDocument9 pagesBalrampur Chini Mills Limited.: Analysis of Annual Report OFBloomy devasiaPas encore d'évaluation

- Chapter 14 - Answer PDFDocument18 pagesChapter 14 - Answer PDFAldrin ZlmdPas encore d'évaluation