Vous aimerez peut-être aussi

- Human Resource Management Practices in A Local Organization of BangladeshDocument12 pagesHuman Resource Management Practices in A Local Organization of BangladeshisanPas encore d'évaluation

- Mod Te Ha Ge Liaison Office of BDDocument37 pagesMod Te Ha Ge Liaison Office of BDFakir TajulPas encore d'évaluation

- Liquidity StatementDocument10 pagesLiquidity StatementFakir TajulPas encore d'évaluation

- Profitability An v1 Sent 2Document9 pagesProfitability An v1 Sent 2Fakir TajulPas encore d'évaluation

- Service Quality Bank v1 Sent 2Document12 pagesService Quality Bank v1 Sent 2Fakir TajulPas encore d'évaluation

- Assignment FormatDocument7 pagesAssignment FormatFakir TajulPas encore d'évaluation

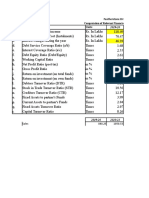

- Fund Management Practices of Nationalized Bangladeshi BanksDocument13 pagesFund Management Practices of Nationalized Bangladeshi BanksFakir TajulPas encore d'évaluation

- Differences RAM ROM GivenDocument6 pagesDifferences RAM ROM GivenFakir TajulPas encore d'évaluation

- What Is CRR & SLR Position and What Are The Components of CRR & SLR?Document8 pagesWhat Is CRR & SLR Position and What Are The Components of CRR & SLR?Fakir TajulPas encore d'évaluation

- Just For UploadDocument1 pageJust For UploadFakir TajulPas encore d'évaluation

- Classification of Computers GivenDocument5 pagesClassification of Computers GivenFakir TajulPas encore d'évaluation

- Carers in Partnership Mental Health CommissioningDocument6 pagesCarers in Partnership Mental Health CommissioningFakir TajulPas encore d'évaluation

- Uu Co MacroeconomicsDocument3 pagesUu Co MacroeconomicsFakir TajulPas encore d'évaluation

- Differences RAM ROM GivenDocument6 pagesDifferences RAM ROM GivenFakir TajulPas encore d'évaluation

- Chronic Condition Self-Management Approaches Research and EvaluationDocument50 pagesChronic Condition Self-Management Approaches Research and EvaluationFakir TajulPas encore d'évaluation

- Rex - Research Proposal SentDocument15 pagesRex - Research Proposal SentFakir TajulPas encore d'évaluation

- 5 BP White Paper Engagement 2Document10 pages5 BP White Paper Engagement 2Fakir TajulPas encore d'évaluation

- Irr SolveDocument1 pageIrr SolveFakir TajulPas encore d'évaluation

- Unit 8Document1 pageUnit 8Fakir TajulPas encore d'évaluation

- Jahid e Business Jan5 SentDocument6 pagesJahid e Business Jan5 SentFakir TajulPas encore d'évaluation

- Rumki - Vision and Strategic Direction 3500 - April 13 - Sent Black Plaz SolvedDocument16 pagesRumki - Vision and Strategic Direction 3500 - April 13 - Sent Black Plaz SolvedFakir Tajul100% (1)

- Management skills and organizational behaviorDocument1 pageManagement skills and organizational behaviorFakir TajulPas encore d'évaluation

- MTB Millionaire PlanDocument5 pagesMTB Millionaire PlanFakir TajulPas encore d'évaluation

- Rex Research ProposalDocument20 pagesRex Research ProposalFakir TajulPas encore d'évaluation

- MTB Millionaire PlanDocument5 pagesMTB Millionaire PlanFakir TajulPas encore d'évaluation

- GK - Headquaters of OrganizationsDocument1 pageGK - Headquaters of OrganizationsFakir TajulPas encore d'évaluation

- Subject CoverageDocument1 pageSubject CoverageFakir TajulPas encore d'évaluation

- UnusedDocument2 pagesUnusedFakir TajulPas encore d'évaluation

- CFA Exam Calendar and FeesDocument12 pagesCFA Exam Calendar and FeesFakir TajulPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Knowledge for eAudIT: Processes, WCGWs and Controls in Oil and GasDocument10 pagesKnowledge for eAudIT: Processes, WCGWs and Controls in Oil and Gasabdullahsaleem91100% (1)

- CIR v. Gotamco & SonsDocument3 pagesCIR v. Gotamco & Sonsjmf123Pas encore d'évaluation

- Morgan Stanley Funds (UK) : Semi-Annual Report (Unaudited)Document45 pagesMorgan Stanley Funds (UK) : Semi-Annual Report (Unaudited)J. BangjakPas encore d'évaluation

- Lehman BrothersDocument38 pagesLehman Brothersapi-370084550% (6)

- 330 S12 IndSty MT AMongelluzzoDocument8 pages330 S12 IndSty MT AMongelluzzomongo9279Pas encore d'évaluation

- Retail Maths FormulasDocument6 pagesRetail Maths Formulasankursharma29100% (1)

- Total Computation QB by CA Pranav ChandakDocument37 pagesTotal Computation QB by CA Pranav ChandakSurajPas encore d'évaluation

- Sargodha Spices Accounts DetailDocument3 pagesSargodha Spices Accounts Detailwasim khanPas encore d'évaluation

- Audited Financial StatementDocument17 pagesAudited Financial StatementVictor BiacoloPas encore d'évaluation

- PAFCO 2015 Annual Report SummaryDocument43 pagesPAFCO 2015 Annual Report Summarycris gerard trinidadPas encore d'évaluation

- Basic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)Document17 pagesBasic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)LiaPas encore d'évaluation

- Ratio Analysis Notes (Theory)Document3 pagesRatio Analysis Notes (Theory)Karishma KatiyarPas encore d'évaluation

- Chapter 3 ExercisesDocument11 pagesChapter 3 ExercisesNguyen VyPas encore d'évaluation

- Answers - Chapter 4 Vol 2 RvsedDocument15 pagesAnswers - Chapter 4 Vol 2 Rvsedjamflox50% (2)

- PVH Financial Analysis - Q1Document7 pagesPVH Financial Analysis - Q1Dulakshi RanadeeraPas encore d'évaluation

- Chapter 6 - Accounting For SalesDocument4 pagesChapter 6 - Accounting For SalesArmanPas encore d'évaluation

- GHCLLimitedDocument40 pagesGHCLLimitedhamsPas encore d'évaluation

- The Colorado Cannabis Industry: A Tale of Ten CitiesDocument12 pagesThe Colorado Cannabis Industry: A Tale of Ten CitiesJames CampbellPas encore d'évaluation

- Accounting Principles 12th Edition Weygandt Solutions Manual Full Chapter PDFDocument37 pagesAccounting Principles 12th Edition Weygandt Solutions Manual Full Chapter PDFEdwardBishopacsy100% (11)

- Balance Sheet: Glaxosmithkline Pakistan LimitedDocument15 pagesBalance Sheet: Glaxosmithkline Pakistan LimitedMuhammad SamiPas encore d'évaluation

- Checklist of Key Figures: Kieso Intermediate Accounting, Twelfth EditionDocument4 pagesChecklist of Key Figures: Kieso Intermediate Accounting, Twelfth EditionEdi F SyahadatPas encore d'évaluation

- ADBM – Full Time Financial Accounting Multiple Choice QuestionsDocument8 pagesADBM – Full Time Financial Accounting Multiple Choice QuestionsAshika JayaweeraPas encore d'évaluation

- 2015 IKEA Annual Report Shows 18.75% Revenue GrowthDocument1 page2015 IKEA Annual Report Shows 18.75% Revenue GrowthGilang RamadhanPas encore d'évaluation

- Featherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53Document39 pagesFeatherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53saubhik goswamiPas encore d'évaluation

- Islam MLM by mufti-MASUM-billahDocument61 pagesIslam MLM by mufti-MASUM-billahkazi yakub aliPas encore d'évaluation

- Financial Reporting 3rd Edition Janice Loftus Ken Leo Sorin Daniliuc Noel Boys Belinda Luke Hong Nee Ang Karyn ByrnesDocument35 pagesFinancial Reporting 3rd Edition Janice Loftus Ken Leo Sorin Daniliuc Noel Boys Belinda Luke Hong Nee Ang Karyn ByrnesLinda MitchellPas encore d'évaluation

- Establishment of Jackfruit Meat Gourmet Manufactoring Business in Siniloan LagunaDocument14 pagesEstablishment of Jackfruit Meat Gourmet Manufactoring Business in Siniloan LagunaAPJAET JournalPas encore d'évaluation

- Accounting GlossaryDocument2 pagesAccounting GlossaryPisokely Nana JrPas encore d'évaluation

- Dynamic ModelDocument48 pagesDynamic ModelJohnny BravoPas encore d'évaluation

- Ican Nov 2014 Skills PathfinderDocument172 pagesIcan Nov 2014 Skills PathfinderEmezi Francis Obisike100% (3)