Académique Documents

Professionnel Documents

Culture Documents

Tax Accounting

Transféré par

semerederibeCopyright

Formats disponibles

Partager ce document

Partager ou intégrer le document

Avez-vous trouvé ce document utile ?

Ce contenu est-il inapproprié ?

Signaler ce documentDroits d'auteur :

Formats disponibles

Tax Accounting

Transféré par

semerederibeDroits d'auteur :

Formats disponibles

Chapter One: Introduction to Taxation and Tax Accounting

Chapter One Introduction to Taxation and Tax Accounting

Chapter Outline:

1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. What is taxation? Definition of tax and duty Tax accounting Interdisciplinary Nature of Taxation Objectives of taxation History of taxation Basic Elements of Tax Systems Tax Related Terms Basic characteristics of tax Types of Tax Rates Taxation Systems (Tax Rate Structures) Principles of taxation Canons of taxation Effects of Taxation Classification of taxes

Chapter Objectives:

After completing this chapter, you would be able to:

Define taxation, tax, duty, and tax accounting Understand why government levies taxes on citizens Discuss the evolution and history of taxation in the world and in Ethiopia Define different tax related terms Comprehend basic characteristics of taxes Identify and Calculate Different Types of Tax Rates Grasp the basic principles and canons of taxation See the effect of taxation on Economy Classify taxes on the basis of different dimensions

Time Required: 4 Hours

1.1) Taxation

Taxation is one of the systems that government uses to collect public revenues from various sources. However, taxation is the most important system of collecting public revenue in modern economic system. Taxation is the most powerful instrument in the hands of the government for transferring purchasing power from individuals to government. The money collected through taxation tax revenue is used to finance government operations. That is, the money required by the government to undertake different functions taxes is collected from the citizens. Without taxes to fund its activities, government could not exist. Thus, a government uses taxation as a system of raising the lion share of its revenue. Government uses the money collected through taxation: To pay soldiers and police; To build dams and roads; To operate schools and hospitals; To provide food to the poor and needy; To provide medical care to the elderly people; and To finance other hundreds of operations

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Tax Accounting (ACCT-332)

Taxation is used as a system of raising the lion share of public revenue in modern economic system to fulfill the requirement of the goods and services. Taxation depends on concepts from law, accounting, economics, public financial management, politics, behavioral sciences, etc. Thus, taxation can be considered as a part of special fields of study such as law (specifically tax law), accounting (specifically tax accounting), public financial management, economics, politics, etc. The scope of taxation includes tax policies, tax theories, tax decisions, and tax administration

1.2) Tax and Duty

Tax is defined as an amount of money levied by a government on its citizens and used to run the country. A tax is an involuntary fee or more precisely "unrequited payment" made by individuals or businesses to a government without quid pro quo. Human beings need four types of goods and services: Private goods consumed individually, for payment Toll goods consumed jointly, for payment Common pull goods consumed individually, for free Collective goods consumed jointly, for free Tax is an indirect payment for collective goods and services Duties are also taxes. Duties are distinguished from taxes by their strictly economic characteristic. For example, any government imposes a compulsory levy on the goods imported from a foreign country. This compulsory levy is called Custom Duty. Custom duty is compulsory a levy on individuals and companies importing goods to the country and its purpose is to protect the domestic market and economy. When goods are imported from abroad while the same goods can be produced within the country, it affects the domestic market and economy in number of ways as follows: It reduces demand for domestic products It discourage production within the county It discourages Foreign Direct Investment in the country It results in negative balance of payment (BOP) It increases the unemployment rate

1.3) Tax Accounting

Tax accounting is one of the specialized fields of accounting that encompasses activities such as: recording of tax related transactions; continuous follow-up of tax laws affecting a taxpayer i.e. individual or organizations; analyzing the consequences of tax on alternative business transactions/courses of actions determination of taxes and tax liabilities; preparation of tax returns or tax reports; and providing tax related information to assist decision makers Tax returns are government declaration forms filled and then filed with the Federal, State, or Local tax authorities. Tax returns are forms filed with the tax authority containing information used to calculate tax base and taxes (e.g. taxable income and the related income tax). Examples of tax returns (tax declarations), in Ethiopia, are: Business Income Tax Declarations VAT Declaration

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Chapter One: Introduction to Taxation and Tax Accounting

Employment Income Tax Declarations Turnover Tax Declaration Excise Tax Declaration Withholding Tax Declaration Other Income Tax Declarations

Tax accountant is an individual who assists a taxpayer in preparation of tax returns and who undertakes tax planning and other related activities.

1.4) Interdisciplinary Nature Taxation

A. Taxation and Economics Economics used taxation as one of the tools of fiscal policy and other economic measures B. Taxation and Public Financial Management Taxation is used as one of the systems of raising public revenue and it is one of the items that public financial management is concerned with. C. Taxation and Law Law provides rules and regulations that are used to guide taxation system so that the taxation system can be streamlined. D. Taxation and Politics Political decisions on tax related issues directly or indirectly affect the environment of taxation. E. Taxation and Accounting Accounting is concerned with regulation, control, and reporting of taxes from both sides: taxpayers and tax office F. Taxation and Behavioral Sciences Taxation is one of the things that highly affect human behavior. When a government increases or decreases taxes, taxpayers may react negatively or positively which could be subject of discussion in sociology and psychology

1.5) Objectives of Taxation

The objectives of taxation are: 1. To Raise public revenue 2. To Remove inequalities income and wealth 3. To Ensure economic stability 4. To Reduce regional imbalances 5. To Create employment opportunities 6. To Prevent harmful consumption 7. To Divert resources beneficially 8. To Encourage exports 9. To Enhance standard of Living

1.6) History of Taxation

History of taxation is concerned with these four questions: Who paid tax? What was taxed? Who collected taxes? In what form taxes were paid?

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Tax Accounting (ACCT-332)

1) History of Taxation in the World

A. Ancient Period (up to 5th Century AD)

Palestine, Egypt, Assyria, and Babylonia

Individual property rights did not exist The king was sole owner of everything in his domain Confiscated property and tribute payment from conquered peoples (additional source of finance) Ancient Athens (Greece) Relied on publicly owned silver mines Tribute from conquered countries Few custom duties, and Voluntary contributions from citizens. Poll tax - on slaves and aliens Eisphora - a tax imposed during war times Metoikion a poll tax on foreigners (people who did not have both an Athenian Mother and Father) Ancient Roman Republic Poll Tax on all roman citizens Roman military victories brought large amount of Foreign Tribute 5% Inheritance Taxes by Emperor (Caesar) Augustus Wheat and Salt tax 1 % sales tax for most goods and 4% sales tax for slaves by Emperor Julius and the sales tax on slaves was increased to 5% by Emperor Augustus Portoria The earliest custom duty in Rome on imports and exports

B. Medieval Period (5th to 15th Century AD)

Europeans were subject to many forms of taxation:

Land taxes Poll taxes Inheritance taxes, Tolls (payments for the use of bridges, roads, or seaports), and Miscellaneous fees and fines. Many people paid taxes in the form of money or crops. Taxes were paid directly to the local lords. An important development toward the end of the feudalism was taxes on Property Under the system of feudalism in Western Europe (11th Century): Kings, nobles, and church rulers all collected taxes. Kings derived income from their lands, from import and export duties, and from the various feudal dues and services owed by their vassals. Scutages - payments made in lieu of military service under King Edward of England Feudal nobility refused to pay scutages In 1215, Feudal nobility forced the king to sign the Magna Carta -the king agreed to collect scutages only with the common consent The Roman Catholic Church was a major tax collector during the middle ages Tithe. The church also collected various fees, fines, and tolls.

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Chapter One: Introduction to Taxation and Tax Accounting

C. Modern Period (16th Century AD to Date)

Strong centralized states emerged in Europe During the 16th and 17th centuries, these states relied heavily on revenues generated by the kings own estates and by taxes on land. In England, the power of Parliament grew steadily - in 1689 the English Bill of Rights guaranteed that the king could not tax without Parliaments consent. In 18th century, England started imposing various taxes on transactions. Taxes on imported goods (tariffs) assumed great importance. It also stated imposing income taxes. In 1799 Britain enacted the first national income tax - to finance the Napoleonic Wars. The war was ended up in 1815. The tax was discontinued after the war and revived in 1842. In the late 19th Century AD and early 20th Century AD, concerns about both fairness and the ability of tax systems to generate sufficient revenue led governments to enact income taxes. In 1853 - the first progressive income tax was used by Prussia. Other countries introduced progressive income taxation subsequently: Great Britain in 1907, United States in 1913, and France in 1917

2) History of Taxation in Ethiopia

A. Ancient Ethiopia

History of taxation in Ethiopia comes with the establishment of the government. The Aksum Kingdom minted coins in 500 AD which facilitated internal trades, external trades, and collection of taxes, which tells us that taxation was used starting from the Aksum Kingdom in Ethiopia

B. Medieval Ethiopia

During medieval period, in Ethiopia, taxation greatly varied from region to region and was often arbitrary There had been different obligations that were considered to be taxes including compulsory labor and compulsory hospitality This was evident during 15th century AD at the time of Emperor Zarayakobe Form 15th to 19th century AD taxation was carried out in haphazard manner It was also dependent on the will of the chief or the tax collector During Emperor Tewdros, as per Walter Plowden who was friend and consultant of the emperor, The taxes are numerous but varied according to the traditional customs of each village." C. Modern Ethiopia Emperor Menilik II carried out first important reform in taxation - a fixed tenth (tithe) was established rather than the undefined and arbitrary systems of agricultural taxes. The second major reform was the steady monetarization (monetization) of agriculture and other taxes. Emperor Haileselassie I continued the tax reforms started by Emperor Menilik II Modern tax collection procedure, tax schedules and the development of trained responsible bodies and regularly paid civil service came into existence. In 1943 (1935 E.C.) - a government body was established to collect taxes

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Tax Accounting (ACCT-332)

In 1944 - Proclamation No 60/1944 (1936 E.C ) was enacted and issued to be used as a tax code in collecting tax from all individuals and their jobs In 1949 - Proclamation No 107/1949 (1941 E.C) amended Proclamation No 60/1944. This second proclamation excluded agricultural income from taxes and made a tax holiday of 5 years for persons or businesses with a capital balance of less than Br 200,000. In 1954, Proclamation No 19/1954 (1946 E.C) was enacted and amended Proclamation No 107/1949. In 1961 - Proclamation No 173/1961 (1953 E.C) repealed Proclamation No 19/1954 Since then, there were few amendments to improve the tax proclamations and involved in changing tax rates from 35% up to 89% In the post-revolution period (1974 91) - significant major changes were made on the tax rate and structure of all types of taxes In 2002 - Proclamation No 173/1961 was repealed by Proclamation No 286/2002 (1994 E.C) after it served nearly 40 years. Proclamation No 286/2002 is currently in use in Ethiopia regarding income taxes

3) Taxation and Some Holy Books

A. The Bible and Taxation There are many evidences of taxation in the holy book bible. Different types of taxes were collected by the then governments in the holy book bible. These include Income Tax (Genesis 47:26), Property Tax (II Kings 23:35), Special Assessment Tax (II Chronicles 24:5), Poll Tax (Exodus 30:12) and Indirect taxes (Ezra 4:20) B. The Koran and Taxation In Koran, there are different contributions which are considered to be taxes. For examples, Khums, Jizya and Zakat are common contributions which can be considered taxes. Khums is one fifth of any item which a Muslim acquires as wealth, income and property and which must be paid as an Islamic tax.

1.7) Basic Elements of a Tax System

The five pillars or basic elements of tax system are taxpayer, tax base, tax rates, tax period, and tax administration. 1. Taxpayer refers to any individual or organization that is obligated to pay tax 2. Tax Base is the value of everything which is subject to taxation 3. Tax Rate is the amount of taxes expresses as a percentage of the tax base 4. Tax Period is the period for tax assessment. It can be a year (tax year), month, week, etc 5. Tax Administration refers to any government office mainly with a responsibility of tax collection and other related activities

1.8) Tax Related Terms

1. 2. 3. 4. 5. Delinquent Tax refers to taxes remaining unpaid on and after the date of penalty Fiscal Year refers to the twelve month period used by the government Gross Income is the total income of individual or business Tax Abatement refers to a complete or partial cancellation of imposed taxes Tax Assessment is the determination of the amount subjected to tax 6

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Chapter One: Introduction to Taxation and Tax Accounting

6. Tax Avoidance refers to the practice of paying as little tax as possible 7. Tax Bracket is a range of income subject to tax at the same tax rate. It is the band of taxation in which a taxpayer is in. 8. Tax Cut is the act of reducing taxes for certain reason 9. Tax Credit is an investment activity which directly minimizes the tax to be paid 10. Tax Deed is a written instrument by which title to property sold for taxes is transferred unconditionally to the purchaser 11. Tax Deduction is the amounts legally permitted to be subtracted from gross income 12. Tax Evasion is an illegal activity in which a taxpayers seek to hide taxable income by overstating expenses or understating revenues 13. Tax Exemption is a legal provision that permits to deduct specified amount from gross income as a tax free income. The term tax exempt income can be used interchangeably with tax free income. 14. Tax Exile refers to somebody who leaves a country in order to avoid paying taxes 15. Tax Favored Investment refers to an investment whose profits are taxed lower tax rate 16. Tax Function is a function of tax accountant 17. Taxable Income refers to the amount of an Individual or business income which is subject to taxation 18. Tax Heaven means a country with favorable tax rates 19. Tax Holiday is period of no taxation 20. Tax Liability is the legal obligation of a taxpayer to the government 21. Tax Liens is claim for unpaid taxes 22. Tax Levy is the total amount of taxes imposed on an individual or corporation 23. Tax Method is a method of recording trading of plant assets for tax purposes with no gain or loss 24. Tax Penalties are fines or punishments imposed on a taxpayer 25. Tax Refund an amount that a government gives back to a taxpayer 26. Tax Relief is tax savings in the form of special allowable deduction. E.g. Capital Gain loss, Business Loss 27. Tax Return is a government tax collection form 28. Tax Schedule is the official list of tax rates matched with different level of incomes 29. Tax Shelter is an investment activity that protects some of a taxpayer's income form taxes. E.g. Investment in Treasury Bills 30. Tax Subsidy refers to a government subsidy to a particular company in the form of reduced tax

1.9) Basic Characteristics of Tax

Tax has the following basic characteristics: 1. Tax is a compulsory payment 2. Benefits are not the basic condition in tax payment 3. It is a personal obligation 4. It is used for Common interest 5. It is a Legal collection 6. Element of Sacrifice is seen in tax 7. It is a periodic and regular payment 8. It has Wide Scope 9. No discrimination exists in tax payment

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Tax Accounting (ACCT-332)

1.10) Types of Tax Rates There are four different types of tax rates: statutory tax rate, marginal tax rate, average tax rate, and effective tax rate, which are discussed as follows:

Statutory Tax Rates (STRs): all the tax rates applicable to a particular type of tax. They are

legally imposed tax rates on a taxpayer. Statutory tax rates are those percentages appearing in the tax law. Marginal Tax Rate (MTR): is the tax rate that applies to the taxpayers last birr of taxable Income. It is the ratio of change in tax to taxable income Average Tax Rate (ATR): is the ratio of the amount of taxes paid to taxable income Effective Tax Rate (ETR): is the ratio of the amount of taxes paid to the total income Example 2.1: assume that income is taxed on a Schedule Exempt from Br 0 up to 150, 10% over Br 150 to 650, 15% over Br 650 to 1400, 20% over Br 1400 to 2350, 25% over Br 2350 to 3550, 30% over Br 3550 to 5000 and 35% over Br 5000. Instruction: Determine the Marginal Tax Rate, Statutory Average Tax Rate and Effective Average Tax Rate for a taxpayer with a basic salary of Br 5300 and with no special allowances.

1.11) Tax Rate Structures (Tax Systems)

Tax rate structure expresses the relationship between the tax rate and tax base in a country. Currently nations are using four different types of tax systems: progressive tax system, proportional tax system, regressive tax system, and degressive tax system.

1. Progressive Tax System

Tax Rate

35% 30% 25% 20% 15% 10% Tax Base in Birr 150 650 1400 2350 3550 5000

Tax Rate Structure

2. Proportional Tax System

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Chapter One: Introduction to Taxation and Tax Accounting

Tax Rate

10%

Tax Rate Structure

1500

6500

14000

23500

35500

50000

Tax Base in Birr

3. Regressive Tax System

Tax Rate

20%

15%

10%

5%

Tax Rate Structure

4000

6000

12000

15000

Tax Base in Birr

4. Degressive Tax System

Tax Rate

25%

15% 10% Tax Rate Structure

500

1000

3000

5000

7000

Tax Base in Birr

5. Government Tax Revenue and Taxation System

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Tax Accounting (ACCT-332) Tax Rate Progressive Taxation System Proportional Taxation System Degressive Taxation System

Regressive Taxation System

Tax Base in Birr

1.12) Principles of Taxation

1. Principle of Economic Neutrality The taxation system of a country must be economic neutral. Taxation should not have unneutral effects. Taxation must not create economic distortion. Taxation may the following unneutral effects: A. Affecting the Consumer Choice B. Affecting the supply of Factors of Production 2. Principle of Equity The tax burden should be fair and equal. There are two approaches how a government could be fair. The government may use one of the following to be fair: A. Benefit Received Approach B. Ability - to - Pay Approach Horizontal Equity means persons in like circumstances should be treated equally. Vertical Equity means persons in unlike circumstances should get relative treatment 3. Principle of Efficiency According to this principle, a Taxation System a country should be economically and administratively efficient. A. Economic Efficiency - taxation system of a country should be economical B. Administrative Efficiency taxation system of a country should have sufficient number and competent staffs.

1.13) Canons of Taxations

1. Canon of Equality - every person ought to contribute toward the support of the Government, as nearly as possible, in proportion to their abilities 2. Canon of Certainty tax which each individual is required to pay should be certain and not arbitrary. 3. Canon of Convenience mode and timings of tax payment should be, so far as possible, convenient to the taxpayer. 4. Canon of Economy - recommends that cost of collection of taxes should be the minimum possible.

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

10

Chapter One: Introduction to Taxation and Tax Accounting

5. Canon of Productivity (Canon of Adequacy) - the tax system should be productive enough. It should enable to collect sufficient tax revenue. 6. Canon of Elasticity (Canon of Flexibility) - this canon implies that taxes should be increased or decreased according to the needs of the government. 7. Canon of Diversity-the tax system should be diverse in nature. 8. Canon of Simplicity-a tax system should be easily understood by the Taxpayer 9. Canon of Expediency-taxes should be levied after considering all favorable and unfavorable factors from different angles such as economical, political and social. 10. Canon of Buoyancythe tax revenue should have an inherent tendency to increase along with an increase in national income even if the rates and coverage of taxes are not revised. 11. Canon of Co-ordination: according to this canon, there should be a proper co-ordination between various authorities (Federal, State and Local Tax Collecting Agencies) while imposing taxes so as to avoid double and triple taxation.

1.14) Classification of Taxes

1. Classification Based on the Tax Bases A. Income Taxes: are taxes levied on income of persons or businesses B. Property Taxes: are levied on a property of Persons or businesses C. Commodity Taxes: are taxes levied on commodities and services 2. Classification Based on ultimate burden of taxes (Based on Tax Impact, Tax Shifting and Tax Incidence) Tax Impact refers to the person who bears the money burden of tax in the first instance Tax Incidence refers to the person who ultimately bears the money burden of a tax Tax Shifting refers to the process by which the money burden of a tax is transferred from one person to another person. Based on ultimate burden, taxes are classified into two: Direct Taxes and Indirect Taxes described as follows: A. Direct Taxes: are taxes the impact and incidence of which fall on the same person. Direct taxes are taxes which can not be shifted on to the others. E.g. Employment income tax B. Indirect Taxes: these are taxes the impact and incidence of which fall on different persons. The impact fall on one person and the incidence fall on another person. E.g. VAT 3. Classification Based on Tax Determinant A. Ad-valorem Taxes: taxes are determined based on the value of the item to be taxed. B. Specific Tax: are the taxes levied at a fixed amount, irrespective of the value of the goods and services 4. Classification Based on Number of Taxes A. Single Tax: using only one tax in the country. It is a tax on one thing B. Multiple Taxes: using many kinds of taxes in the country. The government of modern state uses diversified taxes to use advantage of it 5. Classification based on Taxing Authority Taxes are classified into three based on taxing authority or taxing hierarchy: Federal Taxes, State Taxes and Local Taxes A. Federal Taxes: are taxes collected by Federal government tax agency B. State Taxes: are taxes collected by Regional State governments C. Local Taxes: are taxes collected by local tax authorities

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

11

Tax Accounting (ACCT-332)

1.15) Effects of Taxation

Taxation might have different effects in an economy. Taxation has a positive or adverse effect on production, distribution of income, and economic stabilization 1. Effects of Taxation on Production Taxation may affect either adversely or positively production in an economy. Increasing or decreasing the tax rate affects the ability to work, save and invest and will to work, save and invest. Thus, it affects production 2. Effects of Taxation on Distribution of Income Taxation is used in most countries to distribute fairly the income generated in a country. 3. Effects of Taxation on Stabilization of Economy During abnormal prices rises (inflation), taxation can be used as a tool to stabilize the economy. Inflation is results of either demand pull or cost push. In demand pull inflation, the government should increase the tax so as to reduce the capacity of the people to purchase. In cost push inflation, the government uses taxation to minimize and control cost of production so as to reduce the price of goods and services

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

12

Chapter Two: Employment Income Tax Accounting

Chapter Two Employment Income Tax Accounting

Chapter Outlines:

Components of Employment Income Employment Income Tax Rates Employment Income Tax Exemptions Computation of Taxable Employment Income Computation of Employment Income Tax Employment Income Tax Declaration

Chapter Objectives

After completing this chapter, you would be able to:

Differentiate benefits that are included in employment income Understand the basic legal provisions (tax laws) applicable on employment income in Ethiopia Calculate taxable employment income Determine employment income tax as per the tax law of the country Determine employment income tax on severance pay, bonus and other employment benefits Account for employment income tax related transactions Complete Employment Income Tax Declaration (FIRA Form 1103) Complete Personal Income Tax Declaration (FIRA Form 1105)

Time Required: 4 Hours

2.1) What is Employment Income? (Components of Employment Income)

As per Article 12 of Income Tax Proclamation No. 286/2002, employment income shall include any payments or gains in cash or in kind received from employment by an individual from all the employers. These include: 1. Basic salary or wages 2. Overtime (OT) Income a. For OT jobs between 6:00 AM to 10:00 PM, OHR=RHR @ 1.25 b. For OT jobs between 10:00 PM to 6:00 AM, OHR=RHR @ 1.5 c. For OT jobs on weekly rest day, OHR=RHR @ 2.0 d. For OT jobs on public holiday, OHR=RHR @ 2.5 3. Allowances a. Acting allowance b. Board allowance c. Cash indemnity allowance (cash fault allowance) d. City compensation allowance e. Educational allowance f. Hardship allowance (desert allowance) g. Cell phone allowance (mobile allowance) h. Disturbance allowance i. House rent allowance (house subsidy) j. Meal allowance (lunch allowance) k. Medical allowance l. Per-diem allowance (daily allowance) m. Position allowance n. Computer allowance

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

13

Tax Accounting (ACCT-332)

Representation allowance Transportation allowance (fuel allowance) Entertainment allowance (guest accommodation expenses) Stress allowance: a special payment made to employees whose job is stressful. E.g. air traffic controllers s. License allowance: a special payment made to licensed employees. E.g. air traffic controllers 4. Bonus: payment made to employees of businesses as acknowledgment of employees hard work and effort in generating beyond expected amount of profit. 5. Employment Termination Payment a. Severance Pay- the severance pay shall be thirty times his or her daily wages of the last week of service for the first year of service; for the service less than one year, severance pay shall be calculated in proportion to the period of service. If the worker has served for more than one year, payment shall be increased by one-third of the previous sum for every additional year of service, within the limit of a total amount of twelve months salary b. Job Search Payment c. Compensation Payment d. Annual Leave Payment e. Job Termination Bonus

o. p. q. r.

2.2) Basic Legal Provisions of EIT The legal provisions are taken form Income Tax Proclamation No. 286/2002 and Income Tax Regulation No. 78/2002. Employment Income Tax Rates

Article 11 of Income Tax Proclamation No. 286/2002 provides that the following tax rate schedule shall be applied on employment income

Schedule A

Employment Income per Month TB Over Birr To Birr st 1 0 150 2nd 150 650 rd 3 650 1,400 th 4 1,400 2,350 5th 2,350 3,550 th 6 3,550 5,000 7th 5,000 xxxxx Tax Liability Tax Rate Exempt (0%) 10% 15% 20% 25% 30% 35%

Employment Income Tax Exemptions

Art 13 of Proclamation No 286/2002 exempts the following employment income from taxation: a. Income from employment received by casual employees b. Pension contribution, provident fund contributions and all forms of retirement benefits not more 15% of basic salary c. Income from employment received by diplomatic and consular representatives; and other persons employed in any Embassy d. Income specifically exempted from income tax by any law in Ethiopia

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

14

Chapter Two: Employment Income Tax Accounting

e. Payments made to a person as compensation or gratitude in relation to personal injuries; or the death of another person. Art 3 of Regulation 78/2002 exempts the following allowances from taxation: a. Medical Allowance b. Transportation Allowance c. Hardship Allowance d. Per-diem Allowance (Daily Allowance) e. Traveling Expenses f. Board Allowances of public enterprises board members g. Income of persons employed for domestic duties

2.3) Computation of Taxable Employment Income (TEI)

Every person deriving income from employment is liable to pay tax on that income at the rate specified in Schedule "A", set out in Article 11. But the entire employment income is not taxable as some the employment benefits are non taxable. Taxable employment is the sum of all taxable employment benefits. Taxable income shall mean the amount of income subject to tax after deduction of all expenses and other deductible items as per Article 2 of Proclamation No. 286/2002. The first Birr 150 employment income exclusion from taxable income should be considered as a taxable employment income at the rate of zero percent. TEI = Gross Employment Income Special Tax Exemption Tax Allowances 1. Gross Employment Income refers to any income earned from employment sources regardless of the way it is earned 2. Tax Exemptions are employment incomes exempted from EIT. Tax Exemptions are classified into two: Special Exemptions and Personal Exemption A. Special Tax Exemptions are income directly exempted by the income tax proclamation in Ethiopia for special reasons. B. Personal Exemption is a non-taxable income for each employee under Schedule A per month. It is common to all employees regardless of their employment income, which is Br 150 per month. It is considered an income taxable at rate of 0%. 3. Tax Allowances are amounts which are allowed or permitted to be deducted from Gross Employment Income for different reasons However, there is no tax allowance in Ethiopia so that the formula for calculating taxable Employment income can be modified to the following form: TEI= Gross Employment Income Special Tax Exemptions. The detail calculation can be in one of the following two ways Alternative 1: When all payments are made at the end of the month

Determination of Taxable Employment Income

Basic salary.............................................................................................. Xxxxx Overtime Pay .......................................................................................... Xxxxx Transport allowance................................................................................ Xxxxx Other allowances..................................................................................... Xxxxx Gross Employment Income..................................................................... Xxxxx Less: Special Tax Exemptions ................................................................ (xxxxx) Taxable Employment Income ................................................................. Xxxxx

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

15

Tax Accounting (ACCT-332)

Alternative 2: Special Exemptions can be paid any time

Determination of Taxable Employment Income

Basic salary.............................................................................................. xxxxx Overtime pay .......................................................................................... xxxxx Taxable Transport allowance.................................................................. xxxxx Other Taxable allowances....................................................................... xxxxx Tax Employment Income........................................................................ xxxxx

Adding Tax on Income

If the tax on income from employment instead of being deducted from the salary or wage of the employee is paid by the employer in whole or in part, the amount so paid shall be added to the taxable income and shall be considered as part thereof (Article 4, Regulation No 78/2002).

Illustrations on calculating TEI

Example 2.1: Ato Hizkiyas is an employee of Excel Pvt. Ltd. Co. The basic salary of Br 3,200 is

meant for 160 normal working hours. He worked 170 hours during the month of Hamle 2006. Assuming that all overtime work is done on employee rest days and the employee received Br 300 transportation allowance according to the employment contract, determine the taxable employment income. Required: determine taxable employment income

Example 2.2: Ato Daniel is a loan officer at Awash International Bank. Determine the Taxable

Employment Income of Ato Daniel if his monthly salary of Br 2,800 is for 176 Normal Working Hours and the Employers Contribution to Provident Fund is 20% of Daniels basic salary.

Example 2.3: Ato Samuel is head of Human resource department of BB Family Pvt. Ltd. Co.

Assume the following He gets a monthly salary of Br 2,640 for 176 normal working hours; He worked 186 hours during the month of Sene 2006 and all overtime work is done from 6:00 A.M. to 10:00 P.M. He is entitled to receive a Transportation Allowance of Br 1000 Required: determine the Taxable Employment Income of Ato Samuel

Example 2.4: the employment contract between Ato XY and his employer stated that Ato XY will receive a basic salary of Br 940 net of tax (after the tax is deducted) and the employer agreed to pay Br 110 tax to the tax authority on the basic salary amount. The normal working hours are 150. Determine the taxable income for the month of Nehase and Pagumen assuming that Ato XY worked 170 Hours and all overtime work was done on employee rest days

2.4) Accounting For Employment Income Tax

Accounting for employment income tax is concerned with determination of Taxable Employment Income as we discussed earlier. Accounting is also concerned with: A. Determination EIT Base i.e. Taxable Employment Income B. Calculation of Employment Income Tax; C. Preparation of Employment Income Tax Declaration; and D. Recording Employment Income Tax Related Transactions Recording transactions is an overlapping activity with payroll accounting but the tax accountant need not consider other transactions on the payroll

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

16

Chapter Two: Employment Income Tax Accounting

2.4.1) Calculation of Employment Income Tax (EIT)

A. Progression Method the EIT is computed progressively applying the tax rates in Schedule A Example: take example 3.1 to 3.4 and calculate Employment Income Tax under progression method

B. Deduction Method

EIT = Taxable Employment Income @ Marginal Tax Rate Deduction

Table 2:1 Employment Income Tax under Deduction Method

TB 1st 2nd 3rd 4th 5th 6th 7th Range of TEI 0 150 150 650 650 1,400 1,400 2,350 2,350 3,550 3,550 5,000 Over 5,000 Tax Rate Exempt 10% 15% 20% 25% 30% 35% Deduction 0.00 15.00 47.50 117.50 235.00 412.50 662.50 EIT Calculation No Tax Payment EIT = TEI @ 10% 15 EIT = TEI @ 15% 47.50 EIT = TEI @ 20% 117.50 EIT = TEI @ 25%n 235 EIT = TEI @ 30% 412.50 EIT = TEI @ 35% 662.50

C. Addition Method

EIT = Addition + [(TEI Lower Tax Bracket) @ Marginal Tax Rate] The Addition is equal to the EIT amount payable on the Previous Tax Bracket

Table 2.2: Employment Income Tax under Addition Method

TB 1st 2nd 3rd 4th 5th 6th 7th Range of TEI 0 150 150 650 650 1,400 1,400 2,350 2,350 3,550 3,550 5,000 Over 5,000 Tax Rate Exempt 10% 15% 20% 25% 30% 35% Addition 0.00 0.00 50.00 162.50 352.50 652.50 1,087.50 EIT Calculation No Tax Payment EIT = 0.00 + (TEI 150) @ 10% EIT = 50.00 + (TEI 650) @ 15% EIT = 162.50 + (TEI 1,400) @ 20% EIT = 352.50 + (TEI 2,350) @ 25% EIT = 652.50 + (TEI 3,550) @ 30% EIT = 1,087.50 + (TEI 5,000) @ 35%

Example 2.5: Assuming a Taxable Employment Income of Br 1,000, determine employment income tax under Progression, Deduction, and Addition Method Example 2.6: Determine the Employment Income Tax to be paid by Ato Girma for taxable employment income of Br 3,600 for the month of Hamle 1999 under the three Employment Income Tax calculation methods

Employment Income Tax on Job Termination Payments EIT on Severance Pay

The EIT on Severance Pay is computed as follows: Determine the total severance pay Determine number of months with severance pay - the total Severance Pay is divided by the basic salary of the employee at the time the Employment of Contract is terminated Determine the EIT on Severance Pay per month using Schedule A Determine the EIT on the total Severance Pay

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

17

Tax Accounting (ACCT-332)

If there is any remainder after determining the full number of months, the severance pay is treated separately as one month taxable income for tax purposes. Example 3.7: Assume that the contract of employment is terminated when the basic salary of the employee is Br 2,000. Determine the Employment Income Tax on the Severance Pay of Br 12,000

Reading Assignment: Employment Income Tax on Ordinary Annual Bonus Employment Income Tax on Weekly and Bi-Weekly Salary and other employment benefits

2.4.2) Preparation of Employment Income Tax Declaration

The Federal Inland Revenue Authority (FIRA) introduced Employment Income Tax Declaration (Form 1103) as of July 2006. The Employer is required to file Form 1103. Form 1103 has five sections:

1. 2. 3. 4. 5. Taxpayer Information Declaration Details Calculation of Tax Due Employees Removed From Payroll Taxpayer Certification

2.4.3) Recording Employment Income Tax Related Transactions

At the time of payment of Employment Income, the appropriate income tax liability should be recorded. The Withheld EIT should be credited to liability account. This Withheld EIT (EIT deducted at source) should be submitted to the tax authority within the time frame set in the income tax proclamation. At time of submission the related liability account should debited.

Exercise: You are given the following: basic Salary, Overtime Hours, Overtime Duration, Allowances of Employee of SHINA Plastic Factory Pvt. Ltd. Co. for the Month of September 1999 E.C.

S. No. 1 2 3 4 5 6 7 8 Employee Name ABY CAM GFD KKK LMA WZB ZFW SBH Basic Salary Br 3,200 4,800 1,600 2,400 2,880 1,760 2,080 1,080 Normal Working Hours 160 160 160 160 160 160 160 160 Overtime Hours 20 5 8 12 10 10 Overtime Duration 6:00A.M -10:00 PM 10:00PM -6:00 AM Weekly Rest Days Public Holidays Weekly Rest Days Weekly Rest Days Allowances 1000 (PA) 500(TA) 500 (TA) 500 (TA) 500 (TA) 500 (TA) 500 (TA)

Required:

A. Determine the Gross Employment Income, Taxable Employment Income and the Employment Income Tax B. Prepare the Employment Income Tax Return i.e. Complete Form 1103 (Employment Income Tax Declaration) to be filed with FIRA. C. Show all the accounting entries

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

18

Chapter Two: Employment Income Tax Accounting

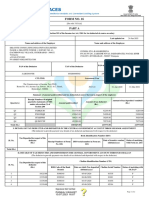

Federal Democratic Republic of Ethiopia Ministry of Revenue Federal Inland Revenue Authority

Schedule A

Employment Income Tax Declaration Form (Income Tax Proclamation No.286/2002 & Income Tax Regulation No. 78/2002 3. TIN

0000121361

Section 1: Taxpayer Information

A) Taxpayers Name (Company Name, Fathers Name, Grandfathers Name) SHEENA Consultancy Pvt. Ltd. Co. 2A. Region - Addis Ababa 2B. Zone / Kifle Ketema - Kirkos 2C. Woreda 2D. Kebele /Farmers Association 2E. House Number 14/53 1534

A) Seq. No. 1 2 3 4 5 6 7 B) Employee TIN S000121 S000122 S000123 S000124 S000125 S000126 S000127 C) Employee Name ABY CAM GFD KKK LMA WZB ZFW D) Date of Employmen t E) Basic Salary

4. TAN 000112

5. Tax Center - Kirkos 6. Telephone 7. Fax Number

011 125 3434 011 125 4141

8. Tax Period Page 1 of _2__ Month Year Sep. 1999 Document Number (Official Use Only)

Section 2: Declaration Details

F) Total Additional Benefit Transportation G) Taxable H) OT allowance Transportation Income Allowance Sep. 2004 3200 500 July 2003 4800 500 225 August 2004 1600 500 100 160 Dec. 2004 2400 500 450 January 2005 2880 500 360 January 2005 1760 500 60 January 2005 2080 500 260 Transfer totals from the last continuation sheets to the Line I) Other Taxable Benefits 1000.00 Total

J) Taxable Income (sum columns E, G, H and I

K) Tax WH 997.50 1096.25 254.50 477.50 575.00 246.50 350.50 114.50 4112.25 (Line 30)

I) Cost Shari ng

M) Net Pay

N) Emp. Sign

4700.00 5025.00 1860.00 2850.00 3240.00 1820.00 2340.00 1080.00 22915.00 (Line 20)

3702.50 4428.75 2005.50 2872.50 3165.00 2013.50 2489.50 20677.25

Section 3: Calculation of Tax Due

10 20 30 Number of Employees on Your Payroll for this Tax Period Total Taxable Income (From Column J Above) Total Tax Withheld (From Column K Above) 8 Br 22,915.00 Br 4,112.25

Seq. No.

Section 4: Employees Removed from Payroll

Employee TIN Employees Name Use OnlyFor Office Date of Payment Receipt No. Amount Payment Cheque No. Cashiers Sign.

Section 5: Employers Certification

I declare that the above declaration and all information provide here with (Including continuation sheets) is correct and complete. I understand that any misrepresentation is punishable as per the Tax Laws and the penal Code

Taxpayer or Authorized Agent Name: Signature: Date: Employer Seal For Tax Office: Authorized Tax Officer Name: Signature: Date:

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

19

Tax Accounting (ACCT-332)

Ethiopian Revenues and Customs Authority (ERCA) Continuation Sheet

FORM 1103

Employment Income Tax Declaration (Continuation Sheet for Form 1103)(Form 1104) (Income Tax Proclamation No. 286/2002 & Income Tax Regulation No. 78/2002) 2. TIN 3. Tax Period

Federal Democratic Republic of Ethiopia Ministry of Revenue Federal Inland Revenue Authority

1. Taxpayers Name (Company Name) SHEENA Consultancy Pvt. Ltd. Co.

Section 1: Taxpayer Information

0000121361 Month Sep.

J) Taxable Income (Sum Columns E, G, H, And I) K) Tax Withheld

Year 1999

L) Cost Sharing

Page _____2_____ Of _______2_____

Section 2: Calculation of Payments to Employees

A) Seq Num B) Employee TIN C) D) E) Employee Date Of Basic Name Employment Salary F) Transport Allowance Additional Benefits G) H) I) Taxable Over Other Transport Time Taxable Allowance Benefits M) Net Pay N) Employee Sign

S000127

SBH

January 2005

1,080

1,080

114.50

965.50

Totals from Previous Continuation Sheet(s) if Used Carry Totals from Final Continuation Sheet to Page 1 of EIT Declaration, Form 1103

1,080 (Line 20)

114.50 (Line 30)

Name of taxpayer/Authorized Agent: Ethiopian Revenues and Customs Authority (ERCA)

Signature :

Employer Seal

FORM 1104

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

20

Chapter Three: Rental Income Tax Accounting

Chapter Three Rental Income Tax Accounting

Chapter Outlines:

Overview of Rental Income Tax Basic Legal Provisions for Rental Income Tax as per the tax law of the country Accounting for rental income tax

Chapter Objectives

After completing this chapter, you would be able to:

Understand the concepts of Rental Income Tax in Ethiopia Identify the lessee, lessor, and sub-lessor and understand who should pay rental income tax Determine Gross Rental Income and Taxable Rental Income Know deductible expenses for Rental Income Tax purposes Calculate Rental Income Tax for taxpayers maintaining books of accounts and not maintaining books of accounts Understand briefly the Rental Income Tax Declaration (FIRA Form 1201)

Time Required: 2 Hours

3.1) Introduction to Rental Income Tax

Rental Income is taxed under Schedule B of Income Tax Proclamation No. 286/2002 Income generated by renting either Residential or Business Buildings is taxable There are two parties to the lease contract in buildings: The Lessor and Lessee.

Sometimes the third party called Sub-lessor may part of it

The leased building can be empty or furnished Advance Payments: income that covers a period longer than one year shall be prorated

over the number of years covered by the amount paid for tax purposes. Responsibility of the Local Administration: Informing to the Tax Authority

3.2) Basic Legal Provisions for Rental Income Tax (RIT) The legal provisions are taken form Income Tax Proclamation No. 286/2002 and Income Tax Regulation No. 78/2002. 3.2.1) Taxable Rental Income (TRI) Taxable Rental Income = Gross Rental Income Deductible Expenses Determination of Gross Rental Income

Gross Rental Income shall include: All payments in cash and all benefits in kind received by the lessor (owner of the building) from the lessee; All payments made by the lessee on behalf of the lessor according to the contract of lease; for example if the lessee agreed to pay brokerage cost on behalf of the lessor. The value of any renovation or improvement made under the contract of lease to the land or building, where the cost of such renovation or improvement was borne by the lessee in addition to rent payable to the lessor; If the tax payer leased furnished quarters the amounts received attributable to the lease of furniture and equipment shall be included in Gross Rental Income in addition to the above rental incomes.

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

21

Tax Accounting (ACCT-332)

Deductible Expenses from Gross Rental Income

The following amounts shall be deducted from income in computing taxable income: Taxes paid with respect to the land and buildings being leased; except Rental Income Taxes; and For taxpayers not maintaining books of account, one fifth (1/5) of the gross income received as rent for buildings, furniture and equipment as an allowance for repairs, maintenance and depreciation of such buildings, furniture and equipment; For taxpayers maintaining books of account, the expenses incurred in earning, securing, and maintaining rental income, to the extent that the expenses can be proven by the taxpayer and subject to the limitations specified in Proclamation No.286/2002, deductible expenses include (but are not limited to) the cost of lease (rent) of land ,repairs, maintenance, and depreciation of buildings, furniture and equipment in accordance with Art 23 of Proclamation No 286/2002 as well as interest on bank loans, insurance premiums

3.2.2 Tax Rate

On rental income of body thirty percent (30%) of Taxable Rental Income On income of persons according to the Schedule B (hereunder)

Schedule B

TB 1st 2nd 3rd 4th 5th 6th 7th Range of Rental Income 0 1800 1,800 7,800 7,800 16,800 16,800 28,200 28,200 42,600 42,600 60,000 ***** 60,000 T RI 6,000 9,000 11,400 14,400 17,400 Tax Rate Exempt (0%) 10% 15% 20% 25% 30% 35%

3.3) Accounting for Rental Income Tax

In this case, accounting is involved with the following tasks: Determination of Gross Rental Income and Taxable Rental Income Calculation of Rental Income Tax Preparation of Rental Income Tax Return

3.3.1) Determination of Gross Rental Income and Taxable Rental Income

Taxable Rental Income for those Taxpayers Maintaining Books of Accounts Rental Income Received................................................................ Add: the following amounts Amount on the lease of furniture................................................... Amount on the lease of equipments.............................................. Payments made by the lessee on behalf lessor ............................. Cost renovation or improvement paid by the lessee...................... Gross Rental Income..................................................................... Less: Rental Payment.................................................................... Net Rental Income......................................................................... xxxxx xxxxx xxxxx xxxxx xxxxx xxxxx (xxxxx) xxxxx 22

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

Chapter Three: Rental Income Tax Accounting

Less: deductible expenses Land and building tax....................................................................xxxxx Annual lease payment on land.......................................................xxxxx Cost of repairs and maintenance....................................................xxxxx Depreciation of building................................................................xxxxx Depreciation of furniture and equipment......................................xxxxx Interest on bank loans....................................................................xxxxx Adverting expense to call tenant...................................................xxxxx Other expense, if any incurred to generate rental income.............xxxxx Insurance premiums.......................................................................xxxxx Total deduction.............................................................................. (xxxxx) Taxable rental income................................................................... xxxxx

Taxable Rental Income for those Taxpayers not maintaining Books of Accounts

Rental Income Received....................................................................... Add: The Following Amounts Amount on the lease of furniture.......................................................... Amount on the lease of equipments...................................................... Payments made by the lessee on behalf lessor ..................................... Cost renovation or improvement paid by the lessee............................. Gross Rental Income............................................................................. Less: Rental Payment............................................................................ Net Rental Income (NRI) ..................................................................... Less: Deductible Expenses Land and building tax, if any................................................................xxxx x Allowance for repairs, maintenance & depreciation (20%@NRI).......xxxx x Total deductible expense Taxable rental income........................................................................... xxxxx xxxxx xxxxx xxxxx xxxxx xxxxx (xxxxx) xxxxx

(xxxxx) xxxxx

Calculation of Rental Income Tax (RIT)

Sub-lessor shall pay the tax on the difference between income from sub-leasing and the rent paid to the lessor, provided that the amount received from the sub-lessor is greater than the amount payable to the lessor In the computation of Rental Income Tax, the taxpayers can use the progressive method using Schedule B or Deduction Method

Deduction Method

RIT = Taxable Rental Income @ Marginal Tax Rate Deduction TB 1st 2nd 3rd 4th Over 0 1,800 7,800 16,80 0 To 1,800 7,800 16,800 28,000 Tax Rate Exempt 10% 15% 20% Deduction 0.00 180.00 570.00 1,410.00

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

23

Tax Accounting (ACCT-332)

5th 6th 7th

28,20 0 42,60 0 60,00 0

42,600 60,000 *****

25% 30% 35%

2,820.00 4,950.00 7,950.00

Addition Method

Under this method, Rental Income Tax is determined by multiplying any Taxable Rental Income above the minimum level of the Tax Bracket by the tax rate and adding the given addition for each tax bracket as follows: TB Over To Tax Rate Addition st 1 0 1,800 0% Exempt 2nd 1,800 7,800 10% 0.00 rd 3 7,800 16,800 15% 600.00 4th 16,800 28,200 20% 1,950.00 5th 28,200 42,600 25% 4,230.00 6th 42,600 60,000 30% 7,830.00 th 7 60,000 ***** 35% 13,050.00

Rental Income Tax (RIT)

The Rental Income Tax is computed as follows under Addition Method:

RIT = Addition + [(TRI Lower Tax Bracket) @ Marginal Tax Rate] Illustrations on Rental Income Tax Example 3.1: Assume ATO AYELE, the owner of AYU BUILDING, let out (leased) the

Building at Br 2,000,000 per annum. In addition to this, the lessee will incur Br 100,000 cost for repair and maintenance of the building. Assume further that Ato Ayele maintains books of Accounts and the cost of the building is Br 20,000,000 and the following expenses are incurred by the lessor: Cost of Lease payments on Land.......................... Br 100,000 Land and Building Tax.......................................... 4,800 Other Deductible Expenses................................... 5,200 Required: Determine the Gross Rental Income, Taxable Rental Income, and Rental Income Tax

Example 3.2: WELINEGUDENA SHARE COMPANY leased its building for Br 200,000 for

cash per month. The lessor is responsible to make renovation and improvement in the building by incurring Br 100,000 per year as per the lease term. The cost of building is Br 10,000,000 the Share Company paid Br 100,000 for the lease hold Land. Required: Determine Gross Rental Income, Taxable Rental Income and Rental Income Tax Liability

Example 3.3: ATO ZINABU leased his furnished building for Br 2,000 per month and the

equipments and furniture were leased for Br 1,000 per month. He paid Br 1,200 land and building tax to Addis Ababa Municipality. Determine Gross Rental Income, Taxable Rental Income and Rental Income Tax Liability assuming that the house was vacant for four months during tax year 1999

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

24

Chapter Three: Rental Income Tax Accounting

Rental Income Tax Declarations

RIT Declaration with books of accounts (FORM 1201) RIT Lessee Details Declaration and Continuation Sheet (FORM 1202 and FORM 1203) RIT Declaration for taxpayers not maintaining Books of Accounts (FORM 1205 & FORM 1206)

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

25

Tax Accounting (ACCT-332)

Chapter Four Business Income Tax / Business Profit Tax

Chapter Outlines:

Overview of Business Income Tax Legal form businesses and taxable entities Categories of Business taxpayers in Ethiopia Tax accounting methods Business profit tax rate and other legal provisions on Business Profit Tax Deductible Expenses Non-Deductible Expenses Exemptions from Business Profit Tax Accounting for business income tax

Chapter Objectives

After completing this chapter, you would be able to:

Understand what business income tax is Identify taxable entities as per the tax law of the country Know the three different categories of business taxpayers Apply tax accounting methods allowed by the Tax Law currently enforce Differentiate items that are allowed to be deducted from gross income Identify non-deductible expenses Know revenues of incomes exempted from business profit tax Determine taxable business income for different categories of business taxpayers and body and non-body Compute business income tax for small, medium and large businesses Understand the concepts of foreign tax credit, withholding income tax, investment tax credit and loss carry back and carry forward

Time Required: 10 Hours

The legal provisions are taken form Income Tax Proclamation No. 286/2002 and Income Tax Regulation No. 78/2002. 4.1) Legal Forms of Businesses and Taxable Entities

According to Ethiopia: Commercial Code of Ethiopia, there are seven forms of business organizations in Sole Proprietorship It is a taxable entity but not legal entity General Partnership it is both taxable and legal entity Limited Partnership it is both taxable and legal entity Joint Venture - It is a taxable entity but not legal entity Private Limited Company - it is both taxable and legal entity Share Company - it is both taxable and legal entity Co-operative - it is a legal entity but it may or may not be a taxable entity

4.2) Categories of Taxpayers

The categorization of taxpayers depends upon of the following points: a. Annual turnover or annual sales b. Maintenance of accounting records or books of accounts

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

26

Chapter Four: Business Income Tax Accounting

c. d. e. f.

Requirements for registered vouchers, etc Number and types of financial statements to be prepared for tax purposes Tax Year Declaration of Income and time of payment of tax liability

1. Category A Taxpayers a. Category A Taxpayers shall include the following persons and bodies: Any business having an annual turnover of Br 500,000 (Five Hundred Thousand Birr) or more; Any company incorporated under the laws of Ethiopia or in a foreign country Share Companies b. They have to maintain accounting records c. They have to use registered vouchers d. Category A taxpayers shall submit to two statements to the Tax Authority: a balance sheet and a profit & loss statement (income statement) e. The tax year can be either the government fiscal year or the accounting year of the body f. They shall submit the Tax Declaration Form to the Tax Authority within 4 months 2. Category B Taxpayers a. Category B shall include any business having an annual turnover of Br 100,000 and above (100,000 to 499,999.99). b. They have to maintain accounting records c. They have to use registered vouchers d. Category B taxpayers shall submit only a profit and loss statement to the Tax Authority e. The tax year can be either the government fiscal year or the accounting year of the body f. They shall submit the Tax Declaration Form to the Tax Authority within 2 months 3. Category C Taxpayers a. Category C Taxpayers include, unless already classified in Categories A and B, Taxpayer whose annual turnover is estimated by the Tax Authority as being up to Birr 100,000. Category C taxpayers shall pay tax in accordance with Schedule 1 and 2 attached with Regulations No. 78/2002 b. Maintaining books of accounts is encouraged by the Tax Authority for Category C Taxpayers but not mandatory c. They are not required to use registered vouchers d. They are not required to submit any financial statement to the tax authority e. The tax year is the government fiscal year f. Category C taxpayer shall, within the period of 7th day of July to the 6th day of August every tax year, declare to the Tax Authority. One month from the end of the tax year.

4.3) Tax Accounting Methods

A taxpayer shall account for tax purposes on a Cash or Accrual Basis . But, for the purposes of ascertaining a persons income accruing or derived during a tax period, the Timing of Inclusions and Deductions shall be made according to GAAPs and a Company shall account for tax purposes only on an accrual basis. Cash-Basis Accounting revenue is recognized when received and expense is recognized when paid for tax purposes Accrual-Basis Accounting - revenue is recognized when it is earned and expense is recognized when it is incurred.

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

27

Tax Accounting (ACCT-332)

4.4) Business Profit Tax Rate

Business Profit Tax is a tax on income from business activities in Ethiopia. Business Profit is taxed under Schedule C, 30% Flat Tax Rate or Presumptive Tax Assessment 1) Taxable Business Profit of body is taxable at the rate of 30 %. Body shall mean any Company (Pvt. Ltd. Co. and Share Company), Registered Partnership, Any Public Enterprise or Public Financial Agency that carries out business activities 2) Taxable business income of other taxpayers whose annual turnover is Br 100,000 or more shall be taxed in accordance with Schedule C hereunder

Schedule C

Taxable Business Income per Year TB Over Birr To Birr st 1 0 1,800 2nd 1,800 7,800 rd 3 7,800 16,800 4th 16,800 28,000 th 5 28,200 42,600 6th 42,600 60,000 th 7 60,000 ***** Business Income Tax Tax Rate Exempt (0%) 10 15 20 25 30 35

3) Presumptive Tax is a predetermined amount of tax paid by small businesses whose annual sales is less than Br 100,000. The tax is estimated by estimating annual sales (daily sales)

4.5) Deductible Expenses (Allowable Deductions)

Any Direct Costs and expenses of producing the Income is deductible General Concept of deductible expenses. It includes: 1. Insurance Expense 2. Promotional Expense 3. Commissions Expense 4. Payment to Holding or Parent Company 5. General and administrative expenses 6. Salary Expense A. Salary paid to employees B. Salary paid to Management of the Company C. Salary paid to children of business owners 7. Interest Expense Shall not exceed Inter-Bank Interest Rate + 2% A. To lending institutions recognized by the national bank of Ethiopia, B. To foreign banks permitted to lend to enterprises in Ethiopia; C. To shareholders of Companies 8. Donations and Gift Expense 9. Maintenance and Improvement Expense 20% of Depreciation Base 10. Bad Debts Expense (Uncollectible Accounts Expense) 11. Participation deduction (Deduction for Reinvestment of Profit) 12. Special Reserves for Finance Institutions provisions for NPLs 13. Transportation Allowance paid to Employees not exceeding the limit 14. Retirement Benefits less or equal to 15% of the basic salary of the employee 15. Representation Expense 10% of basic salary of employee

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

28

Chapter Four: Business Income Tax Accounting

16. Trading Stock Disposed (Cost of Goods Sold) - The cost of trading stock disposed during a tax period is determined on the basis of the Average Cost Method Example 4.1: BIRTY Share Company has the following beginning and purchased of merchandise Inventory during the Tax Year 1998 (Assume a tax year from Hamle 1 to Sene 30) Date Particulars Quantity Unit Cost Hamle 1, 1997 Beginning Inventory 2,000 100 Tikmet 16, 1998 Purchased Inventory 2,600 110 Megabit 22, 1998 Purchased Inventory 3,000 105 Sene 13, 1998 Purchased Inventory 2,500 106 Required: determine cost of trading stock disposed during the tax assuming that 2,700 units were on hand as of the end of the tax year 17. Depreciation Expense (Article 23) Method of Depreciation for Tax Purposes 1. Fine Art, Antiques, Jewelry, Trading Stock and Other Business shall not be depreciated. 2. The Acquisition or Construction cost, and the cost of Improvement, Renewal and Reconstruction, of buildings and constructions shall be depreciated individually on a straight-line basis at five per cent (5%) 3. The Acquisition or Construction cost, and the cost of Improvement, Renewal and Reconstruction, of intangible assets shall be depreciated individually on a straight-line basis at ten percent (10%) 4. The following two categories of business assets shall be depreciated according to a Pooling System at the following rates: A. Computers, information systems, software products and data storage equipment at twenty five percent (25%) B. All other business assets at twenty percent (20%) Depreciation Base under Pooling Method Depreciation Base during the Tax Year = Book Value at the Beginning + Cost of Assets Acquired Disposal of Assets If the depreciation base is a Negative Amount, that amount shall be added to taxable profit and the depreciation base shall become zero. If the depreciation base does not exceed Br 1,000, the entire depreciation base shall be a deductible business expense

Example 4.2: Assume ABC Spare Parts Pvt. Ltd. Co. uses the Tax Year Hamle 1 to Sene 30

and has the following plant assets: Computers, Information System, Software and Data Storage. Date of Purchase Acquisition Cost Yekatit 10, 1996................................ 16,000 Ginbot 01, 1996................................. 6,000 Nehase 07, 1996................................ 7,000 Tahsas 19, 1997................................. 3,500 Instruction: Compute Depreciation Base and Depreciation Expense for Tax Year Ending Hamle 30, 1996, 1997 and 1998 assuming that ABC Spare Parts Pvt. Ltd. Co. sold old Computer at Birr 3000 on Megabit 23, 1996

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

29

Tax Accounting (ACCT-332)

Example 4.3: The following data were obtained from the accounting records of ZENA Pvt.

Ltd. Co. On Hamle 1, 1997, beginning of the current tax year, the Store Equipment account shows a book value of Birr 170,000. At the beginning of the tax period, the company sold one of the equipments for Birr 25,000 cash and acquired a new one for Birr 85,000 on account. Determine the amount of Depreciation Expense to be recognized on the store equipment and the depreciation base for the store equipment for the tax year ending Sene 30, 1998 as per Art.23 of Income Tax Proclamation No.286/2002

4.6) Non-Deductible Expenses

1. The cost of the acquisition, improvement, renewal and reconstruction of business assets that are depreciated pursuant to Article 23 of EITP No. 286/2002 2. An increase in the share capital of a company or the basic capital of a registered partnership 3. Voluntary pension or provident fund contributions over and above 15% of the monthly salary of the employee 4. Declared dividends and paid-out profit shares 5. Interest in excess of the rate used between the National Bank of Ethiopia and the commercial banks increased by two (2) percentage points 6. Damages covered by insurance policy 7. Punitive damages and penalties 8. The creation or increase of reserves, provisions and other special-purpose funds unless otherwise allowed by this Proclamation; 9. Income Tax paid on Schedule C income and Recoverable or Refundable Value-Added Tax; 10. Representation expenses over and above 10% of basic salary; 11. Personal consumption expenses; 12. Expenditures exceeding the limits set forth in Proclamation No 286 13. Entertainment expenses 14. Donation or gift to other entities not listed in the EITP No 286 15. Sum paid as salary, wages or other personal emoluments to the proprietor or partner of the enterprises and to their spouses 16. Expenditure for maintenance of other private properties of the proprietor or partner of the enterprises 17. Losses not connected with or not arising out of the actively of the enterprise;

4.7) Exemptions

The following categories of income shall be exempt from payment of business income tax hereunder: Awards for adopted or suggested innovations and cost saving measures Public awards for outstanding performance Income specifically exempted from income tax by the law in force in Ethiopia, by international treaty or by an agreement made or approved by the Ministry of Revenue The revenue obtained by the Federal Government, Regional State Governments and Local Governments of Ethiopia; and the National Bank of Ethiopia from activities that are incidental to their operations

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

30

Chapter Four: Business Income Tax Accounting

4.8) Accounting for Business Profit Tax

Accounting for Business Profit Tax is concerned with the following tasks: 1. Computation of Business Profit Tax 2. Determination of Taxable Business Income according the legal Provisions 3. Preparation of Tax Returns i.e. Profit and Loss Account and Balance Sheet 4. Adjusting Business Profit Tax 5. Recording Transactions Related to the Business Tax Liability

4.8.1) Calculation of Business Income Tax

1. Progression Method 2. Deduction Method BIT = Taxable Business Profit @ Marginal Tax Rate Deduction TB 1st 2nd 3rd 4th 5th 6th 7th Over Br 0 1,800 7,800 16,800 28,200 42,600 60,000 To Br 1,800 7,800 16,800 28,000 42,600 60,000 ***** Tax Rate Exempt 10% 15% 20% 25% 30% 35% Deduction 0.00 180.00 570.00 1410.00 2820.00 4950.00 7950.00

3. Addition Method BPT = TBI Lower Tax Bracket @ Marginal Tax Rate + Addition TB 1st 2nd 3rd 4th 5th 6th 7th Over Br 0 1,800 7,800 16,800 28,200 42,600 60,000 To Br 1,800 7,800 16,800 28,000 42,600 60,000 ***** Tax Rate Exempt 10% 15% 20% 25% 30% 35% Addition 0.00 0.00 600.00 1950.00 4230.00 7830.00 13050.00

4.8.2) Determination of Taxable Business Income (Taxable Business Profit)

Taxable business income shall be determined per tax period on the basis of the profit and loss account or income statement, which shall be drawn in compliance with the Generally Accepted Accounting Standards, subject to the provisions of Ethiopian Income Tax Proclamation and the

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

31

Tax Accounting (ACCT-332)

Directives issued by the Tax Authority. Accordingly, the Taxable Business Profit is the can be determined by subtracting costs & expenses from annual revenues. Taxable Business Profit = Annual Revenues Cost of goods sold Operating Expenses Example 4.4: SHALA Merchandising Enterprise is a Category B taxpayer but not a body. The enterprise reported Br 300,000.00 sales revenue; Br 200,000 Cost of goods sold and Br 62,000 operating expenses during the tax year ending Sene 30, 1997. Determine the Taxable Business Income and Business Profit Tax to be paid.

4.8.3) Preparation of Tax Returns

When a business is required to prepare tax returns i.e. profit and loss account and balance sheet, it shall apply the income tax law regarding deductible and non-deductible expenses. The tax returns shall be accompanied by: the amount of business profit tax payable in check or in cash, tax vouchers and documents, and any other relevant information Example 4.5: Assume that the revenue from SAMARITAN Share Company is Br 2,000,000 during Tax Year ended Sene 30, 1997. Cost and Expense were Br 1,000,000 and Br 560,000, respectively. Determine the Taxable Business Profit and Compute the Business Profit Tax Liability of this Share Company preparing a tax return i.e. Profit and Loss Statement.

Example 4.6: Assume Oromia Cooperative Bank Share Company made Br 10,000,000

loans and advances during the tax year ending Sene 30, 1998. Assume also the bank has the following income and expenses for the same Tax Year: Interest Income...........................................................Br 12,000,000 Service Charge Income.............................................. 1,600,000 Interest Expense......................................................... 10,050,000 Administrative and General Expenses....................... 1,600,000 Advertising Expenses................................................. 400,000 Instruction: Determine the Taxable Business Profit of the Bank for the tax year ended Sene 30, 1998 if the technical reserve on the loan and advance was Br 1,300,000.00 and five year tax holiday period for the business.

4.9) Special Items that Reduces Business Profit Tax

There are tax provisions to pay taxes in advance under tax withholding system of the country and tax benefit as a result of loss carry forward and loss carry back. Thus, the business profit tax is adjusted for factors such as Loss Carry Forward and Loss Carry Back; Withholding of Business Profit Tax; Foreign Income Tax Credit and Investment Income Tax Credit.

1. Loss Carry Forward and Loss Carry Back

Loss Carry Back is a tax provision that allows operating losses to be used as a tax shield to reduce taxable income in prior. Loss Carry-Forward is a tax provision that allows operating losses to be used as a tax shield to reduce taxable income of the future years In some countries losses can be carried back and/or forward Example 4.7: MOTERA Trading Share Company reported net sales and Cost & Expense of Birr 1,000,000 and 1,200,000 during the year ended June 30, 2001, respectively. During the year ended June 30, 2002, the same Share Co. reported net sales of Birr 1,500,000 and Cost and

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

32

Chapter Four: Business Income Tax Accounting

Expenses of Br 1,200,000.00. Required: Determine the Taxable Business Income and Business Profit Tax during the tax year ended June 30, 2002 and Record the necessary transaction

2. Withholding Income Tax (Withholding Profit Tax)

A. Collection of withholding Income Tax on Imports 3% of the sum of cost, insurance, and freight (CIF value) B. Withholding of Income Tax on Payments Organization having Legal Personality, Government Agencies, Private Nonprofit Institutions, and Non-Governmental Organizations (NGOs) shall withhold income tax on payments The amount withheld shall be two per cent (2%) of the gross amount of the payment. C. Withholding Scheme Supply of goods involving more than Birr 10,000 in any one transaction or one supply contract; Rendering of the certain services involving more than Birr 500 in any one transaction or one service contract. Example 4.8: TENKER Pvt. Ltd. Co. purchased Birr 200,000 Stationary Materials from HALEHA Stationary Materials Import and Distribution Pvt. Ltd. Co. on Tikmet 18, 1997 Instruction: Record the above transaction for both the seller (withholdee) and buyer (withholder) Withholding Tax Declaration the withholder is required to declare Withholding Income Tax Declaration on monthly basis. Withholding Tax Declaration Form has the following Four Sections: Taxpayer Information; Declaration Details; Tax Declaration Summations; and Taxpayer Certification

3. Foreign Tax Credit and Investment Tax Credit

Both foreign tax credit and investment tax credit are direct reduction from business profit tax to be paid. Foreign tax credit refers to reduction of business profit tax for income tax paid in foreign country from foreign source income. The investment tax credit refers to immediate reduction of business profit tax for some investment made during the tax period. In Ethiopia, there is no tax provision relating to investment tax credit. Businesses can take advantage of foreign tax credit as per Art. 7 or Proclamation No.286/2002

4.10) Computation of TBI from GAAP Based Financial Statements

Amount Amount Particulars In ETB In ETB Taxable Business Profit from GAAP Based Income Statement xxxxx Add: Non-Deductible Expenses (If they are deducted) Depreciation on revalued assets........................................................................................................ xxxxx Above 15% of the basic salary retirement contribution.................................................................... xxxxx Declared dividends and paid-out profit Shares................................................................................. xxxxx Interest in excess of the rate of specified in Proclamation No 286.................................................... xxxxx Damages covered by insurance policy.............................................................................................. xxxxx Punitive damages and penalties........................................................................................................ xxxxx Unallowed provisions and reserves................................................................................................... xxxxx Income tax paid on Schedule C income......................................................................................... xxxxx Recoverable value-added tax............................................................................................................ xxxxx

Compiled By: Kassahun Boressa, AAU, School of Commerce, Revised in 2011

33

Tax Accounting (ACCT-332)