Vous aimerez peut-être aussi

- 1 2 3 4 5 6 7 8 9 File Name: C:/Courses/Course Materials/3 Templates and Exercises M&A Models/LBO Shell - Xls Colour CodesDocument46 pages1 2 3 4 5 6 7 8 9 File Name: C:/Courses/Course Materials/3 Templates and Exercises M&A Models/LBO Shell - Xls Colour CodesfdallacasaPas encore d'évaluation

- Banking LawsDocument24 pagesBanking LawsPrankyJellyPas encore d'évaluation

- Peter Bernholz - Monetary Regimes and Inflation: History, Economic and Political Relationships (2003)Document225 pagesPeter Bernholz - Monetary Regimes and Inflation: History, Economic and Political Relationships (2003)1236howard100% (1)

- Bank Modeling Guide SampleDocument8 pagesBank Modeling Guide SampleRaphael LeitePas encore d'évaluation

- A Primer On Restructuring Your Company's FinancesDocument9 pagesA Primer On Restructuring Your Company's FinancesLeonardo TeoPas encore d'évaluation

- Unit 01 Introduction To Business FinanceDocument10 pagesUnit 01 Introduction To Business FinanceRuthira Nair AB KrishenanPas encore d'évaluation

- Willmoore Kendall: The Unassimilable Man, by Jeffrey Hart, "National Review," Dec. 31, 1985Document5 pagesWillmoore Kendall: The Unassimilable Man, by Jeffrey Hart, "National Review," Dec. 31, 19851236howardPas encore d'évaluation

- Financial Management - Chapter 1 NotesDocument2 pagesFinancial Management - Chapter 1 Notessjshubham2Pas encore d'évaluation

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingD'EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingPas encore d'évaluation

- Company Kta LawDocument64 pagesCompany Kta LawNishanth VS100% (1)

- The Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionD'EverandThe Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionPas encore d'évaluation

- Capital StructureDocument4 pagesCapital StructurenaveenngowdaPas encore d'évaluation

- 1 - An Overview of Financial ManagementDocument14 pages1 - An Overview of Financial ManagementFawad Sarwar100% (5)

- IAS 23 Borrowing Cost F7Document10 pagesIAS 23 Borrowing Cost F7Maria100% (1)

- Literature and The Economics of Liberty, Edited by Paul A. Cantor and Stephen CoxDocument530 pagesLiterature and The Economics of Liberty, Edited by Paul A. Cantor and Stephen Cox1236howardPas encore d'évaluation

- Assessors HandbookDocument215 pagesAssessors Handbookwbalson100% (1)

- Contemporary Issues in Accounting: Solution ManualDocument17 pagesContemporary Issues in Accounting: Solution ManualDamien SmithPas encore d'évaluation

- Capital Structure Analysis at Bharathi CementDocument21 pagesCapital Structure Analysis at Bharathi Cementferoz khan100% (1)

- Tut 2Document5 pagesTut 2Steffen HoPas encore d'évaluation

- Journal Report: Pay Them in DebtDocument7 pagesJournal Report: Pay Them in DebtgeethkeetsPas encore d'évaluation

- Executive CompensationDocument3 pagesExecutive CompensationmarkdedzPas encore d'évaluation

- ch05 SM RankinDocument17 pagesch05 SM Rankinhasan jabrPas encore d'évaluation

- CFO Initiatief Executive RemunerationDocument7 pagesCFO Initiatief Executive RemunerationPeter KroosPas encore d'évaluation

- Pledge (And Hedge) Allegiance To The CompanyDocument6 pagesPledge (And Hedge) Allegiance To The CompanyBrian TayanPas encore d'évaluation

- Fitch Report - US Corporate Pension PlansDocument8 pagesFitch Report - US Corporate Pension PlansSimon B. AdamsPas encore d'évaluation

- ch05 - SM - Rankin - 2e Theories in AccountingDocument22 pagesch05 - SM - Rankin - 2e Theories in AccountingU2003053 STUDENTPas encore d'évaluation

- Assignment Report Fin544 Sem 3Document12 pagesAssignment Report Fin544 Sem 3Sharil Afiq bin Turiman100% (1)

- Tomato Bank: 2 (A) Criticisms of Remuneration CommitteeDocument5 pagesTomato Bank: 2 (A) Criticisms of Remuneration CommitteeShaheer NaeemPas encore d'évaluation

- MODULE 5 - Issues in Valuing Financial Service FirmsDocument3 pagesMODULE 5 - Issues in Valuing Financial Service Firmschristian garciaPas encore d'évaluation

- Current Liabilities Current (Or Short-Term) Liabilities Are Obligations Whose Settlement Requires The UseDocument4 pagesCurrent Liabilities Current (Or Short-Term) Liabilities Are Obligations Whose Settlement Requires The UseKiki AmeliaPas encore d'évaluation

- AF301 Unit 7 Positive Accounting TheoryDocument41 pagesAF301 Unit 7 Positive Accounting TheoryNarayan DiviyaPas encore d'évaluation

- BBPW3103 - Agency ProblemDocument11 pagesBBPW3103 - Agency ProblemM AdiPas encore d'évaluation

- BKM CH 01 AnswersDocument4 pagesBKM CH 01 AnswersDeepak OswalPas encore d'évaluation

- Capital Structure PolicyDocument7 pagesCapital Structure PolicymakulitnatupaPas encore d'évaluation

- January 2020 Assignment BBPW3103Document14 pagesJanuary 2020 Assignment BBPW3103sandhya raoPas encore d'évaluation

- Tut 4Document12 pagesTut 4Steffen HoPas encore d'évaluation

- SM ch1Document18 pagesSM ch1Arie WidodoPas encore d'évaluation

- Bankruptcy DecisionDocument20 pagesBankruptcy DecisionJeffy JanPas encore d'évaluation

- Deferred Compensation, Risk, and Company ValueDocument38 pagesDeferred Compensation, Risk, and Company ValueSayla SiddiquiPas encore d'évaluation

- Aefman Module 1 5Document28 pagesAefman Module 1 5TUGADE, AMADOR EMMANUELLE R.Pas encore d'évaluation

- Report - FonterraDocument19 pagesReport - FonterraK59 DOAN THANH TAMPas encore d'évaluation

- Tutorial 6 SolutionsDocument4 pagesTutorial 6 Solutionsmerita homasiPas encore d'évaluation

- Q1) Define The Meaning of Agency Theory?Document8 pagesQ1) Define The Meaning of Agency Theory?vivek1119Pas encore d'évaluation

- 15.963 Management Accounting and Control: Mit OpencoursewareDocument21 pages15.963 Management Accounting and Control: Mit OpencoursewareFernando Miguel De StefanoPas encore d'évaluation

- Factors Affecting Capital Structure: (A) Internal Factors (B) External Factors (C) General FactorsDocument4 pagesFactors Affecting Capital Structure: (A) Internal Factors (B) External Factors (C) General Factorsshri277Pas encore d'évaluation

- Financial MGMTDocument13 pagesFinancial MGMTBen AzarelPas encore d'évaluation

- Chapter 1 - Overview of Financial ManagementDocument4 pagesChapter 1 - Overview of Financial Management132345usdfghjPas encore d'évaluation

- Agency Problems and Executive Compensation: Corporate Finance, 3eDocument19 pagesAgency Problems and Executive Compensation: Corporate Finance, 3eSandip SurekaPas encore d'évaluation

- Investment Management Fee Structures: Act IIDocument7 pagesInvestment Management Fee Structures: Act IIStefan Whitwell, CFA, CIPMPas encore d'évaluation

- C30CY Week 8 LectureDocument50 pagesC30CY Week 8 Lecturejohnshabin123Pas encore d'évaluation

- Business Finance NotesDocument42 pagesBusiness Finance Noteskaiephrahim663Pas encore d'évaluation

- Tutorial in Week 11 (Based On Week 10 Lecture) Beginning 14 May 2018 TOPIC: Executive Compensation Solutions Q1 AttachedDocument5 pagesTutorial in Week 11 (Based On Week 10 Lecture) Beginning 14 May 2018 TOPIC: Executive Compensation Solutions Q1 AttachedhabibPas encore d'évaluation

- Fundamentals of Advanced Accounting 4Th Edition Hoyle Solutions Manual Full Chapter PDFDocument67 pagesFundamentals of Advanced Accounting 4Th Edition Hoyle Solutions Manual Full Chapter PDFhorsecarbolic1on100% (12)

- Fundamentals of Advanced Accounting 4th Edition Hoyle Solutions ManualDocument49 pagesFundamentals of Advanced Accounting 4th Edition Hoyle Solutions Manualeffigiesbuffoonmwve9100% (27)

- Chap 006Document51 pagesChap 006kel458100% (1)

- Capital Structure - Bharati CementDocument14 pagesCapital Structure - Bharati CementMohmmedKhayyumPas encore d'évaluation

- Pension Finance AssingmentDocument3 pagesPension Finance AssingmentFridah ApondiPas encore d'évaluation

- P4AFM SQB As - d09 PDFDocument108 pagesP4AFM SQB As - d09 PDFTaariq Abdul-MajeedPas encore d'évaluation

- 5004 Seminar 1 - AnswersDocument5 pages5004 Seminar 1 - AnswershichichicPas encore d'évaluation

- Ge Entrep Activity 2 (Sayre)Document4 pagesGe Entrep Activity 2 (Sayre)Cyrell Malmis SayrePas encore d'évaluation

- Long-Term CapitalDocument13 pagesLong-Term Capitalafoninadin81Pas encore d'évaluation

- 7.1. Source of Project FinanceDocument7 pages7.1. Source of Project FinanceTemesgenPas encore d'évaluation

- FM Unit 3Document9 pagesFM Unit 3ashraf hussainPas encore d'évaluation

- FM ExamDocument13 pagesFM Examtigist abebePas encore d'évaluation

- FM 101 SG 1Document5 pagesFM 101 SG 1Evalend SaltingPas encore d'évaluation

- Managerial Finance in a Canadian Setting: Instructor's ManualD'EverandManagerial Finance in a Canadian Setting: Instructor's ManualPas encore d'évaluation

- 07 Political SituationDocument13 pages07 Political Situation1236howardPas encore d'évaluation

- 07.10.07 Volcker On ReformDocument8 pages07.10.07 Volcker On Reform1236howardPas encore d'évaluation

- PNP Nup Loan Application Form and Promissory NoteDocument2 pagesPNP Nup Loan Application Form and Promissory NoteEnteng Teng TengitsPas encore d'évaluation

- Lesson 13-COT 4TH QUARTERDocument40 pagesLesson 13-COT 4TH QUARTERmaria genioPas encore d'évaluation

- Ch-30 Money Growth & InflationDocument37 pagesCh-30 Money Growth & InflationSnehal BhattPas encore d'évaluation

- Time Value of Money: All Rights ReservedDocument50 pagesTime Value of Money: All Rights ReservedHasib NaheenPas encore d'évaluation

- The British Money MarketDocument2 pagesThe British Money MarketAshis karmakarPas encore d'évaluation

- Laos 1003 Eu-Laos Ipip MT199 110221Document22 pagesLaos 1003 Eu-Laos Ipip MT199 110221TerenzPas encore d'évaluation

- Transaction Disbursement Form-VIDA NufindataDocument2 pagesTransaction Disbursement Form-VIDA NufindataPharmastar Int'l Trading Corp.Pas encore d'évaluation

- Assignment 8 - Geas: InstructionDocument4 pagesAssignment 8 - Geas: InstructionJhoe TangoPas encore d'évaluation

- Top Reasons Why You Should Invest in Patricia Executive VillageDocument10 pagesTop Reasons Why You Should Invest in Patricia Executive VillagekonyatanPas encore d'évaluation

- Contact: 8 Ikeja Close, Off Oyo Street Garki Area 2, Abuja. 08099997661 07033058663 09022220513Document12 pagesContact: 8 Ikeja Close, Off Oyo Street Garki Area 2, Abuja. 08099997661 07033058663 09022220513Chigoziri ArinzePas encore d'évaluation

- Busmath K76 Self-Check Exercise 1.1: Brian Chuahiock Charmaine Gozon Kath Parungao Seoyeon Choi Juliann SabaterDocument7 pagesBusmath K76 Self-Check Exercise 1.1: Brian Chuahiock Charmaine Gozon Kath Parungao Seoyeon Choi Juliann SabaterJuliann SabaterPas encore d'évaluation

- FNCE 317 Formula Sheet - FinalDocument2 pagesFNCE 317 Formula Sheet - FinalDon JonesPas encore d'évaluation

- CH 13Document20 pagesCH 13Muhammad3786Pas encore d'évaluation

- YEBABE Final MBA Paper - REVIESDDocument59 pagesYEBABE Final MBA Paper - REVIESDamognePas encore d'évaluation

- IM in ENSC-20093-ENGINEERING-ECONOMICS-TAPAT #CeaDocument73 pagesIM in ENSC-20093-ENGINEERING-ECONOMICS-TAPAT #CeaAHSTERIPas encore d'évaluation

- Members Loan Balance Import TemplateDocument77 pagesMembers Loan Balance Import TemplateSamuelPas encore d'évaluation

- Money MarketDocument8 pagesMoney MarketMAMTA WAGHPas encore d'évaluation

- Chapter - 4 Exchange Rate DeterminationDocument14 pagesChapter - 4 Exchange Rate DeterminationAshiqur RahmanPas encore d'évaluation

- 31 QuestionsDocument30 pages31 QuestionsAmira SallehPas encore d'évaluation

- DocxDocument9 pagesDocxReiah RongavillaPas encore d'évaluation

- Repo RateDocument5 pagesRepo RateSweta SinghPas encore d'évaluation

- CCP Rbi Jul-Dec'23Document21 pagesCCP Rbi Jul-Dec'23RaviTuduPas encore d'évaluation

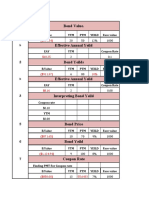

- Bond Value.: B.Value YTM PTM Yeild Face ValueDocument4 pagesBond Value.: B.Value YTM PTM Yeild Face ValueshabywarriachPas encore d'évaluation

- 4th Weekly TestsDocument9 pages4th Weekly TestsAdrian F. CapilloPas encore d'évaluation