Vous aimerez peut-être aussi

- A Policyholder's Primer On Commercial InsuranceDocument211 pagesA Policyholder's Primer On Commercial Insurancepauljosephwhiteyahoo.comPas encore d'évaluation

- Audit Work Program TemplateDocument64 pagesAudit Work Program TemplateleonciongPas encore d'évaluation

- Generated Leads For State FarmDocument12 pagesGenerated Leads For State Farmapi-19783206Pas encore d'évaluation

- Preparation Audit ProgramDocument8 pagesPreparation Audit ProgramJem VadilPas encore d'évaluation

- Accounts PayableExpense Accounting Audit Work ProgramDocument5 pagesAccounts PayableExpense Accounting Audit Work ProgrammohamedciaPas encore d'évaluation

- Internal Audit Charter and Operating StandardsDocument7 pagesInternal Audit Charter and Operating Standardssinra07Pas encore d'évaluation

- Expense PurchasesDocument29 pagesExpense PurchasesAshPas encore d'évaluation

- General Vs BarramedaDocument11 pagesGeneral Vs BarramedaShivaPas encore d'évaluation

- Audit Procedure of InventoryDocument3 pagesAudit Procedure of Inventoryd_idayu87Pas encore d'évaluation

- Audit Program For Inventory RisksDocument4 pagesAudit Program For Inventory RisksCrystal Chow100% (1)

- Hartford Payroll Audit ReportDocument10 pagesHartford Payroll Audit ReportkevinhfdPas encore d'évaluation

- Procurement Audit SampleDocument13 pagesProcurement Audit SampleCyrile Dianne Therese Ablir-BaliolaPas encore d'évaluation

- Fixed Assets Policy and Procedure ManualDocument60 pagesFixed Assets Policy and Procedure ManualArup DattaPas encore d'évaluation

- Internal Audit Plan & ScheduleDocument9 pagesInternal Audit Plan & SchedulezamanbdPas encore d'évaluation

- Citi BankDocument21 pagesCiti BankVysakh PkPas encore d'évaluation

- Purchasing Payables ControlDocument9 pagesPurchasing Payables ControljenjenheartsdanPas encore d'évaluation

- Module1 Internal Control Checklist en 0Document12 pagesModule1 Internal Control Checklist en 0Mohammad Abd Alrahim ShaarPas encore d'évaluation

- Empleyado Brochure PDFDocument3 pagesEmpleyado Brochure PDFRose ManaloPas encore d'évaluation

- MYOB AccountingDocument114 pagesMYOB Accountingmukarromin100% (1)

- Test of Control Working PaperDocument4 pagesTest of Control Working PaperMich Angeles50% (2)

- 3 Audit Files and Working PapersDocument11 pages3 Audit Files and Working PapersMoffat MakambaPas encore d'évaluation

- Cash Handling IcqDocument5 pagesCash Handling IcqpalaviyaPas encore d'évaluation

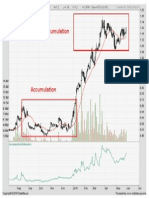

- Darvas Box SummaryDocument7 pagesDarvas Box SummaryVijayPas encore d'évaluation

- Audit Working Papers: By: Tariq MahmoodDocument38 pagesAudit Working Papers: By: Tariq MahmoodMazhar Hussain Ch.Pas encore d'évaluation

- BAICS AppendixesDocument7 pagesBAICS AppendixesDenmark CostanillaPas encore d'évaluation

- Audit of Property, Plant, and Equipment - Hahu Zone - 1622367787308Document8 pagesAudit of Property, Plant, and Equipment - Hahu Zone - 1622367787308Iam AbdiwaliPas encore d'évaluation

- Compliance Test Program: State Accounting OfficeDocument10 pagesCompliance Test Program: State Accounting OfficeChristen CastilloPas encore d'évaluation

- Sample Audit Program - Cash Disbursing OfficersDocument3 pagesSample Audit Program - Cash Disbursing OfficersYnnejesor Aruges100% (1)

- Audit Program For Fixed Assets: Form AP 35Document9 pagesAudit Program For Fixed Assets: Form AP 35Adrianna LenaPas encore d'évaluation

- Field Finance Manual 2010Document135 pagesField Finance Manual 2010Muhammad Zaki83% (6)

- Trade PayableDocument7 pagesTrade PayablemnhammadPas encore d'évaluation

- Purchasing Audit ProgrammeDocument12 pagesPurchasing Audit ProgrammemercymabPas encore d'évaluation

- Sample Audit ProgramDocument119 pagesSample Audit ProgramEcyojEiramMarapaoPas encore d'évaluation

- Fixed Assets PolicyDocument19 pagesFixed Assets PolicyLouiePas encore d'évaluation

- Physical Inventory Observation Checklist-Fixed AssetsDocument7 pagesPhysical Inventory Observation Checklist-Fixed AssetsCreanga Georgian100% (1)

- AUDIT PROGRAM For Cash Disbursements 2Document5 pagesAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedPas encore d'évaluation

- Audit of Fixed Assets 1Document3 pagesAudit of Fixed Assets 1Leon MushiPas encore d'évaluation

- 2017 9 Audit Observations and RecommendationsDocument79 pages2017 9 Audit Observations and RecommendationsKean Fernand BocaboPas encore d'évaluation

- CSMSI Cash Handling PolicyDocument3 pagesCSMSI Cash Handling PolicyJayson MaleroPas encore d'évaluation

- 2011 11 16 - SMRC - Sales and Marketing - Audit ReportDocument10 pages2011 11 16 - SMRC - Sales and Marketing - Audit ReportNayan GuptaPas encore d'évaluation

- H001 - Intro To Internal AuditingDocument12 pagesH001 - Intro To Internal AuditingKevin James Sedurifa OledanPas encore d'évaluation

- W.P BSAccount RecDocument2 pagesW.P BSAccount RecnaimaPas encore d'évaluation

- Accounting Receivables and PayablesDocument14 pagesAccounting Receivables and PayablesDiego EspinozaPas encore d'évaluation

- Petty Cash /imprest Reimbursement Post Audit ChecklistDocument2 pagesPetty Cash /imprest Reimbursement Post Audit ChecklistHenry Mapa100% (1)

- Key Internal ControlDocument5 pagesKey Internal ControlBarkah Wahyu PrasetyoPas encore d'évaluation

- Working Paper For Audit Procedures and EmailDocument3 pagesWorking Paper For Audit Procedures and EmailGiven RefilwePas encore d'évaluation

- Audit WorksheetDocument7 pagesAudit WorksheetEricXiaojinWangPas encore d'évaluation

- Internal Audit Manual TemperedDocument29 pagesInternal Audit Manual TemperedMan Singh100% (1)

- Audit Program 1 PDFDocument3 pagesAudit Program 1 PDFHimanshu GaurPas encore d'évaluation

- Audit of Sales and ReceivablesDocument5 pagesAudit of Sales and ReceivablesTilahun S. Kura100% (1)

- Audit Program For Accounts Receivable and Sales Client Name: Date of Financial Statements: Iii. Accounts Receivable and SalesDocument6 pagesAudit Program For Accounts Receivable and Sales Client Name: Date of Financial Statements: Iii. Accounts Receivable and SalesFatima MacPas encore d'évaluation

- Implementing A Procurement Internal Audit ProgramDocument10 pagesImplementing A Procurement Internal Audit ProgramFaruk H. IrmakPas encore d'évaluation

- General Internal Audit ModelDocument5 pagesGeneral Internal Audit ModelSoko A. KamaraPas encore d'évaluation

- Internal Control QuestionnaireDocument1 pageInternal Control QuestionnaireNicole Megan AmacanPas encore d'évaluation

- Yes No Comments A. Organizational Background and GovernanceDocument12 pagesYes No Comments A. Organizational Background and GovernanceJennifer Constantino DulayPas encore d'évaluation

- Cop Safely Remove AsbestosDocument72 pagesCop Safely Remove AsbestostenglumlowPas encore d'évaluation

- 09 - Cash and Bank BalancesDocument4 pages09 - Cash and Bank BalancesAqib SheikhPas encore d'évaluation

- Credit Card DetailsDocument5 pagesCredit Card DetailsSyed Farid AliPas encore d'évaluation

- Fixed Assets PolicyDocument3 pagesFixed Assets PolicyShinil Nambrath100% (1)

- Doctrine of TracingDocument34 pagesDoctrine of TracingAkmal SafwanPas encore d'évaluation

- K AP 3 Capital Work in ProgressDocument5 pagesK AP 3 Capital Work in Progresssibuna151Pas encore d'évaluation

- Visa Fee For AustraliaDocument11 pagesVisa Fee For AustraliaShaifur RahmanPas encore d'évaluation

- Management Representation AaaDocument3 pagesManagement Representation AaaFaizan AlhamdPas encore d'évaluation

- Procurement IcqDocument8 pagesProcurement IcqzuldvsbPas encore d'évaluation

- Aud. Program - Accounts PayableDocument6 pagesAud. Program - Accounts PayableRalph Christer MaderazoPas encore d'évaluation

- Management of A Public Accounting Firm: Professional FeesDocument18 pagesManagement of A Public Accounting Firm: Professional FeesLaiza Mechelle Roxas MacaraigPas encore d'évaluation

- Audit Program-Cash FundsDocument2 pagesAudit Program-Cash FundsCristina RosalPas encore d'évaluation

- Audit of Bank and CashDocument4 pagesAudit of Bank and CashIftekhar IftePas encore d'évaluation

- Cut-Off For Inventory/Stocks RisksDocument4 pagesCut-Off For Inventory/Stocks RisksSultan RanaPas encore d'évaluation

- InventoryDocument4 pagesInventoryPrio DebnathPas encore d'évaluation

- Pav CourseDocument30 pagesPav CoursetenglumlowPas encore d'évaluation

- Analyzing Gaps For Profitable Trading StrategiesDocument31 pagesAnalyzing Gaps For Profitable Trading StrategiestenglumlowPas encore d'évaluation

- Gst-01c - Details of Overseas PrincipalDocument7 pagesGst-01c - Details of Overseas PrincipaltenglumlowPas encore d'évaluation

- GST 02 - Application For Group or Joint Venture RegistrationDocument8 pagesGST 02 - Application For Group or Joint Venture RegistrationtenglumlowPas encore d'évaluation

- White Card Online - CPCCOHS1001A - WhiteCard Online - Narbil White CardDocument3 pagesWhite Card Online - CPCCOHS1001A - WhiteCard Online - Narbil White CardtenglumlowPas encore d'évaluation

- Gst-01 - Application For Goods and Services Tax Registration Revised 3 Okt 2014Document9 pagesGst-01 - Application For Goods and Services Tax Registration Revised 3 Okt 2014tenglumlowPas encore d'évaluation

- Strategy Note - Must-Own Stocks For Long-Term InvestingDocument139 pagesStrategy Note - Must-Own Stocks For Long-Term InvestingtenglumlowPas encore d'évaluation

- 1MDB Wants Money To Come Back To Malaysia But What Kind of Returns Would The Investments Have Yielded - Business News - The Star OnlineDocument13 pages1MDB Wants Money To Come Back To Malaysia But What Kind of Returns Would The Investments Have Yielded - Business News - The Star OnlinetenglumlowPas encore d'évaluation

- Royal Malaysian Customs: Guide Approved Toll Manufacturer SchemeDocument15 pagesRoyal Malaysian Customs: Guide Approved Toll Manufacturer SchemetenglumlowPas encore d'évaluation

- Royal Malaysian Customs: Guide Approved Trader SchemeDocument16 pagesRoyal Malaysian Customs: Guide Approved Trader SchemetenglumlowPas encore d'évaluation

- EvergreenDocument1 pageEvergreentenglumlowPas encore d'évaluation

- SSM Illustration of FS MFRSDocument76 pagesSSM Illustration of FS MFRStenglumlowPas encore d'évaluation

- DoorsDocument18 pagesDoorstenglumlow100% (1)

- Guidebook Import Export 1Document279 pagesGuidebook Import Export 1tenglumlowPas encore d'évaluation

- Camel Rating ModalDocument114 pagesCamel Rating Modalaparnaankit100% (2)

- Kuwait - Mohamed IqbalDocument18 pagesKuwait - Mohamed IqbalAsian Development Bank50% (2)

- Vip ReceiptDocument16 pagesVip Receiptvanita kunnoPas encore d'évaluation

- Summary and Conclusions: Chapter Review and Self-Test ProblemsDocument4 pagesSummary and Conclusions: Chapter Review and Self-Test ProblemsSyed Asim AliPas encore d'évaluation

- Greenfield Airport Development in India: A Case Study of Bangalore International AirportDocument31 pagesGreenfield Airport Development in India: A Case Study of Bangalore International AirportAnil Kumar Nayak100% (1)

- About MCBDocument2 pagesAbout MCBtwinklingcoronaPas encore d'évaluation

- Kantox FX Guide For CFODocument20 pagesKantox FX Guide For CFOfcatalaoPas encore d'évaluation

- Mrunal Economy2019 PDFDocument194 pagesMrunal Economy2019 PDFShrikantKadam100% (1)

- Finance of International Trade Related Treasury OperationsDocument1 pageFinance of International Trade Related Treasury OperationsMuhammad KamranPas encore d'évaluation

- Effect of Electronic Banking On Financial Performance of Deposit Taking Micro Finance Institutions in Kisii TownDocument5 pagesEffect of Electronic Banking On Financial Performance of Deposit Taking Micro Finance Institutions in Kisii TownIOSRjournalPas encore d'évaluation

- eGRAS Raj Nic inDocument1 pageeGRAS Raj Nic inPratik GuptaPas encore d'évaluation

- Easypaisa Money Transfer To Any Mobile NumberDocument2 pagesEasypaisa Money Transfer To Any Mobile NumberBryan WalkerPas encore d'évaluation

- 2551QDocument3 pages2551QJerry Bantilan JrPas encore d'évaluation

- Introduction of Financial InstitutionDocument12 pagesIntroduction of Financial InstitutionGanesh Kumar100% (2)

- A Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BankDocument67 pagesA Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BanklalsinghPas encore d'évaluation

- BlackstoneDocument2 pagesBlackstoneaidem100% (2)

- FIN036 AssignmentDocument25 pagesFIN036 AssignmentSandeep BholahPas encore d'évaluation

- Depositry Service TinuDocument76 pagesDepositry Service TinunainakhushbooPas encore d'évaluation

- PESONet ParticipantsDocument2 pagesPESONet ParticipantsKylene Maranan VillamarPas encore d'évaluation

- Blue Chip Stocks TipsDocument16 pagesBlue Chip Stocks TipsPinal MehtaPas encore d'évaluation

- A01 Summer Training Project Report: Marketing MixDocument56 pagesA01 Summer Training Project Report: Marketing MixJaiHanumankiPas encore d'évaluation