Vous aimerez peut-être aussi

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Week 4 ACCT5001 Instructions For Outside-of-Class Study: Self-Study Questions Are To Be Prepared After The Week 3 SeminarDocument3 pagesWeek 4 ACCT5001 Instructions For Outside-of-Class Study: Self-Study Questions Are To Be Prepared After The Week 3 Seminarzhangsaen110Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Week 1 Self-Study: Ch. 1: Q1, Q2, Q3, E1.1 PSA1.1 (B-E), PSA1.2 (B-D) Problem Set A 1.1Document2 pagesWeek 1 Self-Study: Ch. 1: Q1, Q2, Q3, E1.1 PSA1.1 (B-E), PSA1.2 (B-D) Problem Set A 1.1zhangsaen110Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Week 2 Sem 1 2010 Instructions For Out-Of-Class StudyDocument3 pagesWeek 2 Sem 1 2010 Instructions For Out-Of-Class Studyzhangsaen110Pas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- ACCT5001 S1 2010 Week 11 Self-Study SolutionsDocument4 pagesACCT5001 S1 2010 Week 11 Self-Study Solutionszhangsaen110Pas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- ACCT5001 S1 2010 Week 8 Self-Study SolutionsDocument5 pagesACCT5001 S1 2010 Week 8 Self-Study Solutionszhangsaen110Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Lecture 5 Introduction To DirectorsDocument3 pagesLecture 5 Introduction To Directorszhangsaen110Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Lecture 8 - Meetings and Member's RightsDocument6 pagesLecture 8 - Meetings and Member's Rightszhangsaen110Pas encore d'évaluation

- Case Study On National BankDocument12 pagesCase Study On National BankMasuk HasanPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Unit 7. Audit of Property, Plant and Equipment - Handout - Final - t21516Document8 pagesUnit 7. Audit of Property, Plant and Equipment - Handout - Final - t21516mimi96Pas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Small BusinessDocument11 pagesSmall BusinessSaahil LedwaniPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Jindal Steel EIC AnalysisDocument5 pagesJindal Steel EIC AnalysisNavneet MakhariaPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Introduction of The in Duplum Rule in KenyaDocument15 pagesIntroduction of The in Duplum Rule in KenyaMacduff RonniePas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- 4dbe52c73b395 - Company Act (Dhivehi)Document26 pages4dbe52c73b395 - Company Act (Dhivehi)Mohamed MiuvaanPas encore d'évaluation

- Nature and Development of EntrepreneurshipDocument5 pagesNature and Development of Entrepreneurshiprakeshmachhi50% (8)

- Rbi 1Document27 pagesRbi 1Nishant ShahPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Gigacampus Final ReportDocument28 pagesGigacampus Final Reportmacao100Pas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Nationalized BanksDocument12 pagesNationalized BanksAakash JainPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Business Focus PearsonDocument340 pagesBusiness Focus PearsonNate100% (2)

- Pidilite IndustriesDocument7 pagesPidilite IndustriesmuralyyPas encore d'évaluation

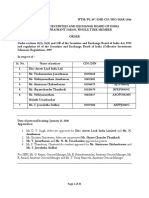

- Order in The Matter of Disc Assets Lead India LTDDocument25 pagesOrder in The Matter of Disc Assets Lead India LTDShyam SunderPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Test Bank - Chapter17 Cash FlowsDocument51 pagesTest Bank - Chapter17 Cash FlowsAiko E. Lara100% (4)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- 21 CorfinExerciseDocument21 pages21 CorfinExerciseAaryn KasoduPas encore d'évaluation

- Analyzing Investing Activities: Intercorporate InvestmentsDocument38 pagesAnalyzing Investing Activities: Intercorporate Investmentsshldhy100% (1)

- IAS OUR DREAM NOTES COMPILATION PART 3 (17 - 23rd Nov.2013)Document45 pagesIAS OUR DREAM NOTES COMPILATION PART 3 (17 - 23rd Nov.2013)Swapnil Patil50% (2)

- Main PDFDocument34 pagesMain PDFLuminati ProPas encore d'évaluation

- Market X Ls FunctionsDocument73 pagesMarket X Ls FunctionsNaresh KumarPas encore d'évaluation

- Kayelekera Mine Malawi, Southern Africa: in Production Ramp-UpDocument4 pagesKayelekera Mine Malawi, Southern Africa: in Production Ramp-UpRanken KumwendaPas encore d'évaluation

- Click Here To Download: Fin 571 Final ExamsDocument4 pagesClick Here To Download: Fin 571 Final ExamsBouzaida MaherPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- HBS CaseStudyDocument11 pagesHBS CaseStudyAmandaTranPas encore d'évaluation

- Letter of CreditDocument7 pagesLetter of CreditAnam AshfaqPas encore d'évaluation

- Maskeliya Plantations PLC and Kahawatta Plantations PLC (1199)Document22 pagesMaskeliya Plantations PLC and Kahawatta Plantations PLC (1199)Bajalock VirusPas encore d'évaluation

- India's Biggest Project Dholera ProjectDocument6 pagesIndia's Biggest Project Dholera Projectkishan prajapatiPas encore d'évaluation

- Steve SaporitoDocument22 pagesSteve SaporitorajasekharboPas encore d'évaluation

- NOTES - Banking and Financial AwarenessDocument44 pagesNOTES - Banking and Financial AwarenessAbhijeet SainiPas encore d'évaluation

- Stock Market Debacle in BangladeshDocument33 pagesStock Market Debacle in BangladeshFalguni Chowdhury100% (1)

- Investment Banking Interview Questions: Wall Street PrepDocument50 pagesInvestment Banking Interview Questions: Wall Street PrepGaripalli Aravind100% (2)

- Insurance Brokers in RomaniaDocument10 pagesInsurance Brokers in RomaniaIrina StefanaPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)