Vous aimerez peut-être aussi

- CASO Pantry ShopperDocument2 pagesCASO Pantry ShopperDiana0% (1)

- Income Statement - ProblemsDocument19 pagesIncome Statement - ProblemsIris Mnemosyne50% (2)

- Electrolux Case StudyDocument4 pagesElectrolux Case StudyEmily GevaertsPas encore d'évaluation

- Model Residential Construction Contract Cost Plus Version 910Document30 pagesModel Residential Construction Contract Cost Plus Version 910Hadi Prakoso100% (2)

- Chapters-1-10-Exam-Problem (2) Answer JessaDocument6 pagesChapters-1-10-Exam-Problem (2) Answer JessaLynssej BarbonPas encore d'évaluation

- Sample MidTerm MC With AnswersDocument5 pagesSample MidTerm MC With Answersharristamhk100% (1)

- Multiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetDocument10 pagesMultiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetRhad Estoque0% (1)

- P1 - Winding UpDocument23 pagesP1 - Winding Upjinky2470% (10)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionD'EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionPas encore d'évaluation

- Seminar 11answer Group 10Document75 pagesSeminar 11answer Group 10Shweta Sridhar40% (5)

- Finals SolutionsDocument9 pagesFinals Solutionsi_dreambig100% (3)

- Asad NotesDocument15 pagesAsad NotesassadjavedPas encore d'évaluation

- Quiz For Finals For PrintingDocument4 pagesQuiz For Finals For PrintingPopol KupaPas encore d'évaluation

- Cpa Aditional CorlynDocument34 pagesCpa Aditional CorlynAlexaMarieAliboghaPas encore d'évaluation

- Assignment in Intermediateaccounting October 21Document12 pagesAssignment in Intermediateaccounting October 21Monica mangobaPas encore d'évaluation

- Semi-Finals Financial Accounting and ReportingDocument23 pagesSemi-Finals Financial Accounting and Reportingjoyce KimPas encore d'évaluation

- Reviewer in Financial MarketDocument6 pagesReviewer in Financial MarketPheobelyn EndingPas encore d'évaluation

- Quiz 2 Statement of Comprehensive Income Cash Vs Accrual BasisDocument11 pagesQuiz 2 Statement of Comprehensive Income Cash Vs Accrual BasisHaidee Flavier SabidoPas encore d'évaluation

- Afar (2018-2022)Document49 pagesAfar (2018-2022)Princess KeithPas encore d'évaluation

- Ma1 Sfe KaDocument6 pagesMa1 Sfe KaMarc MagbalonPas encore d'évaluation

- Commerce: Please Sub YTC: KnowledgeDocument5 pagesCommerce: Please Sub YTC: KnowledgeMuhammad HamidPas encore d'évaluation

- Lagura - Ass04 Statement of Comprehensive IncomeDocument7 pagesLagura - Ass04 Statement of Comprehensive IncomeShane LaguraPas encore d'évaluation

- MGT Adv Serv 09.2019Document11 pagesMGT Adv Serv 09.2019Weddie Mae VillarizaPas encore d'évaluation

- B. Sales Less Variable: Absorption CostingDocument3 pagesB. Sales Less Variable: Absorption CostingLaraPas encore d'évaluation

- Problems 1Document6 pagesProblems 1Russel BarquinPas encore d'évaluation

- LEVEL 2 Online Quiz - Questions SET ADocument8 pagesLEVEL 2 Online Quiz - Questions SET AVincent Larrie MoldezPas encore d'évaluation

- Practice FinalDocument13 pagesPractice FinalngStephanie26Pas encore d'évaluation

- Afar 5Document4 pagesAfar 5Tk KimPas encore d'évaluation

- Managerial AccountingDocument9 pagesManagerial AccountingChristopher Price100% (1)

- Final AFSTDocument7 pagesFinal AFSTCatherine ValdezPas encore d'évaluation

- Variable Costing vs. Absorption CostingDocument3 pagesVariable Costing vs. Absorption CostingLaraPas encore d'évaluation

- Cost AcctgDocument10 pagesCost AcctgCarl AngeloPas encore d'évaluation

- Cost Sheet Practical ProblemsDocument2 pagesCost Sheet Practical Problemssameer_kiniPas encore d'évaluation

- Mas Quizzer - Anaylysis 2021 Part 1Document6 pagesMas Quizzer - Anaylysis 2021 Part 1Ma Teresa B. CerezoPas encore d'évaluation

- Master Budget.5Document2 pagesMaster Budget.5Hiraya ManawariPas encore d'évaluation

- Accounting For Managers-Assignment MaterialsDocument4 pagesAccounting For Managers-Assignment MaterialsYehualashet TeklemariamPas encore d'évaluation

- MASDocument11 pagesMASgray downeyPas encore d'évaluation

- Tutorial Questions CVPDocument6 pagesTutorial Questions CVPChristopher LoisuliePas encore d'évaluation

- Quiz Bowl 10Document9 pagesQuiz Bowl 10mark_somPas encore d'évaluation

- Intermediate Accounting Chapters 9,10Document31 pagesIntermediate Accounting Chapters 9,10Jonathan NavalloPas encore d'évaluation

- MASPDocument3 pagesMASPSteeeeeeeephPas encore d'évaluation

- Management InformationDocument10 pagesManagement InformationTanjil AhmedPas encore d'évaluation

- Managerial AccountingDocument9 pagesManagerial AccountingJelyn RuazolPas encore d'évaluation

- 673 Quirino Highway, San Bartolome, Novaliches, Quezon CityDocument4 pages673 Quirino Highway, San Bartolome, Novaliches, Quezon CityRodolfo ManalacPas encore d'évaluation

- AttDocument8 pagesAttKath LeynesPas encore d'évaluation

- Mas MockboardDocument7 pagesMas MockboardMaurene DinglasanPas encore d'évaluation

- Financial Accounting Part 3Document6 pagesFinancial Accounting Part 3Christopher Price67% (3)

- College of Business Education PR 4 Management Advisory Services Diagnostic ExamDocument6 pagesCollege of Business Education PR 4 Management Advisory Services Diagnostic ExamMendoza Ron NixonPas encore d'évaluation

- Instruction: Shade The Letter of Your Choice in The Answer Sheet Provided. No Erasures AllowedDocument6 pagesInstruction: Shade The Letter of Your Choice in The Answer Sheet Provided. No Erasures AllowedmarygraceomacPas encore d'évaluation

- Cost FM Sample PaperDocument6 pagesCost FM Sample PapercacmacsPas encore d'évaluation

- Self Practice Cost AccountingDocument17 pagesSelf Practice Cost AccountingLara Alyssa GarboPas encore d'évaluation

- MSDocument9 pagesMSAeson Dela CruzPas encore d'évaluation

- Mas - ProblemsDocument14 pagesMas - ProblemsIyang LopezPas encore d'évaluation

- MS-1stPB 10.22Document12 pagesMS-1stPB 10.22Harold Dan Acebedo0% (1)

- Cma Part 1 Mock 2Document44 pagesCma Part 1 Mock 2armaghan175% (8)

- 0405 MAS Preweek QuizzerDocument22 pages0405 MAS Preweek QuizzerSol Guimary60% (10)

- Which of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Document3 pagesWhich of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Kath LeynesPas encore d'évaluation

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsD'EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsPas encore d'évaluation

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionD'EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionPas encore d'évaluation

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryD'EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsD'EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsPas encore d'évaluation

- Finance for IT Decision Makers: A practical handbookD'EverandFinance for IT Decision Makers: A practical handbookPas encore d'évaluation

- Fa 1 - Q1Document3 pagesFa 1 - Q1gon_freecs_4Pas encore d'évaluation

- TOS FinalsDocument1 pageTOS Finalsgon_freecs_4Pas encore d'évaluation

- Advanced Accounting 4 25Document2 pagesAdvanced Accounting 4 25gon_freecs_4Pas encore d'évaluation

- Advanced 5 24Document1 pageAdvanced 5 24gon_freecs_40% (1)

- TOS FinalsDocument1 pageTOS Finalsgon_freecs_4Pas encore d'évaluation

- Access 2007 TutorialsDocument34 pagesAccess 2007 Tutorialsbogsbest100% (4)

- Accounting 5 8Document1 pageAccounting 5 8gon_freecs_4Pas encore d'évaluation

- Sample Cash FlowDocument1 pageSample Cash Flowgon_freecs_4Pas encore d'évaluation

- Price List and Order Form 1st Sem., SY 2008-2009 Eff. June 2008 DeliveriesDocument1 pagePrice List and Order Form 1st Sem., SY 2008-2009 Eff. June 2008 Deliveriesgon_freecs_4Pas encore d'évaluation

- Price List and Order Form 1st Sem., SY 2008-2009 Eff. June 2008 DeliveriesDocument1 pagePrice List and Order Form 1st Sem., SY 2008-2009 Eff. June 2008 Deliveriesgon_freecs_4Pas encore d'évaluation

- Price List and Order Form 1st Sem (1) - SY 2007 2008 Revised May 30 2007Document1 pagePrice List and Order Form 1st Sem (1) - SY 2007 2008 Revised May 30 2007gon_freecs_4Pas encore d'évaluation

- VatDocument170 pagesVatgon_freecs_4Pas encore d'évaluation

- RO15 ProDocument5 pagesRO15 Progon_freecs_4Pas encore d'évaluation

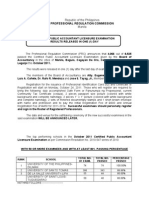

- Full Text of The Official Result of October 2011 Certified Public Accountants Licensure ExaminationDocument17 pagesFull Text of The Official Result of October 2011 Certified Public Accountants Licensure ExaminationPaul Michael Camania JaramilloPas encore d'évaluation

- PhotoshopDocument6 pagesPhotoshopGon FreecsPas encore d'évaluation

- VatDocument170 pagesVatgon_freecs_4Pas encore d'évaluation

- Full Text of The Official Result of October 2011 Certified Public Accountants Licensure ExaminationDocument17 pagesFull Text of The Official Result of October 2011 Certified Public Accountants Licensure ExaminationPaul Michael Camania JaramilloPas encore d'évaluation

- Performance of Schools in Alphabetical Order: (October 2011 Certified Public Accountant Licensure Examination)Document18 pagesPerformance of Schools in Alphabetical Order: (October 2011 Certified Public Accountant Licensure Examination)tristan20Pas encore d'évaluation

- May 2012 Certified Public Accountant Licensure ExaminationDocument1 pageMay 2012 Certified Public Accountant Licensure ExaminationPaul Michael Camania JaramilloPas encore d'évaluation

- CSForm 100 Rev 2012Document2 pagesCSForm 100 Rev 2012Agnes Antonio RodriguezPas encore d'évaluation

- CLS 12Document27 pagesCLS 12aarchi goyalPas encore d'évaluation

- Ar 2019 # Samindo-4 PDFDocument271 pagesAr 2019 # Samindo-4 PDFpradityo88100% (1)

- Fixed DepositDocument16 pagesFixed DepositPrashant MathurPas encore d'évaluation

- Insurance Types Importance Objective Alternative Takaful Feature of Takaful, Re Insurance, Takaful WorldwideDocument11 pagesInsurance Types Importance Objective Alternative Takaful Feature of Takaful, Re Insurance, Takaful WorldwideMD. ANWAR UL HAQUEPas encore d'évaluation

- GHope-Contents-Directors Profile-Letter To Shareholders-CEO ReviewDocument98 pagesGHope-Contents-Directors Profile-Letter To Shareholders-CEO ReviewGerald ChowPas encore d'évaluation

- Teuer B DataDocument41 pagesTeuer B DataAishwary Gupta100% (1)

- Indian Accounting StandardsDocument9 pagesIndian Accounting StandardsAman Singh0% (1)

- Industrial Tour Report On CSE (Chittagong Stock Exchange)Document42 pagesIndustrial Tour Report On CSE (Chittagong Stock Exchange)Khan Md Fayjul100% (2)

- Runaway Corporations: Political Band-Aids vs. Long-Term Solutions, Cato Tax & Budget BulletinDocument2 pagesRunaway Corporations: Political Band-Aids vs. Long-Term Solutions, Cato Tax & Budget BulletinCato InstitutePas encore d'évaluation

- Nego Digest Week 2Document13 pagesNego Digest Week 2Rufino Gerard MorenoPas encore d'évaluation

- Stanley Black DeckerDocument9 pagesStanley Black Deckerarnabkp14_7995349110% (1)

- Wikborg Global Offshore Projects DEC15Document13 pagesWikborg Global Offshore Projects DEC15sam ignarskiPas encore d'évaluation

- I Dunno What de Puck Is This2010-06-06 - 1901 I Do03 - EdmomdDocument2 pagesI Dunno What de Puck Is This2010-06-06 - 1901 I Do03 - EdmomdMuhammad Dennis AnzarryPas encore d'évaluation

- High Conviction BreakoutsDocument4 pagesHigh Conviction BreakoutsRajeshPas encore d'évaluation

- Job Sheet Od Buku BesarDocument13 pagesJob Sheet Od Buku Besarjuandry andryPas encore d'évaluation

- CheatsheetDocument2 pagesCheatsheetSafi NurulPas encore d'évaluation

- Life Insurance Advertising in India Analysis of Recen 337186587Document12 pagesLife Insurance Advertising in India Analysis of Recen 337186587Raghav DudejaPas encore d'évaluation

- Introduction To IPOsDocument1 pageIntroduction To IPOsaugusthrtrainingPas encore d'évaluation

- JDF 208 Application For Court-Appointed Counsel or GAL - R10 2015Document2 pagesJDF 208 Application For Court-Appointed Counsel or GAL - R10 2015Antoinette MoederPas encore d'évaluation

- Module 4 PDFDocument19 pagesModule 4 PDFRAJASAHEB DUTTAPas encore d'évaluation

- LCCI Level 3 - Advanced Business Calculations (Exam Kit)Document332 pagesLCCI Level 3 - Advanced Business Calculations (Exam Kit)BethanyPas encore d'évaluation

- NpaDocument22 pagesNpaDeepika VermaPas encore d'évaluation

- Perbandingan Akuntansi Akrual Di Swedia Dan FinalndiaDocument30 pagesPerbandingan Akuntansi Akrual Di Swedia Dan FinalndiaAbdul RohmanPas encore d'évaluation

- Synopsis and Points To Be UrgedDocument8 pagesSynopsis and Points To Be UrgedGeet ShikharPas encore d'évaluation

- Wise & Co. Vs TanglaoDocument5 pagesWise & Co. Vs Tanglaodominicci2026Pas encore d'évaluation

- MSC Ariel ZadikovDocument119 pagesMSC Ariel ZadikovAkansha JadhavPas encore d'évaluation

- GM Coogan - Money Creators Who Creates Money Who Should Create It 1935Document176 pagesGM Coogan - Money Creators Who Creates Money Who Should Create It 1935mrpoisson100% (1)