Vous aimerez peut-être aussi

- Operating ExposureDocument31 pagesOperating ExposureMai LiênPas encore d'évaluation

- Chapter 23 Sojan & SreehariDocument19 pagesChapter 23 Sojan & SreehariSojanuPas encore d'évaluation

- Variable Interest 2013Document246 pagesVariable Interest 2013gligorjan100% (1)

- Losses Vis-A-Vis Transfer PricingDocument10 pagesLosses Vis-A-Vis Transfer PricingChirag ShahPas encore d'évaluation

- Captive Shared Service Centers For S&L Industry PDFDocument8 pagesCaptive Shared Service Centers For S&L Industry PDFsongaonkarsPas encore d'évaluation

- Are You Identifying and Managing The Key Tax Risks in TMT M&A?Document1 pageAre You Identifying and Managing The Key Tax Risks in TMT M&A?CcapealPas encore d'évaluation

- Transfer Pricing PPT 190714 FinalDocument268 pagesTransfer Pricing PPT 190714 Finalvijaywin6299Pas encore d'évaluation

- Guide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesD'EverandGuide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesPas encore d'évaluation

- Transaction ExposureDocument28 pagesTransaction ExposureMai LiênPas encore d'évaluation

- PAINEL 1 - Transfer Pricing & IntangiblesDocument20 pagesPAINEL 1 - Transfer Pricing & Intangiblesedson souzaPas encore d'évaluation

- FX Risk Management Transaction Exposure: Slide 1Document55 pagesFX Risk Management Transaction Exposure: Slide 1prakashputtuPas encore d'évaluation

- Plesnerrossing2017 PDFDocument13 pagesPlesnerrossing2017 PDFM Iqbal RamadhanPas encore d'évaluation

- Workshop On Transfer Pricing 7 8aug09Document107 pagesWorkshop On Transfer Pricing 7 8aug09PRAMODH VMNPas encore d'évaluation

- Bae 4382 WP Cloud MigrationDocument12 pagesBae 4382 WP Cloud MigrationMauricio CastroPas encore d'évaluation

- International TP Handbook 2011Document0 pageInternational TP Handbook 2011Kolawole AkinmojiPas encore d'évaluation

- Itp 2015 2016 Final PDFDocument1 162 pagesItp 2015 2016 Final PDFht1234222Pas encore d'évaluation

- Slides International Taxation 2Document17 pagesSlides International Taxation 2yebegashetPas encore d'évaluation

- Coordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsDocument18 pagesCoordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsSgt2Pas encore d'évaluation

- Bav Unit 4th DCFDocument57 pagesBav Unit 4th DCFRahul GuptaPas encore d'évaluation

- PWC Managed Services Whitepaper Covid 19Document14 pagesPWC Managed Services Whitepaper Covid 19Gert KoekemoerPas encore d'évaluation

- Performance Contracting in KenyaDocument10 pagesPerformance Contracting in Kenyawangaoe100% (9)

- Lecture 23 - 45 CombinedDocument271 pagesLecture 23 - 45 CombinedMuhammad Kamran KhanPas encore d'évaluation

- IFM 08 Transfer PriceDocument27 pagesIFM 08 Transfer PriceTanu GuptaPas encore d'évaluation

- Income Tax Provision ChecklistDocument20 pagesIncome Tax Provision Checklistakschess pPas encore d'évaluation

- Cost of Capital of UK CompaniesDocument8 pagesCost of Capital of UK CompaniesSonia AgarwalPas encore d'évaluation

- Operational Readiness Review A Complete Guide - 2020 EditionD'EverandOperational Readiness Review A Complete Guide - 2020 EditionPas encore d'évaluation

- Financial Statement Analysis (Fsa)Document32 pagesFinancial Statement Analysis (Fsa)Shashank100% (1)

- Libor Euribor Prime RatesDocument16 pagesLibor Euribor Prime RatessabbathmailerPas encore d'évaluation

- How to Start a Valet Service Business: Step by Step Business PlanD'EverandHow to Start a Valet Service Business: Step by Step Business PlanPas encore d'évaluation

- Various Forces of Change in Business EnviromentDocument5 pagesVarious Forces of Change in Business Enviromentabhijitbiswas25Pas encore d'évaluation

- Operating LeverageDocument2 pagesOperating LeveragePankaj2cPas encore d'évaluation

- AssignmetDocument4 pagesAssignmetHumza SarwarPas encore d'évaluation

- ADIT Exam Paper - June 2019 (Question Paper)Document8 pagesADIT Exam Paper - June 2019 (Question Paper)Yayang Pratama PutraPas encore d'évaluation

- BX2011 Topic01 Tutorial Solutions 2020Document15 pagesBX2011 Topic01 Tutorial Solutions 2020Shi Pyeit Sone Kyaw0% (1)

- Property and EquipmentDocument101 pagesProperty and EquipmentJulianna TonogbanuaPas encore d'évaluation

- Complex Decisions in Capital BudgetingDocument4 pagesComplex Decisions in Capital BudgetingDeven RathodPas encore d'évaluation

- Dividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Document9 pagesDividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Anonymous H2L7lwBs3Pas encore d'évaluation

- Corporate Financial Analysis with Microsoft ExcelD'EverandCorporate Financial Analysis with Microsoft ExcelÉvaluation : 5 sur 5 étoiles5/5 (1)

- June 2017 Paper 3.03 (Question Paper)Document7 pagesJune 2017 Paper 3.03 (Question Paper)Timore FrancisPas encore d'évaluation

- Unit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomDocument68 pagesUnit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomMotiram paudelPas encore d'évaluation

- Mid MonthDocument4 pagesMid Monthcipollini50% (2)

- Discounted Cash Flow (DCF) Definition - InvestopediaDocument2 pagesDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532Pas encore d'évaluation

- REAL 209 Midterm II Study GuideDocument4 pagesREAL 209 Midterm II Study GuidejuanPas encore d'évaluation

- Apv PDFDocument10 pagesApv PDFSam Sep A SixtyonePas encore d'évaluation

- Credit Risk ManagementDocument4 pagesCredit Risk ManagementlintoPas encore d'évaluation

- EBK TMS Toolkit TMS Selection GTreasuryDocument25 pagesEBK TMS Toolkit TMS Selection GTreasurymashael abanmiPas encore d'évaluation

- 9.1 Operating ExposureDocument28 pages9.1 Operating ExposureSanaFatimaPas encore d'évaluation

- Week 2 Managerial FinanceDocument64 pagesWeek 2 Managerial FinanceCalista Elvina JesslynPas encore d'évaluation

- Asset Backed SecuritiesDocument179 pagesAsset Backed SecuritiesShivani NidhiPas encore d'évaluation

- Data Mining and Knowledge ManagementDocument9 pagesData Mining and Knowledge ManagementSyed Arfat AliPas encore d'évaluation

- Debt (Or Leverage) Management RatiosDocument4 pagesDebt (Or Leverage) Management RatiosJohn MuemaPas encore d'évaluation

- Venkys Financial Results 31.03.17Document7 pagesVenkys Financial Results 31.03.17sriramrangaPas encore d'évaluation

- Rural Electrification Corp. Ltd. Initiating CoverargeDocument5 pagesRural Electrification Corp. Ltd. Initiating CoverargesriramrangaPas encore d'évaluation

- Navkar Corporation - SPA ResearchDocument4 pagesNavkar Corporation - SPA ResearchanjugaduPas encore d'évaluation

- Annual Report CimmcoDocument57 pagesAnnual Report CimmcosriramrangaPas encore d'évaluation

- Voltamp Annual Report F.Y - 2015-16Document67 pagesVoltamp Annual Report F.Y - 2015-16sriramrangaPas encore d'évaluation

- Pennar Industries Q4fy17 Investor Presentation FinalDocument29 pagesPennar Industries Q4fy17 Investor Presentation FinalsriramrangaPas encore d'évaluation

- NDR Presentation (Company Update)Document28 pagesNDR Presentation (Company Update)Shyam SunderPas encore d'évaluation

- Eimco Elecon Equity Research Report July 2016Document19 pagesEimco Elecon Equity Research Report July 2016sriramrangaPas encore d'évaluation

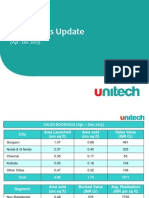

- Unitech Limited Annual Report 2014 15Document192 pagesUnitech Limited Annual Report 2014 15sriramrangaPas encore d'évaluation

- 53rd Annual Report 2013-2014Document127 pages53rd Annual Report 2013-2014sriramrangaPas encore d'évaluation

- SC Arunchal - JudgmentDocument331 pagesSC Arunchal - JudgmentFirstpostPas encore d'évaluation

- The Murder of The MahatmaDocument65 pagesThe Murder of The MahatmaKonkman0% (1)

- JpassociatAnnual Report For The Year 2014-15Document212 pagesJpassociatAnnual Report For The Year 2014-15Gagan SinghPas encore d'évaluation

- 55th Annual Report 2013-14Document78 pages55th Annual Report 2013-14sriramrangaPas encore d'évaluation

- Operational Update 31dec 2013Document64 pagesOperational Update 31dec 2013sriramrangaPas encore d'évaluation

- Angel Union Budget 2015-16 PreviewDocument51 pagesAngel Union Budget 2015-16 PreviewsriramrangaPas encore d'évaluation

- LGBalakrishnan Annualreport13-14Document120 pagesLGBalakrishnan Annualreport13-14sriramrangaPas encore d'évaluation

- Deloitte Regulatory Alert - Companies Act 2013 - RulesDocument10 pagesDeloitte Regulatory Alert - Companies Act 2013 - RulessriramrangaPas encore d'évaluation

- Capital Gains Accounts Scheme, 1988Document9 pagesCapital Gains Accounts Scheme, 1988sriramrangaPas encore d'évaluation

- 12 Large Cap Blue Chip StocksDocument52 pages12 Large Cap Blue Chip StocksAnonymous W7lVR9qs25Pas encore d'évaluation

- General - Circular - 8 - Commencement Date of Certain SectionsDocument2 pagesGeneral - Circular - 8 - Commencement Date of Certain SectionssriramrangaPas encore d'évaluation

- Astral PolytechnikDocument58 pagesAstral PolytechniksriramrangaPas encore d'évaluation

- KPMG Flash News - Additional Guidelines On Employment Visa and Business ...Document3 pagesKPMG Flash News - Additional Guidelines On Employment Visa and Business ...sriramrangaPas encore d'évaluation

- PWC News Alert 11 February 2014 e Funds Ruling A Silver Lining For Contract Service ProvidersDocument3 pagesPWC News Alert 11 February 2014 e Funds Ruling A Silver Lining For Contract Service ProviderssriramrangaPas encore d'évaluation

- Deloitte International Tax Alert - E-Fund CorpDocument7 pagesDeloitte International Tax Alert - E-Fund CorpsriramrangaPas encore d'évaluation

- Deloitte BusinessTax Alert - Dolphin Drilling LTDDocument3 pagesDeloitte BusinessTax Alert - Dolphin Drilling LTDsriramrangaPas encore d'évaluation

- Capital Gains Accounts Scheme, 1988Document9 pagesCapital Gains Accounts Scheme, 1988sriramrangaPas encore d'évaluation

- Nhai Im 2013-14 02-04-13Document30 pagesNhai Im 2013-14 02-04-13Pankaj GoyenkaPas encore d'évaluation

- 08 MCN F 29062013Document12 pages08 MCN F 29062013sriramrangaPas encore d'évaluation

- CHR Report 2017 IP Nat InquiryDocument30 pagesCHR Report 2017 IP Nat InquiryLeo Archival ImperialPas encore d'évaluation

- S No Name of The Company Regional OfficeDocument39 pagesS No Name of The Company Regional OfficeNo namePas encore d'évaluation

- Reading #11Document2 pagesReading #11Yojana Vanessa Romero67% (3)

- 95 IDocument17 pages95 IsvishvenPas encore d'évaluation

- Bacnet Today: W W W W WDocument8 pagesBacnet Today: W W W W Wmary AzevedoPas encore d'évaluation

- Time-Series Forecasting: 2000 by Chapman & Hall/CRCDocument9 pagesTime-Series Forecasting: 2000 by Chapman & Hall/CRCeloco_2200Pas encore d'évaluation

- ABSTRACT (CG To Epichlorohydrin)Document5 pagesABSTRACT (CG To Epichlorohydrin)Amiel DionisioPas encore d'évaluation

- HD785-7 Fault Codes SEN05900-01-3Document16 pagesHD785-7 Fault Codes SEN05900-01-3ISRAEL GONZALESPas encore d'évaluation

- Safurex - Sandvik Materials TechnologyDocument14 pagesSafurex - Sandvik Materials TechnologyGhulam AhmadPas encore d'évaluation

- Safety Manual For DumperDocument9 pagesSafety Manual For DumperHimanshu Bhushan100% (1)

- " Distribution Channel of Pepsi in Hajipur ": Project ReportDocument79 pages" Distribution Channel of Pepsi in Hajipur ": Project ReportnavneetPas encore d'évaluation

- Asmsc 1119 PDFDocument9 pagesAsmsc 1119 PDFAstha WadhwaPas encore d'évaluation

- Types of TrianglesDocument5 pagesTypes of Trianglesguru198319Pas encore d'évaluation

- Fault Tree AnalysisDocument23 pagesFault Tree Analysiskenoly123Pas encore d'évaluation

- Creating Website Banners With Photoshop PDFDocument18 pagesCreating Website Banners With Photoshop PDFLiza ZakhPas encore d'évaluation

- Ahi Evran Sunum enDocument26 pagesAhi Evran Sunum endenizakbayPas encore d'évaluation

- Sweet Delight Co.,Ltd.Document159 pagesSweet Delight Co.,Ltd.Alice Kwon100% (1)

- 34-Samss-718 (12-02-2015)Document14 pages34-Samss-718 (12-02-2015)Mubin100% (1)

- SD HospitalDocument2 pagesSD HospitalSam PowelPas encore d'évaluation

- Modern Computerized Selection of Human ResourcesDocument10 pagesModern Computerized Selection of Human ResourcesCristina AronPas encore d'évaluation

- Financial Ratio Analysis FormulasDocument4 pagesFinancial Ratio Analysis FormulasVaishali Jhaveri100% (1)

- Bbit/Bptm: Busbar Insulating Tubing (5-35 KV)Document1 pageBbit/Bptm: Busbar Insulating Tubing (5-35 KV)Stephen BridgesPas encore d'évaluation

- Atex ExplainedDocument3 pagesAtex ExplainedErica LindseyPas encore d'évaluation

- Project 2 - Home InsuranceDocument15 pagesProject 2 - Home InsuranceNaveen KumarPas encore d'évaluation

- Foreclosure Letter - 20 - 26 - 19Document3 pagesForeclosure Letter - 20 - 26 - 19Santhosh AnantharamanPas encore d'évaluation

- 2013 CATALOG - WebDocument20 pages2013 CATALOG - WebDevin ZhangPas encore d'évaluation

- EXHIBIT 071 (B) - Clearfield Doctrine in Full ForceDocument4 pagesEXHIBIT 071 (B) - Clearfield Doctrine in Full ForceAnthea100% (2)

- Entrepreneurial Management - Midterm ReviewerDocument6 pagesEntrepreneurial Management - Midterm ReviewerAudrey IyayaPas encore d'évaluation

- PD Download Fs 1608075814173252Document1 pagePD Download Fs 1608075814173252straullePas encore d'évaluation

- Forging 2Document17 pagesForging 2Amin ShafanezhadPas encore d'évaluation