Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Indian Market WizardsDocument108 pagesThe Indian Market WizardsRajendra100% (2)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Contractual IndemnitiesDocument481 pagesContractual IndemnitiesUrvashi JaswaniPas encore d'évaluation

- Moneypati Options OI Sheet Link Password PDFDocument10 pagesMoneypati Options OI Sheet Link Password PDFSHOEBPas encore d'évaluation

- Investing in Resilience: Ensuring A Disaster-Resistant FutureDocument188 pagesInvesting in Resilience: Ensuring A Disaster-Resistant FutureAsian Development BankPas encore d'évaluation

- Variable Production Overhead Variance (VPOH)Document9 pagesVariable Production Overhead Variance (VPOH)Wee Han ChiangPas encore d'évaluation

- HO, B & A AcctgDocument15 pagesHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- A Survey of Semiconductor Supply Chain Models IIDocument20 pagesA Survey of Semiconductor Supply Chain Models IINiraj KumarPas encore d'évaluation

- Demand Planning ConfigurationDocument49 pagesDemand Planning ConfigurationSapanalyst94% (18)

- Breach of Obligation - Vasquez V Ayala Corporation Case DigestDocument2 pagesBreach of Obligation - Vasquez V Ayala Corporation Case DigestKyra Sy-Santos100% (2)

- Civil - G.R. No. 200383 - DigestDocument2 pagesCivil - G.R. No. 200383 - Digestjireh bacsPas encore d'évaluation

- Cashless ProcessDocument3 pagesCashless ProcessNiraj KumarPas encore d'évaluation

- Resotrading - Nifty Futures Positional Trading Rules - v2Document2 pagesResotrading - Nifty Futures Positional Trading Rules - v2Niraj KumarPas encore d'évaluation

- 3.1 Guidelines For Dealer Self Evaluation - ServiceDocument4 pages3.1 Guidelines For Dealer Self Evaluation - ServiceNiraj KumarPas encore d'évaluation

- 3.0 Dealer Self Evaluation Sheet - ServiceDocument1 page3.0 Dealer Self Evaluation Sheet - ServiceNiraj KumarPas encore d'évaluation

- Dealer Self Evaluation Sheet - SalesDocument1 pageDealer Self Evaluation Sheet - SalesNiraj KumarPas encore d'évaluation

- Safety Stock or Safety Lead TimeDocument20 pagesSafety Stock or Safety Lead TimeNiraj KumarPas encore d'évaluation

- 11th Feb 3rd Edition Demand Planning Forecasting Summit Awards 2020Document6 pages11th Feb 3rd Edition Demand Planning Forecasting Summit Awards 2020Niraj KumarPas encore d'évaluation

- Criticality: Token NoDocument6 pagesCriticality: Token NoNiraj KumarPas encore d'évaluation

- Business / User Requirement Capturing Form: PurposeDocument2 pagesBusiness / User Requirement Capturing Form: PurposeNiraj KumarPas encore d'évaluation

- Proposal For Safety Reporting - V2Document6 pagesProposal For Safety Reporting - V2Niraj KumarPas encore d'évaluation

- CRTS Screen ShotDocument5 pagesCRTS Screen ShotNiraj KumarPas encore d'évaluation

- Joint Optimisation of Capacity and Safety Stock AllocationDocument18 pagesJoint Optimisation of Capacity and Safety Stock AllocationNiraj KumarPas encore d'évaluation

- The MES Performance Advantage Best of The Best Plants Use MESDocument20 pagesThe MES Performance Advantage Best of The Best Plants Use MESNiraj KumarPas encore d'évaluation

- Safety Stock Calculations and Inventory AnalysisDocument15 pagesSafety Stock Calculations and Inventory AnalysisNiraj KumarPas encore d'évaluation

- Safety Stock Determination Based On Parametric Lead Time and Demand InformationDocument19 pagesSafety Stock Determination Based On Parametric Lead Time and Demand InformationNiraj KumarPas encore d'évaluation

- Dynamic Planned Safety Stocks in Supply Network PDFDocument23 pagesDynamic Planned Safety Stocks in Supply Network PDFNiraj KumarPas encore d'évaluation

- Life SavingsDocument25 pagesLife SavingsNiraj KumarPas encore d'évaluation

- NewDocument1 pageNewNiraj KumarPas encore d'évaluation

- An Inventory Management Approximation For For Estimated Aggregated Regional Food Stock LevelsDocument18 pagesAn Inventory Management Approximation For For Estimated Aggregated Regional Food Stock LevelsNiraj KumarPas encore d'évaluation

- Life Cycle Planning in SAP APO. Business Process Part-2Document6 pagesLife Cycle Planning in SAP APO. Business Process Part-2Niraj KumarPas encore d'évaluation

- Action Plan - Demand & Supply PlanningDocument7 pagesAction Plan - Demand & Supply PlanningNiraj KumarPas encore d'évaluation

- Outstation Travel Expense Voucher-Feb19Document1 pageOutstation Travel Expense Voucher-Feb19Niraj KumarPas encore d'évaluation

- Claim Intimation FormatDocument2 pagesClaim Intimation FormatNiraj KumarPas encore d'évaluation

- BRD - LFAD and NCPD DancingDocument3 pagesBRD - LFAD and NCPD DancingNiraj KumarPas encore d'évaluation

- Worksheet in D Projects Ongoing eDCM Dancing LFAD BRD - LFAD and NCPD DancingDocument30 pagesWorksheet in D Projects Ongoing eDCM Dancing LFAD BRD - LFAD and NCPD DancingNiraj KumarPas encore d'évaluation

- Iron Fly StrategyDocument11 pagesIron Fly StrategyNiraj KumarPas encore d'évaluation

- A CASE STUDY OF EVEREST BANK LIMITED Mbs ThesisDocument74 pagesA CASE STUDY OF EVEREST BANK LIMITED Mbs Thesisशिवम कर्ण100% (1)

- Demo 04 - Journal Entries & Ledger Posting & T.B. - Rizvi Co (Compatibility Mode)Document31 pagesDemo 04 - Journal Entries & Ledger Posting & T.B. - Rizvi Co (Compatibility Mode)Evergreen FosterPas encore d'évaluation

- Formation of Joint Stock CompanyDocument5 pagesFormation of Joint Stock CompanyHemchandra PatilPas encore d'évaluation

- L03-DLP-Financial InsitutionDocument4 pagesL03-DLP-Financial InsitutionKim Mei HuiPas encore d'évaluation

- Case - A Survey of Capital Budgeting Techniques by US FirmsDocument8 pagesCase - A Survey of Capital Budgeting Techniques by US FirmsYatin PushkarnaPas encore d'évaluation

- Legal and Regulatory Frame Work of Merger & AquiDocument14 pagesLegal and Regulatory Frame Work of Merger & Aquimanishsingh6270Pas encore d'évaluation

- CH 22 Acc Changes & Error Edited PDFDocument65 pagesCH 22 Acc Changes & Error Edited PDFStefanPas encore d'évaluation

- E CircularDocument3 pagesE Circularkethan kumarPas encore d'évaluation

- Case Study South Dakota MicrobreweryDocument1 pageCase Study South Dakota Microbreweryjman02120Pas encore d'évaluation

- The Guide To Worry Free Investing VectorvestDocument10 pagesThe Guide To Worry Free Investing VectorvestDdasfda DsafasdfPas encore d'évaluation

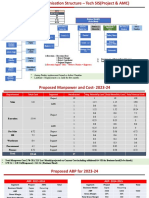

- Proposed Org Chart - Tech SIS.Document5 pagesProposed Org Chart - Tech SIS.Santosh KumarPas encore d'évaluation

- Lot Sizes Vs Risk in Forex SimplifiedDocument14 pagesLot Sizes Vs Risk in Forex SimplifiedTeju OniPas encore d'évaluation

- Infographic Fin 533 (2021)Document3 pagesInfographic Fin 533 (2021)Nurul AlyaPas encore d'évaluation

- The Basic Tools of FinanceDocument25 pagesThe Basic Tools of FinanceVivek KediaPas encore d'évaluation

- Kotak Mahindra Bank Limited Standalone Financials FY18Document72 pagesKotak Mahindra Bank Limited Standalone Financials FY18Shankar ShridharPas encore d'évaluation

- Bucharest Hotel ProjectsDocument8 pagesBucharest Hotel ProjectsLili LewhittePas encore d'évaluation

- Scope of Livestock InsuranceDocument16 pagesScope of Livestock InsuranceAjaz HussainPas encore d'évaluation

- 11 NIQ Soil Testing PatharkandiDocument2 pages11 NIQ Soil Testing Patharkandiexecutive engineer1Pas encore d'évaluation

- Item Wise Boq: (Domestic Tenders - Rates Are To Given in Rupees (Inr) Only)Document3 pagesItem Wise Boq: (Domestic Tenders - Rates Are To Given in Rupees (Inr) Only)RAMAN SHARMAPas encore d'évaluation

- Profit Planning: Cost-Volume-Profit Analysis and Decision MakingDocument36 pagesProfit Planning: Cost-Volume-Profit Analysis and Decision MakingDhim PlePas encore d'évaluation

- Community and Management Skills TrainingDocument42 pagesCommunity and Management Skills TrainingAdnan AkramPas encore d'évaluation

- Redemption of Preference SharesDocument19 pagesRedemption of Preference SharesAshura ShaibPas encore d'évaluation

- Financial Accounting II - MGT401 Spring 2012 Mid Term Solved QuizDocument21 pagesFinancial Accounting II - MGT401 Spring 2012 Mid Term Solved Quizsania.mahar0% (1)

- Case-Study - Laura Ashley.Document16 pagesCase-Study - Laura Ashley.inesvilafanhaPas encore d'évaluation