Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The Financial System and The EconomyDocument258 pagesThe Financial System and The EconomyUmkc Economists90% (58)

- MINDS Conference - 24.7.15Document3 pagesMINDS Conference - 24.7.15Umkc EconomistsPas encore d'évaluation

- Homo Oecnomicus and The ClimateDocument28 pagesHomo Oecnomicus and The ClimateUmkc EconomistsPas encore d'évaluation

- The Nature of MoneyDocument39 pagesThe Nature of MoneyUmkc Economists50% (2)

- Framing MMT - Modern Money NetworkDocument23 pagesFraming MMT - Modern Money NetworkUmkc Economists86% (7)

- System Dynamics of Interest Rate Effects On Aggregate Demand PDFDocument24 pagesSystem Dynamics of Interest Rate Effects On Aggregate Demand PDFUmkc Economists100% (2)

- Post Keynesian Conference ScheduleDocument19 pagesPost Keynesian Conference ScheduleUmkc EconomistsPas encore d'évaluation

- Augustana Talk KeynoteDocument70 pagesAugustana Talk KeynoteUmkc Economists100% (1)

- MMT Coloring BookDocument12 pagesMMT Coloring BookUmkc Economists91% (11)

- Balanced Budgets and DeficitsDocument1 pageBalanced Budgets and DeficitsUmkc EconomistsPas encore d'évaluation

- Robert Eisner's Save Social Security From Its SaviorsDocument17 pagesRobert Eisner's Save Social Security From Its SaviorsUmkc Economists100% (1)

- FASAB Hearing Transcript 2-25-2009 Galbraith and MoslerDocument36 pagesFASAB Hearing Transcript 2-25-2009 Galbraith and MoslerUmkc EconomistsPas encore d'évaluation

- Where The Wild Things Aren'tDocument69 pagesWhere The Wild Things Aren'tUmkc EconomistsPas encore d'évaluation

- Berg HartleyDocument20 pagesBerg HartleyUmkc EconomistsPas encore d'évaluation

- SSN Key Findings Page On Deficit Hawks and Wealthy AmericansDocument2 pagesSSN Key Findings Page On Deficit Hawks and Wealthy AmericansUmkc EconomistsPas encore d'évaluation

- FdicraDocument1 pageFdicraUmkc EconomistsPas encore d'évaluation

- Life After DebtDocument18 pagesLife After DebtUmkc Economists100% (1)

- Democracy and The Policy Preferences of Wealthy AmericansDocument53 pagesDemocracy and The Policy Preferences of Wealthy AmericansUmkc EconomistsPas encore d'évaluation

- Galbraith Who Are These Economist AnywayDocument13 pagesGalbraith Who Are These Economist Anywayanas_jalilPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- BuwisDocument23 pagesBuwisshineneigh00Pas encore d'évaluation

- 30 Days To Real Estate CashDocument160 pages30 Days To Real Estate Cashbillyd0189% (9)

- Development proposal for office & apartment blocks in Ampang, Kuala LumpurDocument16 pagesDevelopment proposal for office & apartment blocks in Ampang, Kuala Lumpursongkk100% (1)

- DM - IntroductionDocument88 pagesDM - IntroductionSagar PatilPas encore d'évaluation

- Dacion en PagoDocument2 pagesDacion en PagoJC93% (15)

- The Fund of Funds: A Focus On Independence: SynopsisDocument4 pagesThe Fund of Funds: A Focus On Independence: SynopsisCryptic LollPas encore d'évaluation

- Functions of A Credit Rating AgencyDocument22 pagesFunctions of A Credit Rating Agencyharshubhoskar3500Pas encore d'évaluation

- Megaworld Globus Asia, Inc., Petitioner, vs. Mila S. TansecoDocument12 pagesMegaworld Globus Asia, Inc., Petitioner, vs. Mila S. TansecoGab CarasigPas encore d'évaluation

- The Great Depression - Assignment # 1Document16 pagesThe Great Depression - Assignment # 1Syed OvaisPas encore d'évaluation

- International Introduction To Securities and Investment Ed6 PDFDocument204 pagesInternational Introduction To Securities and Investment Ed6 PDFdds50% (2)

- Agri Gr8 PresentationDocument45 pagesAgri Gr8 PresentationJames WilliamPas encore d'évaluation

- All About Sale and Mortgage Under Transfer of Property Act 1882 by Rohan UpadhyayDocument9 pagesAll About Sale and Mortgage Under Transfer of Property Act 1882 by Rohan Upadhyayved prakash raoPas encore d'évaluation

- EPC Contract: Draft For Discussion PurposesDocument125 pagesEPC Contract: Draft For Discussion PurposesSrinivasan JanakiramanPas encore d'évaluation

- Banglladesh Bank DPTDocument40 pagesBanglladesh Bank DPTMorshedul ArefinPas encore d'évaluation

- Why Is The BSP The Main Government Agency Responsible For Promoting Price StabilityDocument4 pagesWhy Is The BSP The Main Government Agency Responsible For Promoting Price StabilityMarielle CatiisPas encore d'évaluation

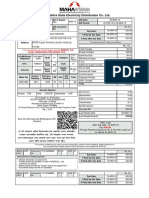

- Light Bill Sept 2019Document1 pageLight Bill Sept 2019Sanjyot KolekarPas encore d'évaluation

- Entrepreneurship, Marketing and Financial ManagementDocument96 pagesEntrepreneurship, Marketing and Financial ManagementPreeti Joshi SachdevaPas encore d'évaluation

- COL - PhilSec Vs CADocument4 pagesCOL - PhilSec Vs CAbuyreasPas encore d'évaluation

- Political Economy Students Group and Individual AchievementsDocument7 pagesPolitical Economy Students Group and Individual AchievementsMaricar BautistaPas encore d'évaluation

- 19-01 Audit Report - Grove Harbour Marina - FINAL PDFDocument11 pages19-01 Audit Report - Grove Harbour Marina - FINAL PDFal_crespoPas encore d'évaluation

- 15 - Country Bankers Insurance Corp Vs Lianga BayDocument8 pages15 - Country Bankers Insurance Corp Vs Lianga BayVincent OngPas encore d'évaluation

- Big Bank Business: The Ethics and Social Responsibility of The Finance IndustryDocument2 pagesBig Bank Business: The Ethics and Social Responsibility of The Finance IndustryFaculty of the ProfessionsPas encore d'évaluation

- Final PPT UmppDocument13 pagesFinal PPT UmppDhritiman PanigrahiPas encore d'évaluation

- 2 Corinthians 1: 20 - 22 Explains God's Promises in ChristDocument39 pages2 Corinthians 1: 20 - 22 Explains God's Promises in ChristYu BabylanPas encore d'évaluation

- Jaiib - 2 Afb - Quick Book Nov 2017Document136 pagesJaiib - 2 Afb - Quick Book Nov 2017Chinnadurai Lakshmanan75% (4)

- Analysis of Financial Performance of SbiDocument5 pagesAnalysis of Financial Performance of SbiMAYANK GOYALPas encore d'évaluation

- MAT112 DOCUMENT ED: 100000 ? - / I 6 V: Universiti Teknologi Mara Final ExaminationDocument8 pagesMAT112 DOCUMENT ED: 100000 ? - / I 6 V: Universiti Teknologi Mara Final ExaminationMuhammad Rifdi50% (2)

- Islamic Law ProjectDocument8 pagesIslamic Law ProjectSami UllahPas encore d'évaluation

- The Global Crisis and Vietnam's Policy Responses: LE Thi Thuy VanDocument12 pagesThe Global Crisis and Vietnam's Policy Responses: LE Thi Thuy VanAly NguyễnPas encore d'évaluation

- Pasani Loan Terms & Condition For Baloyi Wisani CydrickDocument6 pagesPasani Loan Terms & Condition For Baloyi Wisani CydrickClint AnthonyPas encore d'évaluation