Vous aimerez peut-être aussi

- Doe Website SummaryDocument6 pagesDoe Website Summaryapi-300447815Pas encore d'évaluation

- Local Financial Impact Review - Municipal Cost Impacts of Massachusettss HotelMotel-Based Homeless Families Shelter Program PDFDocument68 pagesLocal Financial Impact Review - Municipal Cost Impacts of Massachusettss HotelMotel-Based Homeless Families Shelter Program PDFMassLivePas encore d'évaluation

- Still Building InequalityDocument7 pagesStill Building InequalitynechartersPas encore d'évaluation

- The Truth About Education FundingDocument2 pagesThe Truth About Education FundingKim SchmidtnerPas encore d'évaluation

- IDC School Mandate Relief ReportDocument8 pagesIDC School Mandate Relief ReportRich AzzopardiPas encore d'évaluation

- Christina School District Legislative BriefingDocument16 pagesChristina School District Legislative BriefingKevinOhlandtPas encore d'évaluation

- Debt Service Equalization February Legislative SesssionDocument17 pagesDebt Service Equalization February Legislative Sesssionapi-306876736Pas encore d'évaluation

- Quarterly Deficit District Report December 2015Document10 pagesQuarterly Deficit District Report December 2015Detroit Free PressPas encore d'évaluation

- Acific EporterDocument44 pagesAcific EporterScribd Government DocsPas encore d'évaluation

- Sources of School FundingDocument12 pagesSources of School FundingUchenduOkekePas encore d'évaluation

- 6-22-22 Gov McMaster Veto Message R-271 H. 5150 FY 2022-23 Appropriations ActDocument15 pages6-22-22 Gov McMaster Veto Message R-271 H. 5150 FY 2022-23 Appropriations ActLive 5 NewsPas encore d'évaluation

- Shoreline Supp Levy FactsDocument1 pageShoreline Supp Levy FactsRCRockyRamPas encore d'évaluation

- Pennsylvania State Spending: by Nathan Benefield Commonwealth FoundationDocument25 pagesPennsylvania State Spending: by Nathan Benefield Commonwealth FoundationCommonwealth FoundationPas encore d'évaluation

- Fiscal Note & Local Impact Statement: O L S CDocument14 pagesFiscal Note & Local Impact Statement: O L S CKaren KaslerPas encore d'évaluation

- TRC News and Notes 3-15-12Document2 pagesTRC News and Notes 3-15-12James Van BruggenPas encore d'évaluation

- Fiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationDocument39 pagesFiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationParents' Coalition of Montgomery County, MarylandPas encore d'évaluation

- Wrrbfy14 BudgetDocument18 pagesWrrbfy14 BudgetMass LivePas encore d'évaluation

- Asheville City Board of Education ResponseDocument4 pagesAsheville City Board of Education ResponseDaniel WaltonPas encore d'évaluation

- Ohio Education Budget Cuts $2.9 Billion Over Two YearsDocument14 pagesOhio Education Budget Cuts $2.9 Billion Over Two YearsLisa HenlinePas encore d'évaluation

- How School Funding WorksDocument20 pagesHow School Funding WorksCarolyn UptonPas encore d'évaluation

- Testimony Before NYS Legislative Fiscal CommitteeDocument3 pagesTestimony Before NYS Legislative Fiscal CommitteemaryrozakPas encore d'évaluation

- Financing Educational SystemsDocument2 pagesFinancing Educational SystemsRochelle EstebanPas encore d'évaluation

- Reichley Report Summer 2011Document4 pagesReichley Report Summer 2011PAHouseGOPPas encore d'évaluation

- TTR Illinoisfunding SchwartzcordesDocument12 pagesTTR Illinoisfunding SchwartzcordesNational Education Policy CenterPas encore d'évaluation

- OFA OLR Research Report: Education Cost Sharing GrantsDocument18 pagesOFA OLR Research Report: Education Cost Sharing GrantsAlfonso RobinsonPas encore d'évaluation

- SB 12-103: Allocation of At-Risk Funding For Public SchoolsDocument2 pagesSB 12-103: Allocation of At-Risk Funding For Public SchoolsSenator Mike JohnstonPas encore d'évaluation

- CPS Budget (Catalyst 08.09 08.10.11)Document5 pagesCPS Budget (Catalyst 08.09 08.10.11)Valerie F. LeonardPas encore d'évaluation

- FY 2013 Operating Budget - BD of T 12-13-11Document16 pagesFY 2013 Operating Budget - BD of T 12-13-11daggerpressPas encore d'évaluation

- Assessments Standards by Lonnie Tucker, CHE, CSW & Ms. Donna Wells, BS, PCWSDocument38 pagesAssessments Standards by Lonnie Tucker, CHE, CSW & Ms. Donna Wells, BS, PCWSLakotaAdvocatesPas encore d'évaluation

- An Open Letter To Antietam School District ResidentsDocument5 pagesAn Open Letter To Antietam School District ResidentsReading_EaglePas encore d'évaluation

- NYS School District Factbook 2017Document292 pagesNYS School District Factbook 2017Jacqlene100% (2)

- Pennsylvania State Budget: by Nathan Benefield Commonwealth FoundationDocument26 pagesPennsylvania State Budget: by Nathan Benefield Commonwealth FoundationCommonwealth FoundationPas encore d'évaluation

- Position Paper On School Finance Reform in Michigan Revised June 2015Document9 pagesPosition Paper On School Finance Reform in Michigan Revised June 2015api-241862212Pas encore d'évaluation

- BudgetMessage2008 09Document8 pagesBudgetMessage2008 09Thunder PigPas encore d'évaluation

- Costs OkanoganDocument19 pagesCosts Okanoganapi-242006552Pas encore d'évaluation

- ECB Building Aid For Charter Schools 1Document1 pageECB Building Aid For Charter Schools 1Jennifer HarrisPas encore d'évaluation

- Real TalkDocument11 pagesReal TalkEfren RamosPas encore d'évaluation

- December 2005 Bulletin 2Document14 pagesDecember 2005 Bulletin 2Judicial Watch, Inc.Pas encore d'évaluation

- Financing Education in Croatia: Ivana Batarelo, Željka Podrug, and Tome ApostoloskiDocument23 pagesFinancing Education in Croatia: Ivana Batarelo, Željka Podrug, and Tome Apostoloskiivabat17Pas encore d'évaluation

- Resolution On School Funding From WPSBADocument2 pagesResolution On School Funding From WPSBACara MatthewsPas encore d'évaluation

- School Board Approves 2011-12 Budget-FINALDocument2 pagesSchool Board Approves 2011-12 Budget-FINALJawad AhmedPas encore d'évaluation

- Tax Cap Brochure 10-14-11Document6 pagesTax Cap Brochure 10-14-11hhhtaPas encore d'évaluation

- State Investigative Report On UNTDocument5 pagesState Investigative Report On UNTThe Dallas Morning NewsPas encore d'évaluation

- Hoboken Schools 2013-2014 Budget OverviewDocument4 pagesHoboken Schools 2013-2014 Budget OverviewMile Square ViewPas encore d'évaluation

- Willamette Education Service District Needs To Be AccountableDocument28 pagesWillamette Education Service District Needs To Be AccountableStatesman JournalPas encore d'évaluation

- Oregon School District: 123 East Grove Street, Oregon, WI 53575 608-835-4000Document4 pagesOregon School District: 123 East Grove Street, Oregon, WI 53575 608-835-4000Anonymous 9eadjPSJNgPas encore d'évaluation

- Blog Budget PresentationDocument22 pagesBlog Budget Presentationapi-282246902Pas encore d'évaluation

- LAUSD Independent Financial Review Panel - Meeting Materials As of 23 Oct 2015Document260 pagesLAUSD Independent Financial Review Panel - Meeting Materials As of 23 Oct 2015smf 4LAKidsPas encore d'évaluation

- Senate Sub HB59Document110 pagesSenate Sub HB59jointhefuturePas encore d'évaluation

- Audit Report Showed Coatesville School District Mismanaged FundsDocument2 pagesAudit Report Showed Coatesville School District Mismanaged FundsNaomi IsonPas encore d'évaluation

- Young Pa6650 Artifact 1 of 2Document20 pagesYoung Pa6650 Artifact 1 of 2api-671571185Pas encore d'évaluation

- Education Reform SymposiumDocument28 pagesEducation Reform Symposiumapi-651995464Pas encore d'évaluation

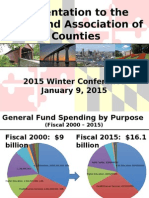

- Presentation To The Maryland Association of CountiesDocument13 pagesPresentation To The Maryland Association of CountiesPublic Information OfficePas encore d'évaluation

- Introduction to School Finance in TexasDocument30 pagesIntroduction to School Finance in TexasaamirPas encore d'évaluation

- Issues and Answers: 2016 Session of The General AssemblyDocument4 pagesIssues and Answers: 2016 Session of The General Assemblyapi-320886833Pas encore d'évaluation

- Forecasting Mainstream School Funding: School Financial Success Guides, #5D'EverandForecasting Mainstream School Funding: School Financial Success Guides, #5Pas encore d'évaluation

- PAY LESS FOR COLLEGE: The Must-Have Guide to Affording Your Degree, 2023 EditionD'EverandPAY LESS FOR COLLEGE: The Must-Have Guide to Affording Your Degree, 2023 EditionPas encore d'évaluation

- Chapter 2 - Taxes, Tax Laws and AdministrationDocument3 pagesChapter 2 - Taxes, Tax Laws and AdministrationAEONGHAE RYPas encore d'évaluation

- BIR Form 1901 Application for RegistrationDocument4 pagesBIR Form 1901 Application for RegistrationMark Domingo MendozaPas encore d'évaluation

- Recomandare CEDocument7 pagesRecomandare CEclaus_44Pas encore d'évaluation

- Hemarus Industries Income Tax Declaration Form SummaryDocument4 pagesHemarus Industries Income Tax Declaration Form SummaryShashi NaganurPas encore d'évaluation

- E-Way Bill SRA 392Document1 pageE-Way Bill SRA 392GANUPas encore d'évaluation

- Income TaxDocument20 pagesIncome Taxjuliaysabellepepitoaguilar100% (1)

- Test Bank For Public Policy Politics Analysis and Alternatives 7th Edition Michael e Kraft Scott R FurlongDocument18 pagesTest Bank For Public Policy Politics Analysis and Alternatives 7th Edition Michael e Kraft Scott R Furlongchristinecruzfbszmkipyd100% (18)

- uFELEKU AYENACHEWDocument50 pagesuFELEKU AYENACHEWamanualPas encore d'évaluation

- ROMarsDocument11 pagesROMarsApply Ako Work EhPas encore d'évaluation

- Employee Declaration Form FY 2020-21Document2 pagesEmployee Declaration Form FY 2020-21Harsha I100% (2)

- Ron Paul "Plan To Restore America": Executive SummaryDocument11 pagesRon Paul "Plan To Restore America": Executive SummaryJoe CookPas encore d'évaluation

- Swedish Match Phil vs. Treasurer of City of Manila.Document2 pagesSwedish Match Phil vs. Treasurer of City of Manila.michelle m. templadoPas encore d'évaluation

- Payslip For The Month of April, 2022: Annual Salary DetailsDocument1 pagePayslip For The Month of April, 2022: Annual Salary DetailsParveen SainiPas encore d'évaluation

- GST LetterDocument1 pageGST LetternrcagroPas encore d'évaluation

- 2019 07 23 09 00 40 881 - 452619484 - PDFDocument6 pages2019 07 23 09 00 40 881 - 452619484 - PDFSadhana TiwariPas encore d'évaluation

- 1 CIR V Hambrecht - QuistDocument2 pages1 CIR V Hambrecht - Quistaspiringlawyer1234Pas encore d'évaluation

- Cost accounting projects breakeven analysis profitDocument3 pagesCost accounting projects breakeven analysis profitbiniamPas encore d'évaluation

- Bitumen Price List HPCL 16-03-2009Document1 pageBitumen Price List HPCL 16-03-2009Vizag Roads100% (1)

- Restaurant Income and Expenses ReportDocument7 pagesRestaurant Income and Expenses ReportSuman Sourav67% (3)

- CTA Ayala Hotels v. CIRDocument17 pagesCTA Ayala Hotels v. CIRnoonalawPas encore d'évaluation

- Income and Expenditure of JakartaDocument10 pagesIncome and Expenditure of JakartaAlfi Nur LailiyahPas encore d'évaluation

- Test Bank Accounting 25th Editon Warren Chapter 11 Current Liabili PDFDocument104 pagesTest Bank Accounting 25th Editon Warren Chapter 11 Current Liabili PDFKristine Lirose Bordeos100% (1)

- Invoice OD117881339439601000Document1 pageInvoice OD117881339439601000bharath.chokkamPas encore d'évaluation

- Sof TAX 1 Case DigestsDocument18 pagesSof TAX 1 Case DigestsJUAN REINO CABITACPas encore d'évaluation

- 2nd Semester Income Taxation Module 2 Taxes, and Tax LawsDocument7 pages2nd Semester Income Taxation Module 2 Taxes, and Tax Lawsnicole tolaybaPas encore d'évaluation

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruMahaPas encore d'évaluation

- Advanced Zimbabwe Tax Module 2011 PDFDocument125 pagesAdvanced Zimbabwe Tax Module 2011 PDFCosmas Takawira88% (24)

- ACCA Result Statistics Jan-Jun 2014Document16 pagesACCA Result Statistics Jan-Jun 2014smedupePas encore d'évaluation

- Goods and Services Tax - GSTR-2B Data Entry InstructionsDocument60 pagesGoods and Services Tax - GSTR-2B Data Entry Instructionsaaruna muruganPas encore d'évaluation

- Compilation of MCQDocument34 pagesCompilation of MCQDaphnie Bolo100% (1)