Vous aimerez peut-être aussi

- Monetary Policy - IndicatorsDocument4 pagesMonetary Policy - IndicatorsGJ RamPas encore d'évaluation

- Monetary Policy of IndiaDocument5 pagesMonetary Policy of IndiaSudesh SharmaPas encore d'évaluation

- Rbi Monetary PolicyDocument5 pagesRbi Monetary PolicyRohit GuptaPas encore d'évaluation

- Monetary Policy of India - WikipediaDocument4 pagesMonetary Policy of India - Wikipediaambikesh008Pas encore d'évaluation

- Monetary Policy ReviewsDocument6 pagesMonetary Policy ReviewspundirsandeepPas encore d'évaluation

- Monetary PolicyDocument3 pagesMonetary PolicymbapritiPas encore d'évaluation

- Monetary PolicyDocument39 pagesMonetary PolicyTirupal PuliPas encore d'évaluation

- What Is Monetary PolicyDocument5 pagesWhat Is Monetary PolicyBhagat DeepakPas encore d'évaluation

- Monetary PolicyDocument9 pagesMonetary Policytulasi nandamuriPas encore d'évaluation

- Financial Management Report: On "Repo Rate and Impact On GDP"Document10 pagesFinancial Management Report: On "Repo Rate and Impact On GDP"Anjali BhatiaPas encore d'évaluation

- Credit Authorisation SchemeDocument6 pagesCredit Authorisation SchemeOngwang KonyakPas encore d'évaluation

- Monetary Policy NotesDocument13 pagesMonetary Policy NotesMehak joshiPas encore d'évaluation

- Monetary Policy Is of Two KindsDocument16 pagesMonetary Policy Is of Two KindsSainath SindhePas encore d'évaluation

- Credit ControlDocument5 pagesCredit ControlHimanshu GargPas encore d'évaluation

- Indian Monetary Policy Analysis (2010-2017)Document38 pagesIndian Monetary Policy Analysis (2010-2017)Parang Mehta95% (21)

- Monetary Policy of IndiaDocument6 pagesMonetary Policy of IndiaKushal PatilPas encore d'évaluation

- Credit Control in India - WikipediaDocument20 pagesCredit Control in India - WikipediapranjaliPas encore d'évaluation

- Monetary PolicyDocument18 pagesMonetary PolicySarada NagPas encore d'évaluation

- Central Bank & Monetary Policy - 1Document30 pagesCentral Bank & Monetary Policy - 1Dr.Ashok Kumar PanigrahiPas encore d'évaluation

- Research Paper On Monetary Policy of RbiDocument6 pagesResearch Paper On Monetary Policy of Rbiaflbtjglu100% (1)

- KP IifsDocument15 pagesKP IifsKalyani PranjalPas encore d'évaluation

- Monetary Policy Initiatives Since 2008-09 and Its Effectiveness in Containing Inflation"Document31 pagesMonetary Policy Initiatives Since 2008-09 and Its Effectiveness in Containing Inflation"Arpit PangasaPas encore d'évaluation

- Monetary Policy and Its Instruments: DefinitionDocument11 pagesMonetary Policy and Its Instruments: Definitionamandeep singhPas encore d'évaluation

- Banking Sector in India: Sr. No. Title Page NoDocument15 pagesBanking Sector in India: Sr. No. Title Page NorohanPas encore d'évaluation

- Monetary Policy of IndiaDocument6 pagesMonetary Policy of IndiaSOURAV SAMALPas encore d'évaluation

- Monetary Policy Monetary Policy DefinedDocument9 pagesMonetary Policy Monetary Policy DefinedXyz YxzPas encore d'évaluation

- RBI Credit Control in IndiaDocument11 pagesRBI Credit Control in IndiaDeepjyotiPas encore d'évaluation

- Monetary Policy in IndiaDocument8 pagesMonetary Policy in Indiaamitwaghela50Pas encore d'évaluation

- Macro Economics: Monetary & Fiscal Policy InstrumentsDocument27 pagesMacro Economics: Monetary & Fiscal Policy InstrumentsACRPas encore d'évaluation

- Monetary and Credit Policy: Asymmetric InformationDocument4 pagesMonetary and Credit Policy: Asymmetric Informationnikhil6710349Pas encore d'évaluation

- Top of FormDocument14 pagesTop of Formprnjlgoswami86Pas encore d'évaluation

- Monetary PolicyDocument23 pagesMonetary PolicyManjunath ShettigarPas encore d'évaluation

- Monetary PolicyDocument18 pagesMonetary PolicyTanmay JainPas encore d'évaluation

- Fiscal and Monetary PolicyDocument17 pagesFiscal and Monetary Policyrajan tiwariPas encore d'évaluation

- CETKing Study3 Report RBI S Monetary PolicyDocument8 pagesCETKing Study3 Report RBI S Monetary PolicyVaishnavi ParthasarathyPas encore d'évaluation

- 1.1 Monetary PolicyDocument77 pages1.1 Monetary PolicyS SrinivasanPas encore d'évaluation

- 9 1Document17 pages9 1VikasRoshanPas encore d'évaluation

- (A) Quantitative Instruments or General ToolsDocument5 pages(A) Quantitative Instruments or General ToolsSiddh Shah ⎝⎝⏠⏝⏠⎠⎠Pas encore d'évaluation

- Monetary Policy:: InflationDocument3 pagesMonetary Policy:: InflationSumit SethiPas encore d'évaluation

- Submitted By-Arpita Shukla Sec ADocument18 pagesSubmitted By-Arpita Shukla Sec AAshish ShuklaPas encore d'évaluation

- Monetary PolicyDocument10 pagesMonetary PolicyPRAKHAR KAUSHIKPas encore d'évaluation

- RBI Credit PolicyDocument1 pageRBI Credit Policysangya01Pas encore d'évaluation

- Ibe - Unit-3Document37 pagesIbe - Unit-3Pranav YeleswarapuPas encore d'évaluation

- Monetary Policy: Affiliated To Devi Ahilya Vishwavidyalaya, IndoreDocument14 pagesMonetary Policy: Affiliated To Devi Ahilya Vishwavidyalaya, IndoreSudheer VishwakarmaPas encore d'évaluation

- Latest Policy RatesDocument3 pagesLatest Policy RatesAbhishek BidhanPas encore d'évaluation

- Monetary Policy of IndiaDocument34 pagesMonetary Policy of IndiaJhankar MishraPas encore d'évaluation

- Fiscal and Monetary PolicyDocument17 pagesFiscal and Monetary PolicySuresh Sen100% (1)

- Main Functions Financial SupervisionDocument9 pagesMain Functions Financial SupervisionAjay MykalPas encore d'évaluation

- Financial Sector Reforms in India Since 1991Document11 pagesFinancial Sector Reforms in India Since 1991AMAN KUMAR SINGHPas encore d'évaluation

- Monetary Policy - Eco ProjectDocument8 pagesMonetary Policy - Eco Projectnandanaa06Pas encore d'évaluation

- Financial Institutions and Markets ProjectDocument10 pagesFinancial Institutions and Markets ProjectPallavi AgrawallaPas encore d'évaluation

- Economics Banking ProjectDocument15 pagesEconomics Banking ProjectCJKPas encore d'évaluation

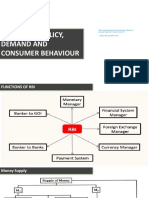

- Monetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreDocument23 pagesMonetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreBhavya NarangPas encore d'évaluation

- Explain Various Quantitative Instruments of Monetary Policy Which Are Undertaken To Control InflationDocument4 pagesExplain Various Quantitative Instruments of Monetary Policy Which Are Undertaken To Control Inflationanvesha khillarPas encore d'évaluation

- Central BankingDocument28 pagesCentral Bankingneha16septPas encore d'évaluation

- Why Interest Rates ChangeDocument4 pagesWhy Interest Rates Changekirang gandhiPas encore d'évaluation

- Role of RBI in Indian EconomyDocument4 pagesRole of RBI in Indian EconomySubhashit SinghPas encore d'évaluation

- L-33 & 34, Fiscal Policy and Monetary PolicyDocument25 pagesL-33 & 34, Fiscal Policy and Monetary PolicyDhruv MinochaPas encore d'évaluation

- Monetary Policy. Minnor Project BBA Banking and Insurance Minnor ProjectDocument65 pagesMonetary Policy. Minnor Project BBA Banking and Insurance Minnor ProjecttanpreetjaggiPas encore d'évaluation

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)D'EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Pas encore d'évaluation

- My ProjectDocument159 pagesMy ProjectVijay KumarPas encore d'évaluation

- RBI Advisory NBFC Enterslice V1-M27Document4 pagesRBI Advisory NBFC Enterslice V1-M27Narendra KumarPas encore d'évaluation

- Debentures Information Memorandum 300 Crore PDFDocument62 pagesDebentures Information Memorandum 300 Crore PDFSmith SivaPas encore d'évaluation

- Universal Banks in IndiaDocument33 pagesUniversal Banks in Indianamita patharkarPas encore d'évaluation

- Bad Bank Is Actually A Good Idea: S. Prasanth, Dr. S.SudhamathiDocument4 pagesBad Bank Is Actually A Good Idea: S. Prasanth, Dr. S.SudhamathiSARVESH RPas encore d'évaluation

- Comparative Study of The Public Sector Amp Private Sector BankDocument73 pagesComparative Study of The Public Sector Amp Private Sector BanksumanPas encore d'évaluation

- Financial Services AssignmentDocument18 pagesFinancial Services Assignmentshiv mehraPas encore d'évaluation

- A Role of Foreign Banks in IndiaDocument6 pagesA Role of Foreign Banks in Indiaalishasoni100% (1)

- Regulatory Framework of Mutual FundsDocument24 pagesRegulatory Framework of Mutual FundsLovepreet NegiPas encore d'évaluation

- HCBL Directors Report 2013-2014 PDFDocument8 pagesHCBL Directors Report 2013-2014 PDF05550Pas encore d'évaluation

- Vohf EQdkx SJ S1 e PDocument14 pagesVohf EQdkx SJ S1 e PAarti ThdfcPas encore d'évaluation

- 10 Chapter2Document30 pages10 Chapter2ashishPas encore d'évaluation

- Agriculture Finance in India - Issues & Future Perspectives: Haresh Barot & Kundan PatelDocument6 pagesAgriculture Finance in India - Issues & Future Perspectives: Haresh Barot & Kundan PatelharpominderPas encore d'évaluation

- Financial Awareness EBook PDFDocument54 pagesFinancial Awareness EBook PDFJayendra GuptaPas encore d'évaluation

- 0102164625advance FEMA RBI Queries PDFDocument28 pages0102164625advance FEMA RBI Queries PDFChintz MehtaPas encore d'évaluation

- Industrial Finance Corporation of India (IFCI) : The Industrial Finance Corporation of India (IFCI) WasDocument4 pagesIndustrial Finance Corporation of India (IFCI) : The Industrial Finance Corporation of India (IFCI) Wasmedha jaiwantPas encore d'évaluation

- Financial Inclusion in IndiaDocument38 pagesFinancial Inclusion in IndiaKusPas encore d'évaluation

- OMLP2P Loan - Peer To Peer Lending India - Online Money LendingDocument6 pagesOMLP2P Loan - Peer To Peer Lending India - Online Money LendingOMLP2P.comPas encore d'évaluation

- FIBA304 Introduction To Indian Financial SystemDocument14 pagesFIBA304 Introduction To Indian Financial SystemAk KalakotiPas encore d'évaluation

- Security ManualDocument117 pagesSecurity ManualNirmal Agarwala100% (2)

- FM M1 22mba22Document29 pagesFM M1 22mba22ARUN KUMARPas encore d'évaluation

- Merchant BankingDocument55 pagesMerchant Bankingsuhaspatel84Pas encore d'évaluation

- Monetary Policy of Last 5 YearsDocument28 pagesMonetary Policy of Last 5 YearsPiyush ChitlangiaPas encore d'évaluation

- A Major Project Report: Master of Business AdministrationDocument71 pagesA Major Project Report: Master of Business AdministrationAYUSH JOSHIPas encore d'évaluation

- Indian EconomyDocument12 pagesIndian EconomyArnab BosePas encore d'évaluation

- MonthlyCurrentAffairsGKDigest June2019 CoverDocument84 pagesMonthlyCurrentAffairsGKDigest June2019 CoverSai Mahesh ChaturvedulaPas encore d'évaluation

- Karnataka Bank ProjectDocument72 pagesKarnataka Bank ProjectBalaji70% (10)

- RBI Master CircularDocument42 pagesRBI Master CircularDeep Singh PariharPas encore d'évaluation

- Monthly Digest July 2021 Eng 54Document34 pagesMonthly Digest July 2021 Eng 54Max MahonePas encore d'évaluation

- RBI Grade B Part 2 Capsule File 2023Document46 pagesRBI Grade B Part 2 Capsule File 2023Ravi AgarwalPas encore d'évaluation