Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- An Explanation of Miller IndicesDocument9 pagesAn Explanation of Miller IndicesSesan FesobiPas encore d'évaluation

- What's The Difference Between A Merozoite, Trophozoite, Sporozoite, and ShizontDocument1 pageWhat's The Difference Between A Merozoite, Trophozoite, Sporozoite, and ShizontSesan Fesobi100% (3)

- Full Text of President Jonathan's Nationwide Broadcast!!!Document3 pagesFull Text of President Jonathan's Nationwide Broadcast!!!Sesan FesobiPas encore d'évaluation

- Product Life Cycle ManagementDocument26 pagesProduct Life Cycle Managementnarasimha_gudiPas encore d'évaluation

- 6 Messages To The ChurchDocument5 pages6 Messages To The ChurchEyemanProphetPas encore d'évaluation

- Understanding MSG-3: by Charlotte Adams, Contributing EditorDocument9 pagesUnderstanding MSG-3: by Charlotte Adams, Contributing EditorSesan Fesobi100% (2)

- Don Moen - Grace Is EnoughDocument2 pagesDon Moen - Grace Is EnoughSesan FesobiPas encore d'évaluation

- Winning Your Personal War Against SatanDocument1 pageWinning Your Personal War Against SatanSesan FesobiPas encore d'évaluation

- Don Moen - Grace Is EnoughDocument2 pagesDon Moen - Grace Is EnoughSesan FesobiPas encore d'évaluation

- Nigeria - The 2012 Failed States Index and Nation-BuildingDocument2 pagesNigeria - The 2012 Failed States Index and Nation-BuildingSesan FesobiPas encore d'évaluation

- President Obama's Speech in RamallahDocument3 pagesPresident Obama's Speech in RamallahSesan FesobiPas encore d'évaluation

- Air PowerDocument32 pagesAir PowerSesan Fesobi0% (1)

- President Obama's Speech To Israelis in JerusalemDocument10 pagesPresident Obama's Speech To Israelis in JerusalemSesan FesobiPas encore d'évaluation

- National Economic Empowerment and Development Strategy (NEEDS) - Adekunlke Ajasin UniversityDocument17 pagesNational Economic Empowerment and Development Strategy (NEEDS) - Adekunlke Ajasin UniversitySesan FesobiPas encore d'évaluation

- ABC of Jonathan's Transformation AgendaDocument6 pagesABC of Jonathan's Transformation AgendaSesan FesobiPas encore d'évaluation

- Emerging Threats To National Security (Feb 2005)Document14 pagesEmerging Threats To National Security (Feb 2005)Sesan FesobiPas encore d'évaluation

- Half-Year Economics Indices 2012-1Document1 pageHalf-Year Economics Indices 2012-1Sesan FesobiPas encore d'évaluation

- Distinguishing Space Power From Air PowerDocument63 pagesDistinguishing Space Power From Air PowerSesan FesobiPas encore d'évaluation

- Succession Planning and Career Pathing ProcedureDocument10 pagesSuccession Planning and Career Pathing ProcedureSesan FesobiPas encore d'évaluation

- African Union - PartnershipsDocument9 pagesAfrican Union - PartnershipsSesan FesobiPas encore d'évaluation

- Colombian ConflictDocument15 pagesColombian ConflictSesan FesobiPas encore d'évaluation

- Syrian Civil WarDocument40 pagesSyrian Civil WarSesan FesobiPas encore d'évaluation

- African Union - PartnershipsDocument9 pagesAfrican Union - PartnershipsSesan FesobiPas encore d'évaluation

- African Nuclear Weapon Free Zone Treaty (ANWFZT)Document13 pagesAfrican Nuclear Weapon Free Zone Treaty (ANWFZT)Sesan FesobiPas encore d'évaluation

- 1999 Toyota Camry Fuel DataDocument3 pages1999 Toyota Camry Fuel DataSesan FesobiPas encore d'évaluation

- SP Tool A Succession Planning Intro and Implementation PlanDocument11 pagesSP Tool A Succession Planning Intro and Implementation PlanSesan FesobiPas encore d'évaluation

- Supercharger: From Wikipedia, The Free EncyclopediaDocument12 pagesSupercharger: From Wikipedia, The Free EncyclopediaSesan FesobiPas encore d'évaluation

- Technical Service Bulletin: M.I.L. On" 1Mz-Fe Engine Misfire DTC P0300, P0301, P0302, P0303, P0304, P0305 OR P0306Document3 pagesTechnical Service Bulletin: M.I.L. On" 1Mz-Fe Engine Misfire DTC P0300, P0301, P0302, P0303, P0304, P0305 OR P0306Sesan Fesobi100% (1)

- Transmission MechanicsDocument10 pagesTransmission MechanicsSesan FesobiPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Fundamental Freedom To Trade by Edward L. HudginsDocument9 pagesThe Fundamental Freedom To Trade by Edward L. HudginsmirunelutuPas encore d'évaluation

- Inco 2000Document21 pagesInco 2000Prakash Gyan SinghPas encore d'évaluation

- Presentation On Export CreditDocument21 pagesPresentation On Export CreditArpit KhandelwalPas encore d'évaluation

- Strategic Trade Act Frequently Asked QuestionsDocument6 pagesStrategic Trade Act Frequently Asked QuestionsVicky FanPas encore d'évaluation

- Indonesia Historical TimelineDocument2 pagesIndonesia Historical Timelinenangkarak8201Pas encore d'évaluation

- Case 4 - Potato Market in ThailandDocument15 pagesCase 4 - Potato Market in ThailandCharmyne De Vera Sanglay0% (1)

- Unit 1Document41 pagesUnit 1hardy1997Pas encore d'évaluation

- World: Ferro-Manganese - Market Report. Analysis and Forecast To 2020Document7 pagesWorld: Ferro-Manganese - Market Report. Analysis and Forecast To 2020IndexBox MarketingPas encore d'évaluation

- Haïti - Économie - Tout Savoir Sur Les Flux Commerciaux Entre Haïti Et La République DominicaineDocument82 pagesHaïti - Économie - Tout Savoir Sur Les Flux Commerciaux Entre Haïti Et La République DominicaineDaniel Daréus100% (1)

- Djoko The Indonesian Mineral Mining Sector Prospects and ChallengesDocument42 pagesDjoko The Indonesian Mineral Mining Sector Prospects and ChallengesUmesh ShanmugamPas encore d'évaluation

- Oct2011 Leather and Leather ProductsDocument12 pagesOct2011 Leather and Leather ProductsArif RamadhanPas encore d'évaluation

- Steel Price HistoryDocument17 pagesSteel Price HistoryPierluigiBusettoPas encore d'évaluation

- Renewable Energy KoreaDocument7 pagesRenewable Energy Koreashantanu91Pas encore d'évaluation

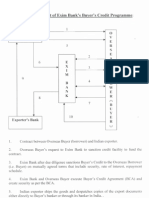

- Procedural Flow Chart of Exim BankDocument3 pagesProcedural Flow Chart of Exim BankMilan DasPas encore d'évaluation

- IndianDocument16 pagesIndianArun ThakurPas encore d'évaluation

- Short Term Report ON Jeera (Cumin Seed: Indiabulls Commodities LimitedDocument10 pagesShort Term Report ON Jeera (Cumin Seed: Indiabulls Commodities LimitedrahulvaliyaPas encore d'évaluation

- Transfer Chute For Bulk MaterialDocument131 pagesTransfer Chute For Bulk Materialmishra_1982100% (8)

- 1 Jbec AlejoDocument145 pages1 Jbec AlejoFr JPas encore d'évaluation

- DLMM04 Week 4Micro-Lecture. 4.3 Protectionist Trading Policy and Optimal TariffsDocument5 pagesDLMM04 Week 4Micro-Lecture. 4.3 Protectionist Trading Policy and Optimal TariffsmuhammadPas encore d'évaluation

- Introducing Electric Sheep Shearing Machines To Nepalese FarmsDocument13 pagesIntroducing Electric Sheep Shearing Machines To Nepalese Farmsapi-341099662Pas encore d'évaluation

- Exporting SpicesDocument15 pagesExporting SpicesRohit PadalkarPas encore d'évaluation

- Progress and Potential of Mango Pulp Industry in India: P. A. Lakshmi Prasanna Sant KumarDocument26 pagesProgress and Potential of Mango Pulp Industry in India: P. A. Lakshmi Prasanna Sant KumarKashmira SawantPas encore d'évaluation

- Inplant Training Report at KAMDHENUDocument51 pagesInplant Training Report at KAMDHENUAlbert ThomasPas encore d'évaluation

- Dock ReceiptDocument2 pagesDock ReceiptKarriem WakkiluddinPas encore d'évaluation

- Export and Import Clearance Procedures and DocumentationDocument38 pagesExport and Import Clearance Procedures and DocumentationAJESH100% (10)

- Exim ProspectusDocument4 pagesExim ProspectusArup ChakrabortyPas encore d'évaluation

- A Project Study Report On Marketing Strategy of JK Tyre LimitedDocument11 pagesA Project Study Report On Marketing Strategy of JK Tyre LimitedthexxxanasPas encore d'évaluation

- (REV) Partial Scope Agreement Brazil-Guyana (English)Document14 pages(REV) Partial Scope Agreement Brazil-Guyana (English)candykisses100% (1)

- Richards Bay Coal Terminal - An OverviewDocument21 pagesRichards Bay Coal Terminal - An OverviewhoneybibayPas encore d'évaluation

- Cocoa Study - enDocument76 pagesCocoa Study - enMonica Bîldea100% (2)