Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Aptitude Tests For EmploymentDocument29 pagesAptitude Tests For EmploymentVelayudham ThiyagarajanPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Icai Differences Between Ifrss and Ind AsDocument21 pagesIcai Differences Between Ifrss and Ind AsdhuvadpratikPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Psychometric Tests PDFDocument7 pagesPsychometric Tests PDFMarshall MahachiPas encore d'évaluation

- Project ReportDocument9 pagesProject ReportVelayudham ThiyagarajanPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Custom Duty CalculetorDocument2 pagesCustom Duty CalculetorVelayudham ThiyagarajanPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Balance Sheet As Per New Schedule ViDocument11 pagesBalance Sheet As Per New Schedule ViVelayudham ThiyagarajanPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Academics: o o o o o o oDocument4 pagesAcademics: o o o o o o oVelayudham ThiyagarajanPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- MM+T+Codes SAPDocument4 pagesMM+T+Codes SAPVelayudham ThiyagarajanPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Keys Combination Functions Control CombinationsDocument8 pagesKeys Combination Functions Control CombinationsVelayudham ThiyagarajanPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Tax Touch Up: Which Is That Amt DepositedDocument5 pagesTax Touch Up: Which Is That Amt DepositedVelayudham ThiyagarajanPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- ATC Enrolment Fee Structure ICAIDocument4 pagesATC Enrolment Fee Structure ICAIVelayudham ThiyagarajanPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- End User Guide To Accounts Receivable in Sap FiDocument82 pagesEnd User Guide To Accounts Receivable in Sap FiVelayudham ThiyagarajanPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Rippling Metrics RedactedDocument17 pagesRippling Metrics RedactedScott GalvinPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Info 620 Exam 2 Study Guide PDFDocument4 pagesInfo 620 Exam 2 Study Guide PDFюрий локтионовPas encore d'évaluation

- Mobile Detailer Business PlanDocument16 pagesMobile Detailer Business PlanTaisa StocksPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- AssignmentDocument5 pagesAssignmentpeter chadaPas encore d'évaluation

- Merchandising Calender: By: Harsha Siddham Sanghamitra Kalita Sayantani SahaDocument29 pagesMerchandising Calender: By: Harsha Siddham Sanghamitra Kalita Sayantani SahaSanghamitra KalitaPas encore d'évaluation

- Branch Accounts Theory and Problems PDFDocument18 pagesBranch Accounts Theory and Problems PDFketanPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Cereal Partners WorldwideDocument13 pagesCereal Partners WorldwideBeamlakPas encore d'évaluation

- E. Patrick Assignment 4.1Document3 pagesE. Patrick Assignment 4.1Alex100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Partnership Questions Problems With Answers PDF FreeDocument11 pagesPartnership Questions Problems With Answers PDF FreeJoseph AsisPas encore d'évaluation

- Group 6 - Transforming Luxury Distribution in AsiaDocument5 pagesGroup 6 - Transforming Luxury Distribution in AsiaAnsh LakhmaniPas encore d'évaluation

- Lesson 2 - Branches of AccountingDocument15 pagesLesson 2 - Branches of AccountingLeizzamar BayadogPas encore d'évaluation

- MAS 25A 27TH BATCH With AnswersDocument12 pagesMAS 25A 27TH BATCH With AnswersSarah Jane GanigaPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Chapter 5Document36 pagesChapter 5Baby KhorPas encore d'évaluation

- Definition of GaapDocument2 pagesDefinition of GaapAshwini PrabhakaranPas encore d'évaluation

- Activity Based Costing and Lean AccountingDocument91 pagesActivity Based Costing and Lean AccountingAira Nharie MecatePas encore d'évaluation

- CH4 - Job Order Costing and Overheads ApplicationDocument51 pagesCH4 - Job Order Costing and Overheads ApplicationYMPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Lean Chapter 2Document14 pagesLean Chapter 2WinterMist11Pas encore d'évaluation

- Quiz Quiz 2 Single Entry and Cash Accrual Accounting PDFDocument28 pagesQuiz Quiz 2 Single Entry and Cash Accrual Accounting PDFluismorentePas encore d'évaluation

- Chapter - 32: Corporate Restructuring, Mergers and AcquisitionsDocument26 pagesChapter - 32: Corporate Restructuring, Mergers and AcquisitionsHardeep sagarPas encore d'évaluation

- Introduction To Marketing Management MNM1503Document27 pagesIntroduction To Marketing Management MNM1503Melissa0% (1)

- 59 IpcccostingDocument5 pages59 Ipcccostingapi-206947225Pas encore d'évaluation

- TB 14Document67 pagesTB 14Dang ThanhPas encore d'évaluation

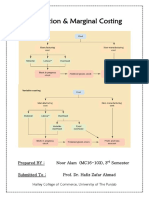

- Absorption & Marginal Costing - Noor Alam (MC16-103)Document24 pagesAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Brand Positioning Refers To "Target Consumer's" Reason To Buy Your Brand in Preference To Others. It IsDocument11 pagesBrand Positioning Refers To "Target Consumer's" Reason To Buy Your Brand in Preference To Others. It IsAndrew BrownPas encore d'évaluation

- DocDocument45 pagesDocYogesh KatnaPas encore d'évaluation

- Lembar KerjaDocument29 pagesLembar Kerjakholisatunnisa530Pas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Profit and Loss - 21TDY 659Document47 pagesProfit and Loss - 21TDY 659aakash rayPas encore d'évaluation

- Business Strategy of The E-Type Company PDFDocument2 pagesBusiness Strategy of The E-Type Company PDFHadeer KamelPas encore d'évaluation

- Instant Download Ebook PDF Fundamental Accounting Principles Volume 1 16th Canadian Edition PDF ScribdDocument42 pagesInstant Download Ebook PDF Fundamental Accounting Principles Volume 1 16th Canadian Edition PDF Scribdjudi.hawkins744100% (40)

- Financial Statement Analysis and Security Valuation 5th Edition by Penman ISBN Test BankDocument16 pagesFinancial Statement Analysis and Security Valuation 5th Edition by Penman ISBN Test Bankcindy100% (24)