Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- How Education Can Prevent ViolenceDocument4 pagesHow Education Can Prevent ViolenceAmit ManwaniPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Print N Colur in Sticker PaperDocument3 pagesPrint N Colur in Sticker PaperAmit ManwaniPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Agreement For SsDocument5 pagesAgreement For SsAmit ManwaniPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- CV - Anil RangwaniDocument3 pagesCV - Anil RangwaniAmit ManwaniPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Process:: PromotionDocument1 pageProcess:: PromotionAmit ManwaniPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Employment ContractDocument3 pagesEmployment ContractMukesh ManwaniPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- InsuranceDocument10 pagesInsuranceAmit ManwaniPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Property Irregularity ReportDocument1 pageProperty Irregularity ReportAmit ManwaniPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Ratio Analysis Project ReportDocument70 pagesRatio Analysis Project ReportAmit ManwaniPas encore d'évaluation

- Contrast Ladies & Gents: Face CleanupDocument3 pagesContrast Ladies & Gents: Face CleanupAmit ManwaniPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Urriculum: Girish Kanjan VashdevDocument3 pagesUrriculum: Girish Kanjan VashdevAmit ManwaniPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Audit Evidence A) IntroductionDocument5 pagesAudit Evidence A) IntroductionAmit ManwaniPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Resume 123Document2 pagesResume 123Amit ManwaniPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- New Microsoft Office Word DocumentDocument3 pagesNew Microsoft Office Word DocumentAmit ManwaniPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Personal Budget Project PowerpointDocument12 pagesPersonal Budget Project Powerpointapi-5604508810% (1)

- Combine PDFDocument3 pagesCombine PDFKaye ApostolPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- UP Bar Reviewer 2013 - TaxationDocument210 pagesUP Bar Reviewer 2013 - TaxationPJGalera89% (28)

- GST Entries For Every Month SalesDocument3 pagesGST Entries For Every Month SalesGiri Sukumar100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Assignment 1 For MBA 2020Document10 pagesAssignment 1 For MBA 2020Sichen UpretyPas encore d'évaluation

- Budget Proposal For Graduation and Completion RitesDocument4 pagesBudget Proposal For Graduation and Completion Ritesloreta50% (6)

- Trish Joy Foundation 990: 2016Document22 pagesTrish Joy Foundation 990: 2016Tony OrtegaPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- ApplicationForm 656724Document1 pageApplicationForm 656724shahid ashrafPas encore d'évaluation

- Manasa Resume - 1Document3 pagesManasa Resume - 1ManasaPas encore d'évaluation

- Statement of Management'S Responsibility For Annual Income Tax ReturnDocument2 pagesStatement of Management'S Responsibility For Annual Income Tax ReturnRyan PazonPas encore d'évaluation

- Ward 9 - Kulo Shreenagar PurvaDocument5 pagesWard 9 - Kulo Shreenagar PurvaPMEP Kapilvastu MunicipalityPas encore d'évaluation

- Remittance VoucherDocument2 pagesRemittance VoucherЕвгений БулгаковPas encore d'évaluation

- Interim Financial ReportingDocument3 pagesInterim Financial ReportingBernie Mojico CaronanPas encore d'évaluation

- Tax 1 - IndividualsDocument15 pagesTax 1 - IndividualsDianne MadridPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- 16 Roxas V CTA 23 SCRA 276 1968 Digest 1Document3 pages16 Roxas V CTA 23 SCRA 276 1968 Digest 1Graziella AndayaPas encore d'évaluation

- List of Bir Forms: Form No. Form TitleDocument2 pagesList of Bir Forms: Form No. Form Titleabc360shellePas encore d'évaluation

- Toa03 05 SBC BC GG Dividends Beps and DepsDocument2 pagesToa03 05 SBC BC GG Dividends Beps and DepsMerliza JusayanPas encore d'évaluation

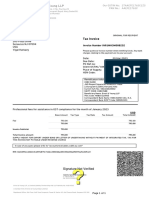

- Tax Invoice For LT Current Consumption Charges For The Month of January 2024Document1 pageTax Invoice For LT Current Consumption Charges For The Month of January 2024goldentraders2574Pas encore d'évaluation

- Taxation I and II Syllabus - Chapters 1 To 28Document61 pagesTaxation I and II Syllabus - Chapters 1 To 28Czar Ian AgbayaniPas encore d'évaluation

- EY Invoice - ORG - IN91MH3M008232Document1 pageEY Invoice - ORG - IN91MH3M008232AltafPas encore d'évaluation

- AuwmDocument1 pageAuwmNishanthPas encore d'évaluation

- Merchant Declaration FormDocument2 pagesMerchant Declaration Formleotrainings5Pas encore d'évaluation

- Individual Tax Payer - Part 2Document18 pagesIndividual Tax Payer - Part 2Ems TeopePas encore d'évaluation

- Stamp Duty For Partnership DeedDocument2 pagesStamp Duty For Partnership DeedragyaPas encore d'évaluation

- Division of Calamba City CADocument6 pagesDivision of Calamba City CAJeremiah TrinidadPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 2010-11 PAYG - FN Tax TablesDocument12 pages2010-11 PAYG - FN Tax Tablescyclops4569Pas encore d'évaluation

- Taxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTDocument5 pagesTaxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTTheEnigmatic AccountantPas encore d'évaluation

- Deceased Depositor Information: Traditional/Roth IRA Plan Beneficiary Distribution Election FormDocument2 pagesDeceased Depositor Information: Traditional/Roth IRA Plan Beneficiary Distribution Election FormJohn Christian ReyesPas encore d'évaluation

- MCM Form ADocument2 pagesMCM Form AAnonymous SCYk5IUPas encore d'évaluation

- Basilan Estates Vs CIR Tax Round4Document2 pagesBasilan Estates Vs CIR Tax Round4Angeleeca Sernande CalpitoPas encore d'évaluation