Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Staff Settlement Form - NewDocument9 pagesStaff Settlement Form - NewBaban GaigolePas encore d'évaluation

- Philippine Stock ExchangeDocument25 pagesPhilippine Stock ExchangeJessa Raga-as100% (1)

- Credit Transaction: RD RDDocument4 pagesCredit Transaction: RD RDaya5monteroPas encore d'évaluation

- LP in ABMDocument4 pagesLP in ABMGLICER MANGARON100% (1)

- Univ of Brunei-Statement of PurposeDocument2 pagesUniv of Brunei-Statement of Purposeayu abidinPas encore d'évaluation

- 121CLEPLUGDocument236 pages121CLEPLUGHR20169Pas encore d'évaluation

- Account StatementDocument1 pageAccount Statementzeeshan kkrPas encore d'évaluation

- Chapter 9 - NPA PDFDocument98 pagesChapter 9 - NPA PDFSuraj ChauhanPas encore d'évaluation

- From press-to-ATM - How Money Travels - The Indian ExpressDocument14 pagesFrom press-to-ATM - How Money Travels - The Indian ExpressImad ImadPas encore d'évaluation

- PAM-Assgn 1 - Mariam Fatima Burhan-20181-24727Document5 pagesPAM-Assgn 1 - Mariam Fatima Burhan-20181-24727Mariam Fatima BurhanPas encore d'évaluation

- Liability For Dishonor of Cheques ProjectDocument25 pagesLiability For Dishonor of Cheques ProjectAbhijeet TalwarPas encore d'évaluation

- Procurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.Document28 pagesProcurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.sharang shankerPas encore d'évaluation

- Letter Writing (Formal) For SBI PO, IBPS PO Mains Exams - Set 1Document62 pagesLetter Writing (Formal) For SBI PO, IBPS PO Mains Exams - Set 1Sakshi BhardwajPas encore d'évaluation

- The Impact of Credit Cards On HDFC Bank Customers in Shimoga - An Evaluative StudyDocument9 pagesThe Impact of Credit Cards On HDFC Bank Customers in Shimoga - An Evaluative StudyankitPas encore d'évaluation

- Fybcon Acc Finance 0001 NEWDocument20 pagesFybcon Acc Finance 0001 NEWnishanthreddy89Pas encore d'évaluation

- SBT AR Eng 2011Document92 pagesSBT AR Eng 2011gmp_07Pas encore d'évaluation

- ACF 103 Tutorial 6 Solns Updated 2015Document18 pagesACF 103 Tutorial 6 Solns Updated 2015Carolina SuPas encore d'évaluation

- Westmont Bank V OngDocument4 pagesWestmont Bank V Ongmodernelizabennet100% (4)

- Caiib - Retail Banking (Numerical)Document24 pagesCaiib - Retail Banking (Numerical)RASHMI KUMARIPas encore d'évaluation

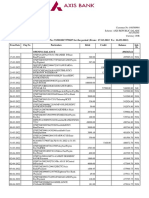

- Statement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Document7 pagesStatement of Axis Account No:913010017379687 For The Period (From: 17-03-2022 To: 16-09-2022)Om Namah ShivayPas encore d'évaluation

- Risk and ReturnDocument3 pagesRisk and ReturnrudrakshiPas encore d'évaluation

- 16 Role of SME in Indian Economoy - Ruchika - FINC004Document22 pages16 Role of SME in Indian Economoy - Ruchika - FINC004Ajeet SinghPas encore d'évaluation

- File CH Tila Worksheet 07Document2 pagesFile CH Tila Worksheet 07Helpin HandPas encore d'évaluation

- NISM V A Sample 500 QuestionsDocument36 pagesNISM V A Sample 500 Questionsbenzene4a183% (35)

- PBP II Chapter 14 Installment PurchasesDocument53 pagesPBP II Chapter 14 Installment PurchasesJorge Luna RamirezPas encore d'évaluation

- Phone Bill (PLDT)Document1 pagePhone Bill (PLDT)Jayson C. LagarePas encore d'évaluation

- Topik 1 Rangka Kerja PerundanganDocument28 pagesTopik 1 Rangka Kerja PerundanganBenjamin Goo KWPas encore d'évaluation

- Commercial Bank Management Sem IIIDocument11 pagesCommercial Bank Management Sem IIIJanvi MhatrePas encore d'évaluation

- Chapter 16 - The Payables LedgerDocument31 pagesChapter 16 - The Payables Ledgershemida100% (3)

- MBBcurrent 564548147990 2022-04-30 PDFDocument7 pagesMBBcurrent 564548147990 2022-04-30 PDFAdeela fazlinPas encore d'évaluation