Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- 581616893-BMO-Bank-Statement-Tina Vennessa MullinsDocument3 pages581616893-BMO-Bank-Statement-Tina Vennessa MullinsAlex NeziPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- All About ChecksDocument5 pagesAll About ChecksCzarina JanePas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Obillos, Jr. vs. Commissioner of Internal Revenue 139 SCRA 436, October 29, 1985Document1 pageObillos, Jr. vs. Commissioner of Internal Revenue 139 SCRA 436, October 29, 1985Clarissa Sawali0% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Billing Invoice Summary ReportDocument2 pagesBilling Invoice Summary ReportAnantha R.K.Pas encore d'évaluation

- A Guide To EMV Chip Technology v3.0 1Document33 pagesA Guide To EMV Chip Technology v3.0 1Jonald NarzabalPas encore d'évaluation

- GR NO 240163 2021 CaseDocument2 pagesGR NO 240163 2021 CaseGRAND LINE GMS100% (1)

- Ubqari Magzine Mar 2018Document60 pagesUbqari Magzine Mar 2018Khalid MahmoodPas encore d'évaluation

- Ubqari Magzine January 2019Document357 pagesUbqari Magzine January 2019Khalid MahmoodPas encore d'évaluation

- Ubqari Magzine May 2018Document68 pagesUbqari Magzine May 2018Khalid MahmoodPas encore d'évaluation

- Al Hub Mahroof Manmohni 2-3Document67 pagesAl Hub Mahroof Manmohni 2-3Khalid MahmoodPas encore d'évaluation

- Ubqari Magzine July 2018Document60 pagesUbqari Magzine July 2018Khalid MahmoodPas encore d'évaluation

- Ubqari Magazine Feb 2018Document62 pagesUbqari Magazine Feb 2018Khalid MahmoodPas encore d'évaluation

- Al Biruni Taqweem 2019Document136 pagesAl Biruni Taqweem 2019Khalid MahmoodPas encore d'évaluation

- RizwanDocument1 pageRizwanKhalid MahmoodPas encore d'évaluation

- Election Appointment of Directors of A CompanyDocument5 pagesElection Appointment of Directors of A CompanyKhalid MahmoodPas encore d'évaluation

- Berger Paints Pakistan: Affairs LTDDocument1 pageBerger Paints Pakistan: Affairs LTDKhalid MahmoodPas encore d'évaluation

- Curriculum Vitae: Page 1 of 1Document1 pageCurriculum Vitae: Page 1 of 1Khalid MahmoodPas encore d'évaluation

- PWCDocument9 pagesPWCKhalid MahmoodPas encore d'évaluation

- Gateway Examination GuideDocument6 pagesGateway Examination GuideKhalid MahmoodPas encore d'évaluation

- Spring 2016 - BNK619 - 4 - MC140401473Document13 pagesSpring 2016 - BNK619 - 4 - MC140401473Khalid MahmoodPas encore d'évaluation

- Management's Assessment Regarding Going Concern AssumptionDocument5 pagesManagement's Assessment Regarding Going Concern AssumptionKhalid MahmoodPas encore d'évaluation

- Saying Astaghfirullah 100 Times Each Takes Only Two MinutesDocument8 pagesSaying Astaghfirullah 100 Times Each Takes Only Two MinutesKhalid MahmoodPas encore d'évaluation

- Bkash: Financial: Technology Innovation For Emerging MarketsDocument8 pagesBkash: Financial: Technology Innovation For Emerging MarketsAditya AnandPas encore d'évaluation

- BAI2 CodesDocument14 pagesBAI2 Codesjinny thakrarPas encore d'évaluation

- Usage Guide - Exclusive PDFDocument36 pagesUsage Guide - Exclusive PDFHemant JainPas encore d'évaluation

- Statement of Receipts and ExpendituresDocument1 pageStatement of Receipts and ExpendituresNorma CanoyPas encore d'évaluation

- Payroll in Excel FormarDocument9 pagesPayroll in Excel Formarcraig_antonioPas encore d'évaluation

- Ic Disc PresentationDocument47 pagesIc Disc PresentationInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910Pas encore d'évaluation

- Sysnova Cyber Security-1Document1 pageSysnova Cyber Security-1Isteak AhmedPas encore d'évaluation

- Ebook Ebook PDF Pearsons Federal Taxation 2018 Individuals 31st Edition PDFDocument41 pagesEbook Ebook PDF Pearsons Federal Taxation 2018 Individuals 31st Edition PDFmichael.johnson225100% (36)

- Gender and Taxation - Bernadette WanjalaDocument17 pagesGender and Taxation - Bernadette WanjalaKwesi_WPas encore d'évaluation

- Summary Philippine Income Tax FormulaDocument25 pagesSummary Philippine Income Tax FormulaDonvidachiye Liwag CenaPas encore d'évaluation

- House No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilDocument6 pagesHouse No L - 1311, Sector 5-B/3, North KARACHI, Karachi Central North Karachi Town Arsalan AkkilMuhammad AhsanPas encore d'évaluation

- E Bay ISAPIDocument2 pagesE Bay ISAPIShivam AroraPas encore d'évaluation

- By:-Rajat Singla Karan Singh Jaideep Singh Nikhil SinghDocument4 pagesBy:-Rajat Singla Karan Singh Jaideep Singh Nikhil Singhrajat_singlaPas encore d'évaluation

- Countrywise Withholding Tax Rates Chart As Per DTAADocument8 pagesCountrywise Withholding Tax Rates Chart As Per DTAAajithaPas encore d'évaluation

- Final Exam Web 1Document10 pagesFinal Exam Web 1Karina LeakesPas encore d'évaluation

- Class 4 QuestionsDocument5 pagesClass 4 Questionsbaqarnaqvi6204Pas encore d'évaluation

- StatementDocument99 pagesStatementmdarsalankhan.hsePas encore d'évaluation

- Employment Slips T4 / RL 1Document35 pagesEmployment Slips T4 / RL 1kanika019Pas encore d'évaluation

- Group-I and Group-II Categories For PG StudentsDocument12 pagesGroup-I and Group-II Categories For PG Studentsjefeena saliPas encore d'évaluation

- Blessing Plastic: Tax Invoice Original For CompanyDocument1 pageBlessing Plastic: Tax Invoice Original For CompanyCharles NaveenPas encore d'évaluation

- Itzcash - Finly Expense Management: We Make Every Penny Ac'Count'Document11 pagesItzcash - Finly Expense Management: We Make Every Penny Ac'Count'vinod1994Pas encore d'évaluation

- Asu 2019-12Document49 pagesAsu 2019-12janinePas encore d'évaluation

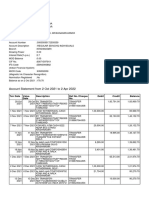

- Account Statement From 2 Oct 2021 To 2 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 2 Oct 2021 To 2 Apr 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceM Eagambaram MunisamyPas encore d'évaluation

- Journal Entries For Engineering StudentsDocument9 pagesJournal Entries For Engineering StudentsSreenivas KodamasimhamPas encore d'évaluation