Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- IB Business and Management Example CommentaryDocument24 pagesIB Business and Management Example CommentaryIB Screwed94% (33)

- The First Basic Plan For Immigration Policy, 2008-2012, Ministry of Justice, Republic of KoreaDocument129 pagesThe First Basic Plan For Immigration Policy, 2008-2012, Ministry of Justice, Republic of KoreakhulawPas encore d'évaluation

- Exemption Certificate PDFDocument33 pagesExemption Certificate PDFChaudhary Hassan ArainPas encore d'évaluation

- BinsDocument1 pageBinsFosterAsantePas encore d'évaluation

- Foreign Direct Investment in Equity Market in IndiaDocument4 pagesForeign Direct Investment in Equity Market in IndiaJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Woodward Life Cycle CostingDocument10 pagesWoodward Life Cycle CostingmelatorPas encore d'évaluation

- China-The Land That Failed To Fail PDFDocument81 pagesChina-The Land That Failed To Fail PDFeric_stPas encore d'évaluation

- India's Wheat Production From 2010 To 2014Document4 pagesIndia's Wheat Production From 2010 To 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Document3 pagesIndia's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India Coir Trade From April To October 2014Document4 pagesIndia Coir Trade From April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Per Capita Food Grain For 2014Document3 pagesIndia's Per Capita Food Grain For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Document4 pagesMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- #IndiaStockExchange #BSE Update On 24th June 2015Document2 pages#IndiaStockExchange #BSE Update On 24th June 2015Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Foreign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Document3 pagesForeign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Diamond Reserves With Diamond Trade Update For 2014Document6 pagesIndia's Diamond Reserves With Diamond Trade Update For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Commercially Operating Nuclear Reactors in The World at The End of 2013Document4 pagesCommercially Operating Nuclear Reactors in The World at The End of 2013Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Rice Trade For 2014Document5 pagesIndia's Rice Trade For 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Coal Production For Last 5 Years Upto October 2014Document2 pagesIndia's Coal Production For Last 5 Years Upto October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

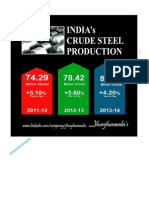

- India Crude Steel Production From 2011-2014Document4 pagesIndia Crude Steel Production From 2011-2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Coal Reserves To Last 100 YearsDocument3 pagesIndia's Coal Reserves To Last 100 YearsJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Import and Export Update For September and December 2014Document16 pagesIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Methane Hydrates Reserves 25th November 2014Document3 pagesIndia's Methane Hydrates Reserves 25th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

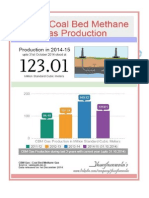

- India's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Document3 pagesIndia's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Kharif and Rabi Crops Area Coverage For October and January 2014Document10 pagesIndia's Kharif and Rabi Crops Area Coverage For October and January 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Fuel Price Change For Petrol, Diesel, and JetFuel in IndiaDocument11 pagesFuel Price Change For Petrol, Diesel, and JetFuel in IndiaJhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Crude Steel Production Estimate For 2014 To 2017Document3 pagesIndia's Crude Steel Production Estimate For 2014 To 2017Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Foreign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Document27 pagesForeign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Global Central Banks Highlights For Monetary Policy Rates For October 2014Document31 pagesGlobal Central Banks Highlights For Monetary Policy Rates For October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Mineral Production in Month of August 2014Document3 pagesIndia's Mineral Production in Month of August 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Indians Railways Revenue Earnings With Freight Traffic During April To October 2014Document18 pagesIndians Railways Revenue Earnings With Freight Traffic During April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India Tax Collection From April To November 2014Document11 pagesIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India 'S Total Kharif Crop Sowing Area As On July and August 2014Document6 pagesIndia 'S Total Kharif Crop Sowing Area As On July and August 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Tourism Sector Performance For January and October 2014Document15 pagesIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- India's Index of Eight Core Industries From June To November 2014Document57 pagesIndia's Index of Eight Core Industries From June To November 2014Jhunjhunwalas Digital Finance & Business Info Library100% (1)

- Global Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Document11 pagesGlobal Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Document5 pagesIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryPas encore d'évaluation

- Time Wise ItineraryDocument3 pagesTime Wise ItineraryKeshav BahetiPas encore d'évaluation

- RSAW Review of The Year 2021Document14 pagesRSAW Review of The Year 2021Prasamsa PPas encore d'évaluation

- Factors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Document53 pagesFactors Responsible For The Location of Primary, Secondary, and Tertiary Sector Industries in Various Parts of The World (Including India)Aditya KumarPas encore d'évaluation

- AIRTITEDocument2 pagesAIRTITEMuhammad AtifPas encore d'évaluation

- Leizel C. AmidoDocument2 pagesLeizel C. AmidoAmido Capagngan LeizelPas encore d'évaluation

- 15 Engineering Economy SolutionsDocument4 pages15 Engineering Economy SolutionsKristian Erick Ofiana Rimas0% (1)

- Seminar Topic: Fill All ContentDocument7 pagesSeminar Topic: Fill All ContentRanjith GowdaPas encore d'évaluation

- 184 History of AgricultureDocument25 pages184 History of AgricultureBhupendra PunvarPas encore d'évaluation

- 10 TPH Cil Equipment-20171022Document10 pages10 TPH Cil Equipment-20171022KareemAmen100% (1)

- Midc MumbaiDocument26 pagesMidc MumbaiparagPas encore d'évaluation

- Grammar Vocabulary 1star Unit7 PDFDocument1 pageGrammar Vocabulary 1star Unit7 PDFLorenaAbreuPas encore d'évaluation

- Project Reference List - ReferenceDocument7 pagesProject Reference List - ReferenceGohdsPas encore d'évaluation

- Red Sun Travels in Naxalite Country by Sudeep Chakravarti PDFDocument218 pagesRed Sun Travels in Naxalite Country by Sudeep Chakravarti PDFBasu VPas encore d'évaluation

- Borjas 2013 Power Point Chapter 8Document36 pagesBorjas 2013 Power Point Chapter 8Shahirah Hafit0% (1)

- CBR ProcterGamble 06Document2 pagesCBR ProcterGamble 06Kuljeet Kaur ThethiPas encore d'évaluation

- 25-JUNE-2021: The Hindu News Analysis - 25 June 2021 - Shankar IAS AcademyDocument22 pages25-JUNE-2021: The Hindu News Analysis - 25 June 2021 - Shankar IAS AcademyHema and syedPas encore d'évaluation

- Galvor CaseDocument10 pagesGalvor CaseLawi AnupamPas encore d'évaluation

- Value ChainDocument31 pagesValue ChainNodiey YanaPas encore d'évaluation

- Import - Export Tariff of Local Charges at HCM For FCL & LCL & Air (Free-Hand) - FinalDocument2 pagesImport - Export Tariff of Local Charges at HCM For FCL & LCL & Air (Free-Hand) - FinalNguyễn Thanh LongPas encore d'évaluation

- Seedling Trays Developed by Kal-KarDocument2 pagesSeedling Trays Developed by Kal-KarIsrael ExporterPas encore d'évaluation

- Contemporary Issues of GlobalizationDocument22 pagesContemporary Issues of GlobalizationAyman MotenPas encore d'évaluation

- Coas b1 AcksDocument1 pageCoas b1 AcksSanah KhanPas encore d'évaluation

- Complete History of The Soviet Union, Arranged To The Melody of TetrisDocument2 pagesComplete History of The Soviet Union, Arranged To The Melody of TetrisMikael HolmströmPas encore d'évaluation

- Unit 1 Econ VocabDocument5 pagesUnit 1 Econ VocabNatalia HowardPas encore d'évaluation