Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Statement of Account: Juanima Porter 102 Bonita CT SUMMERVILLE SC 29485-0000Document5 pagesStatement of Account: Juanima Porter 102 Bonita CT SUMMERVILLE SC 29485-0000Kelley73% (15)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Saptashati Sammanit ChandichintaDocument357 pagesSaptashati Sammanit ChandichintaKnowledge Guru100% (2)

- Reckoning of Child From SaptamsaDocument3 pagesReckoning of Child From SaptamsaKnowledge Guru100% (1)

- Investigating Role of IBNs in Cross-Border M and As in Banking SectorDocument10 pagesInvestigating Role of IBNs in Cross-Border M and As in Banking SectorAnanTh Mullapudi100% (1)

- Shri Chandi GranthaDocument384 pagesShri Chandi GranthaKnowledge GuruPas encore d'évaluation

- Falit Jyotish (Bengali)Document1 251 pagesFalit Jyotish (Bengali)Knowledge Guru78% (23)

- As 18Document13 pagesAs 18Knowledge GuruPas encore d'évaluation

- SEBI (Prohibition of Insider Trading) Regulations, 2015Document21 pagesSEBI (Prohibition of Insider Trading) Regulations, 2015Shyam SunderPas encore d'évaluation

- Membership Interest Pledge AgreementDocument6 pagesMembership Interest Pledge AgreementKnowledge Guru100% (1)

- Listing Agreement 16052013 BSEDocument70 pagesListing Agreement 16052013 BSEkpmehendalePas encore d'évaluation

- Interim Order Was Passed Without Prejudice To The Right of SEBI To Take Any Other ActionDocument3 pagesInterim Order Was Passed Without Prejudice To The Right of SEBI To Take Any Other ActionKnowledge GuruPas encore d'évaluation

- Nava Naga StotramDocument1 pageNava Naga StotramKnowledge GuruPas encore d'évaluation

- Kaala Bhairava Ashtakam Eng v1Document0 pageKaala Bhairava Ashtakam Eng v1ganeshabbottPas encore d'évaluation

- M S Wolstenholme International ... Vs Twin Stars Industrial ... On 5 March, 2001Document7 pagesM S Wolstenholme International ... Vs Twin Stars Industrial ... On 5 March, 2001Knowledge GuruPas encore d'évaluation

- SRF Limited Vs State of Madhya Pradesh and Ors. On 29 November, 2004Document13 pagesSRF Limited Vs State of Madhya Pradesh and Ors. On 29 November, 2004Knowledge GuruPas encore d'évaluation

- State of Punjab Vs M S Nestle India Ltd. & Anr On 5 May, 2004Document13 pagesState of Punjab Vs M S Nestle India Ltd. & Anr On 5 May, 2004Knowledge GuruPas encore d'évaluation

- Account StatementDocument2 pagesAccount StatementGaurav mishraPas encore d'évaluation

- Spouses Tolosa v. United Coconut Planters BankDocument2 pagesSpouses Tolosa v. United Coconut Planters BankJuno GeronimoPas encore d'évaluation

- Interest Rate RiskDocument41 pagesInterest Rate RiskPardeep Ramesh AgarvalPas encore d'évaluation

- Sun Hung Kai 2007Document176 pagesSun Hung Kai 2007Setianingsih SEPas encore d'évaluation

- About Commercial Banks in EthiopiaDocument91 pagesAbout Commercial Banks in EthiopiaDawit G. TedlaPas encore d'évaluation

- Explanation T030 GGP en 2Document39 pagesExplanation T030 GGP en 2scontranPas encore d'évaluation

- Digital Financial Inclusion andDocument6 pagesDigital Financial Inclusion andInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- 1 LicDocument1 page1 LicAshish BatraPas encore d'évaluation

- Accenture IT Blueprint For The Everyday BankDocument12 pagesAccenture IT Blueprint For The Everyday BankCristian RoscaPas encore d'évaluation

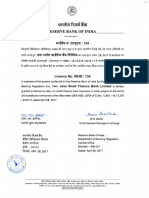

- RBI Approved BankDocument1 pageRBI Approved BankVįňäý Ğøwđã VįñîPas encore d'évaluation

- Exercise For Week 5 v5Document27 pagesExercise For Week 5 v5Mayur GBPas encore d'évaluation

- A Presentation On: Credit CardsDocument26 pagesA Presentation On: Credit Cardsshweta.gdp100% (2)

- Fiduciary Duties of BanksDocument8 pagesFiduciary Duties of BanksTimothy Nshimbi0% (1)

- Customer Satisfaction in E-CommerceDocument66 pagesCustomer Satisfaction in E-CommerceAndrei Nebunoiu100% (1)

- Adsum Notes Credit Trans FactoidDocument2 pagesAdsum Notes Credit Trans FactoidRaz SPPas encore d'évaluation

- P2P and O2CDocument59 pagesP2P and O2Cpurnachandra426Pas encore d'évaluation

- BCC BR 107 152Document12 pagesBCC BR 107 152lkamalPas encore d'évaluation

- BMA Demo 2Document28 pagesBMA Demo 2Huế HoàngPas encore d'évaluation

- BUSANA1 Chapter 4: Sinking FundDocument17 pagesBUSANA1 Chapter 4: Sinking Fund7 bitPas encore d'évaluation

- Msme PDFDocument206 pagesMsme PDFashish100% (1)

- Security Bank Corp v. Victorio - 1Document6 pagesSecurity Bank Corp v. Victorio - 1LegaspiCabatchaPas encore d'évaluation

- Government of KarnatakaDocument5 pagesGovernment of KarnatakaShekarKrishnappaPas encore d'évaluation

- Disclosure No. 132 2016 Top 100 Stockholders As of December 31 2015Document6 pagesDisclosure No. 132 2016 Top 100 Stockholders As of December 31 2015Mark AgustinPas encore d'évaluation

- Sabari Final ProjectDocument54 pagesSabari Final ProjectRam KumarPas encore d'évaluation

- Research Proposal On Mobile Banking PDFDocument12 pagesResearch Proposal On Mobile Banking PDFKhalid de CancPas encore d'évaluation

- Agoda, Look AlikeDocument1 pageAgoda, Look AlikeJem MadridPas encore d'évaluation

- Remittance AdviceDocument5 pagesRemittance AdvicellllllluisPas encore d'évaluation

- Saferpay Payment Page V4.1.3 enDocument31 pagesSaferpay Payment Page V4.1.3 enMiguel NoriegaPas encore d'évaluation