Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- MR - Baiju - MagistrateDocument7 pagesMR - Baiju - MagistrateBaiju TdPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 2nd Online Week5-6Document34 pages2nd Online Week5-6Jennifer De LeonPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Republic Act No. 8424: (Tax Reform Act of 1997)Document34 pagesRepublic Act No. 8424: (Tax Reform Act of 1997)Hanna DevillaPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Retail Management: Prof. Raghavendran.VDocument29 pagesRetail Management: Prof. Raghavendran.VVenkat GVPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Naming and Filing Audit Evidence GuideDocument8 pagesNaming and Filing Audit Evidence GuideGellie De VeraPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

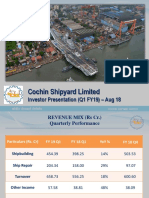

- CSL Investor Presentation Aug 18Document21 pagesCSL Investor Presentation Aug 18gopalptkssPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Derivative+Market - Recent Trends ND Development, Future .Document25 pagesDerivative+Market - Recent Trends ND Development, Future .KARISHMAAT86% (7)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- BP PLASTICS HOLDING BHD Income Statement - MYX - BPPLAS - TradingViewDocument4 pagesBP PLASTICS HOLDING BHD Income Statement - MYX - BPPLAS - TradingViewyasmin nabilahPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Historical Financial Analysis - CA Rajiv SinghDocument78 pagesHistorical Financial Analysis - CA Rajiv Singhవిజయ్ పి100% (1)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 pagesInterim Financial Reporting: Problem 45-1: True or FalseMarjoriePas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- TCWDocument2 pagesTCWPanget PenguinPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Lecture 11 - Getting Funding of FinancingDocument18 pagesLecture 11 - Getting Funding of FinancingMaryam AslamPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Certificate of Employers ' Liability Insurance (A)Document1 pageCertificate of Employers ' Liability Insurance (A)Vincent JohnPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Panama Petrochem LTDDocument7 pagesPanama Petrochem LTDflying400Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Marcos-Araneta v. CADocument3 pagesMarcos-Araneta v. CAJenny Mary DagunPas encore d'évaluation

- PS1SFinal PDFDocument3 pagesPS1SFinal PDFAnonymous lIMsLJNSPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- AtcpDocument2 pagesAtcpnavie VPas encore d'évaluation

- EouDocument12 pagesEouRuby SinghPas encore d'évaluation

- 47 Electricity Accounting Theory ProblemsDocument5 pages47 Electricity Accounting Theory Problemsbala_ae100% (1)

- "Hamburg Summit: China Meets Europe" - Documentation 2010Document21 pages"Hamburg Summit: China Meets Europe" - Documentation 2010Handelskammer HamburgPas encore d'évaluation

- Recent Trends in Public Sector BanksDocument79 pagesRecent Trends in Public Sector Banksnitesh01cool67% (3)

- Corporate Finance Case StudyDocument26 pagesCorporate Finance Case StudyJimy ArangoPas encore d'évaluation

- Five Year Plans of IndiaDocument18 pagesFive Year Plans of IndiaYasser ArfatPas encore d'évaluation

- ABM - BF12 IVm N 24Document4 pagesABM - BF12 IVm N 24Raffy Jade SalazarPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Flat Cargo Case SummaryDocument7 pagesFlat Cargo Case Summaryamir5035Pas encore d'évaluation

- Aligning Training With Corporate StrategyDocument8 pagesAligning Training With Corporate StrategyRudrakshi RazdanPas encore d'évaluation

- Moony: Betting Model ResultsDocument3 pagesMoony: Betting Model ResultsNikola KarnasPas encore d'évaluation

- 5 Series LLC Strategies EbookDocument11 pages5 Series LLC Strategies EbookjuniormintsPas encore d'évaluation

- Shinsegae (004170 KS - Buy)Document7 pagesShinsegae (004170 KS - Buy)PEPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- CostsrelationDocument26 pagesCostsrelationManprita BasumataryPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)