Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Indzara Personal Finance Manager 2010 v2Document8 pagesIndzara Personal Finance Manager 2010 v2AlexandruDanielPas encore d'évaluation

- Week 6 - Deduction From Gross IncomeDocument5 pagesWeek 6 - Deduction From Gross IncomeJuan FrivaldoPas encore d'évaluation

- 100 MCQ NegoDocument12 pages100 MCQ NegoDaphnePas encore d'évaluation

- Accounting NotesDocument23 pagesAccounting NotesboiroyPas encore d'évaluation

- Aml Kyc NotesDocument12 pagesAml Kyc Notesabhi_33Pas encore d'évaluation

- Application AmexDocument8 pagesApplication AmexAkash HimuPas encore d'évaluation

- Cfo 3000Document62 pagesCfo 3000SumitPas encore d'évaluation

- Insurance AwarenessDocument12 pagesInsurance Awarenessbhaskardoley30385215Pas encore d'évaluation

- CE-2023 Challan FormDocument1 pageCE-2023 Challan FormAbdul RehmanPas encore d'évaluation

- Family Roster As of 8.31.22Document12 pagesFamily Roster As of 8.31.22San Simon PantawidPas encore d'évaluation

- LIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentDocument11 pagesLIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentSaravanan DuraiPas encore d'évaluation

- Mitraguna Bsi - Bumn Promo Maret 2022Document1 pageMitraguna Bsi - Bumn Promo Maret 2022SukroPas encore d'évaluation

- SBI Investment ProductsDocument20 pagesSBI Investment ProductssaravananPas encore d'évaluation

- PNB v. Pineda G.R. No. L-46658Document4 pagesPNB v. Pineda G.R. No. L-46658Ernie GultianoPas encore d'évaluation

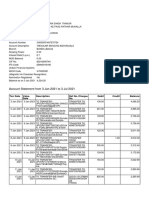

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurPas encore d'évaluation

- 72-Finman Assurance Corporation vs. Court of Appeals, 361 SCRA 514 (2001)Document7 pages72-Finman Assurance Corporation vs. Court of Appeals, 361 SCRA 514 (2001)Jopan SJPas encore d'évaluation

- 5th - Ganga - Term 1 - TM - 5-In-1Document312 pages5th - Ganga - Term 1 - TM - 5-In-1Thirumanthira YogaPas encore d'évaluation

- IIF ReportDocument152 pagesIIF ReportJuan Manuel Lopez LeonPas encore d'évaluation

- Smiths of Winterforge Rulebook 0.9Document9 pagesSmiths of Winterforge Rulebook 0.9NatsukiPLPas encore d'évaluation

- MACN-A018 Universal Affidavit of Termination of All CORPORATEDocument4 pagesMACN-A018 Universal Affidavit of Termination of All CORPORATEJabir Habib Bey33% (3)

- Ixambee Monthly December CapsuleDocument48 pagesIxambee Monthly December CapsulejoydsPas encore d'évaluation

- Ross4ppt ch19Document36 pagesRoss4ppt ch19씨나젬Pas encore d'évaluation

- Insurance Regulation, 2049 (1993) : Chapter - 1 Preliminary 1. Short Title and CommencementDocument41 pagesInsurance Regulation, 2049 (1993) : Chapter - 1 Preliminary 1. Short Title and CommencementAAnit SapkotaPas encore d'évaluation

- Vip ReceiptDocument16 pagesVip Receiptvanita kunnoPas encore d'évaluation

- Description: Tags: Top 100 Current Holders Cor Vers1Document4 pagesDescription: Tags: Top 100 Current Holders Cor Vers1anon-20972Pas encore d'évaluation

- Rbi Org in Scripts Bs Viewcontent Aspx Id 2855Document15 pagesRbi Org in Scripts Bs Viewcontent Aspx Id 2855vinjamurisivaPas encore d'évaluation

- Banking Law Assigment (Silk Bank)Document6 pagesBanking Law Assigment (Silk Bank)Muzamil AshrafPas encore d'évaluation

- MULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionDocument3 pagesMULTIPLE CHOICE. Choose The One Alternative That Best Completes The Statement or Answers The QuestionMohammad Abu LailPas encore d'évaluation

- Letter To All Member Banks of SLBC (UP)Document1 pageLetter To All Member Banks of SLBC (UP)dadan vishwakarmaPas encore d'évaluation

- Kantox FX Guide For CFODocument20 pagesKantox FX Guide For CFOfcatalaoPas encore d'évaluation