Vous aimerez peut-être aussi

- Winterization Checklist & Documentation: Safeguard PropertiesDocument1 pageWinterization Checklist & Documentation: Safeguard PropertiesWb Warnabrother HatchetPas encore d'évaluation

- Fred Killah DevonanDocument1 pageFred Killah DevonanWb Warnabrother HatchetPas encore d'évaluation

- How Music Royalties Work-Types of Rights and RoyaltiesDocument11 pagesHow Music Royalties Work-Types of Rights and RoyaltiesWb Warnabrother HatchetPas encore d'évaluation

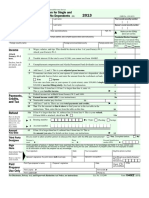

- F1040ez PDFDocument2 pagesF1040ez PDFjc75aPas encore d'évaluation

- Proof of Service MethodsDocument2 pagesProof of Service MethodsWb Warnabrother HatchetPas encore d'évaluation

- 55 Ideas Start Biz For Uner 50000Document11 pages55 Ideas Start Biz For Uner 50000Wb Warnabrother HatchetPas encore d'évaluation

- Resume 1Document4 pagesResume 1Wb Warnabrother HatchetPas encore d'évaluation

- Look Into The Mind of A Madman Ft. Excalibur Blame It On The White Guy FT - Ramz Minolo, Saint Siren & Gstats OCB-Prod - Track ProsDocument2 pagesLook Into The Mind of A Madman Ft. Excalibur Blame It On The White Guy FT - Ramz Minolo, Saint Siren & Gstats OCB-Prod - Track ProsWb Warnabrother HatchetPas encore d'évaluation

- 106Document4 pages106Wb Warnabrother HatchetPas encore d'évaluation

- F1040ez PDFDocument2 pagesF1040ez PDFjc75aPas encore d'évaluation

- FirstNoticeforDiscovery PDFDocument7 pagesFirstNoticeforDiscovery PDFWb Warnabrother HatchetPas encore d'évaluation

- ParalegalDocument1 pageParalegalWb Warnabrother HatchetPas encore d'évaluation

- Certificate of Publication OFDocument2 pagesCertificate of Publication OFWb Warnabrother HatchetPas encore d'évaluation

- Lovewe Incense and Khumsi ContactDocument1 pageLovewe Incense and Khumsi ContactWb Warnabrother HatchetPas encore d'évaluation

- Zulu 40THDocument1 pageZulu 40THWb Warnabrother HatchetPas encore d'évaluation

- The 3 Most Profitable DIY Revenue Streams, and Why Many Artists Succeed at Only One of ThemDocument2 pagesThe 3 Most Profitable DIY Revenue Streams, and Why Many Artists Succeed at Only One of ThemWb Warnabrother HatchetPas encore d'évaluation

- StampDocument1 pageStampWb Warnabrother HatchetPas encore d'évaluation

- Guide To Mixing v1.0: Nick Thomas February 8, 2009Document56 pagesGuide To Mixing v1.0: Nick Thomas February 8, 2009nhomas94% (16)

- Independent Paralegals HandbookDocument401 pagesIndependent Paralegals HandbookWb Warnabrother Hatchet100% (13)

- NotesDocument1 pageNotesjmj9Pas encore d'évaluation

- NotesDocument1 pageNotesjmj9Pas encore d'évaluation

- Create Bigger Sounds Using Layering PDFDocument7 pagesCreate Bigger Sounds Using Layering PDFWb Warnabrother HatchetPas encore d'évaluation

- Create Bigger Sounds Using Layering PDFDocument7 pagesCreate Bigger Sounds Using Layering PDFWb Warnabrother HatchetPas encore d'évaluation

- Independent Paralegals HandbookDocument401 pagesIndependent Paralegals HandbookWb Warnabrother Hatchet100% (13)

- F 1099 ADocument6 pagesF 1099 AWb Warnabrother Hatchet50% (2)

- Examinee Information ClaDocument38 pagesExaminee Information ClaWb Warnabrother HatchetPas encore d'évaluation

- The RainDocument6 pagesThe RainWeeChuanChinPas encore d'évaluation

- How To Make Usb KeyDocument1 pageHow To Make Usb KeyWb Warnabrother HatchetPas encore d'évaluation

- Project Completion Certificate FiligreeDocument1 pageProject Completion Certificate FiligreeWb Warnabrother HatchetPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Effective Instruction OverviewDocument5 pagesEffective Instruction Overviewgene mapaPas encore d'évaluation

- 9 Specific Relief Act, 1877Document20 pages9 Specific Relief Act, 1877mostafa faisalPas encore d'évaluation

- Week 5 WHLP Nov. 2 6 2020 DISSDocument5 pagesWeek 5 WHLP Nov. 2 6 2020 DISSDaniel BandibasPas encore d'évaluation

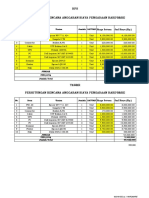

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDocument2 pagesHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriPas encore d'évaluation

- CVA: Health Education PlanDocument4 pagesCVA: Health Education Plandanluki100% (3)

- Political Science Assignment PDFDocument6 pagesPolitical Science Assignment PDFkalari chandanaPas encore d'évaluation

- Scantype NNPC AdvertDocument3 pagesScantype NNPC AdvertAdeshola FunmilayoPas encore d'évaluation

- Geraads 2016 Pleistocene Carnivora (Mammalia) From Tighennif (Ternifine), AlgeriaDocument45 pagesGeraads 2016 Pleistocene Carnivora (Mammalia) From Tighennif (Ternifine), AlgeriaGhaier KazmiPas encore d'évaluation

- FI - Primeiro Kfir 1975 - 1254 PDFDocument1 pageFI - Primeiro Kfir 1975 - 1254 PDFguilhermePas encore d'évaluation

- Schematic Electric System Cat D8T Vol1Document33 pagesSchematic Electric System Cat D8T Vol1Andaru Gunawan100% (1)

- 14 Worst Breakfast FoodsDocument31 pages14 Worst Breakfast Foodscora4eva5699100% (1)

- dlp4 Math7q3Document3 pagesdlp4 Math7q3Therence UbasPas encore d'évaluation

- Presentations - Benefits of WalkingDocument1 pagePresentations - Benefits of WalkingEde Mehta WardhanaPas encore d'évaluation

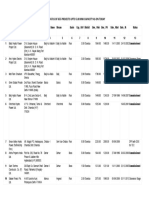

- List/Status of 655 Projects Upto 5.00 MW Capacity As On TodayDocument45 pagesList/Status of 655 Projects Upto 5.00 MW Capacity As On Todayganvaqqqzz21Pas encore d'évaluation

- How To Make Wall Moulding Design For Rooms Accent Wall Video TutorialsDocument15 pagesHow To Make Wall Moulding Design For Rooms Accent Wall Video Tutorialsdonaldwhale1151Pas encore d'évaluation

- DPS Chief Michael Magliano DIRECTIVE. Arrests Inside NYS Courthouses April 17, 2019 .Document1 pageDPS Chief Michael Magliano DIRECTIVE. Arrests Inside NYS Courthouses April 17, 2019 .Desiree YaganPas encore d'évaluation

- Week 1 ITM 410Document76 pagesWeek 1 ITM 410Awesom QuenzPas encore d'évaluation

- Ck-Nac FsDocument2 pagesCk-Nac Fsadamalay wardiwiraPas encore d'évaluation

- 10 1108 - Apjie 02 2023 0027Document17 pages10 1108 - Apjie 02 2023 0027Aubin DiffoPas encore d'évaluation

- El Rol Del Fonoaudiólogo Como Agente de Cambio Social (Segundo Borrador)Document11 pagesEl Rol Del Fonoaudiólogo Como Agente de Cambio Social (Segundo Borrador)Jorge Nicolás Silva Flores100% (1)

- Diagnosis of Dieback Disease of The Nutmeg Tree in Aceh Selatan, IndonesiaDocument10 pagesDiagnosis of Dieback Disease of The Nutmeg Tree in Aceh Selatan, IndonesiaciptaPas encore d'évaluation

- Investigation of Cyber CrimesDocument9 pagesInvestigation of Cyber CrimesHitesh BansalPas encore d'évaluation

- The Use of Humor in The Classroom - Exploring Effects On Teacher-SDocument84 pagesThe Use of Humor in The Classroom - Exploring Effects On Teacher-Sanir.elhou.bouifriPas encore d'évaluation

- General Ethics: The Importance of EthicsDocument2 pagesGeneral Ethics: The Importance of EthicsLegendXPas encore d'évaluation

- Mental Health Admission & Discharge Dip NursingDocument7 pagesMental Health Admission & Discharge Dip NursingMuranatu CynthiaPas encore d'évaluation

- Ruby Tuesday LawsuitDocument17 pagesRuby Tuesday LawsuitChloé MorrisonPas encore d'évaluation

- Compassion and AppearancesDocument9 pagesCompassion and AppearancesriddhiPas encore d'évaluation

- Case Study - Succession LawDocument2 pagesCase Study - Succession LawpablopoparamartinPas encore d'évaluation

- Once in his Orient: Le Corbusier and the intoxication of colourDocument4 pagesOnce in his Orient: Le Corbusier and the intoxication of coloursurajPas encore d'évaluation

- Lab Report FormatDocument2 pagesLab Report Formatapi-276658659Pas encore d'évaluation